Well I’m only interested in % variation year to year compared to the benchmark so currency effect don’t really matter because the underlying assets are anyway in multiple currencies and in a similar allocation (VT, VWRL). The benchmark on the table is reported with the same currency than the ETF.

What I wanted to say is that when you are trying to get 0.1% better TER than you are entering a realm where you are more susceptible to tracking error and security lending, which are more or less manager dependent. So pure TER should not be the final criteria. You must understand the underlying index too.

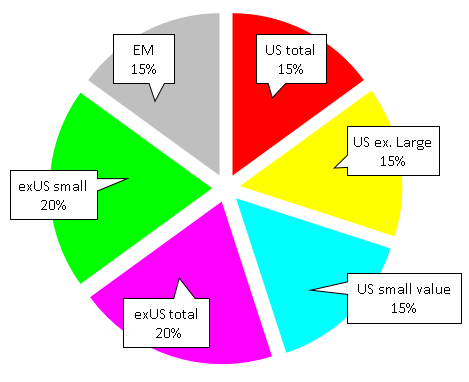

I’d be interested in opinions on my portfolio as I think it still requires a bit of refinement. I am deliberately underweighted in the US as I have taken an opinion that values are currently too high, over time I would consider increasing the weighting. The GBP funds are a requirement, as I slowly transfer historical GBP cash to CHF I wish to remain invested incase of GBP weakening hopefully fund performance would offset this a little.

I was looking at somehow putting a Eurozone fund in there to reduce the UK and CH bias a bit as certain companies reoccur in multiple funds. I liked having the small cap world but was a little worried about having the US domiciled fund, not sure how much of an issue this is regarding dividend taxes etc (no US stocks, US domiciled, would consider a good alternative if someone has a suitable suggestion).

This portfolio makes up about 70% of my wealth, with the rest in pensions etc. Considering my investment horizon due to perhaps buying a house in the next 5 years I am probably overweighted equities. I am aware of this but happy with the portfolio as we just can’t decide what we want to do medium / long term anyway so maybe it doesn’t happen so soon.

You’re losing money with it at crazy rate from holding (Weighted Average Yield To Maturity: -0.62%), fund expenses (-0.15%), taxes (assuming 35% tax * 2% distribution yield: -0.70%) and transaction costs. The only way you’d make any money out of it is if yields would drop down a lot more and that’s not exactly happening for good last half a year (SNB, Bloomberg).

There’s no reason for retail investors to buy any of these negative yielding abominations. You can just hold the cash in a savings account at 0% and still be covered by the government up to 100k per bank. Once you start running out of banks you could trust your money to, then it might make some sense to do it, to put the trust into government. Otherwise it’s just a rather expensive bet on interest rates going down.

You might have bought it from an exchange which quoted it to you in GBP, but don’t fool yourself: it’s not really tied to GBP in any way and only has 28% of UK companies in it. And also it seems to have already some 10% in Switzerland, overlapping somewhat with your SLI position (e.g Nestle Novartis Roche make up 7% and 26% in each).

If you’re certain that you want to buy in 3-5 years and have a high tax burden, I’d rather put the money for downpayment into pillar 2 and 3. Tax savings is guaranteed income (albeit one time only) and easily blows away other investment alternatives for such a short term, despite abysmal interest rates.

But if you’d rather stay heavily in equities for this period, then I’d at least cut out EM and small caps, these casinos will tank faster than the market in a downturn, they are rather low on defensive sectors. Maybe also consider low volatility themed funds instead of capitalization weighted.

IB will loan you CHF currently at 1.5% on the margin. But at 50% it’s very risky, they’ll start selling stocks once the market goes down. You need to be below 50% at the end of each day

Some banks I’ve heard accept stocks as collateral and would give you a higher than 80% mortgage then, but you need to pay them custody fee and mortgage rate on this extra money, so in the end it might not be much better than IB. I don’t know though what margin they allow in this case, so possibly you could loan more through bank than IB

You should be able to arrange something with brokers linked to banks like cornertrader with cornerbank.

I don’t know if Postfinance offers it

Exactly if you have stock to pledge they may go higher and give you 85/90% mortgages.

Well I’ve heard cantonal banks do it, e.g. ZKB. But you’re looking at paying 0.3-0.4% custody fee for parking stocks with them, in addition to mortgage interest. Amortization payment will also be higher, this part of the mortgage has to be fully amortized linearly within 15 years

traditionally this was the purpose of the money market (short termed bonds <1 year, even down to 1 day) but since the low interest area, it hardly serves al alternative to cash anymore.

So, here I come up with the last draft of my new portfolio. the old one is here. By extending my investment universe to US based Vanguard funds, It is now much more consequent in terms of how my dream-portfolio looks like. Again, this would be an equal amount of $$ in every liquid stock in the world, with some value weighting. 100% stocks, at least for that part of my stash that i can freely define (unlike pillars 1,2,3):

with a total expense ratio below 0.1% and an weighted average of 3’700 stocks per ETF but be aware of some overlaps.

the regional distribution is close to that of VT, with EM somewhat overweighted:

50% north america

20% Europe

20% emerging markets

10% rest

rest: others

the size factor is clearly different, with mid caps overweighted and small caps significantly overweighted: 40/34/26 where VT has 77/18/6.

I also want to overwight Value stocks, but when i wrote down the value-blend-growth distribution according to morningstar, I found i cannot do too much about it unless i sacrifice diversification and low TERs. VBR seems the only value fund that does ok with both, but is actually not that valuey, according to altruist advisors. it has about 50% value stocks according to morningstar, somewhat more than 1/3rd.

I also dropped the home bias since SPI stocks are already contained in VXUS. Nestle is the top position there, and roche & Novartis #4 and #5 my beloved SMPCHA simpy shatters at the diversification argument.

What exactly are you trying to achieve with this value and size tilts? Value’ is not a defensive play, everything will crash just as fine as general market. Small caps even more, with their 1.10 beta at the moment

i again forgot to mention i have a 30-60 years time horizon. small & value is believed to grant a risk premium on the long run. this is exactly what i try to achieve^^

Here is my first draft of my portfolio as a stock/bond newbie. When i compare this to @nugget or others i have to get way more precise. I am looking into ETF’s right now, but it is still a big jungle to me. Next step is to find the right products for equity/etf’s and fixed income/bonds. If you have suggestions or good experiences, that would be very welcome.

Portfolio

50% ETF/Bonds

25% Säule 3a (in progress to max out stock portion)

20% Sparkonto (yes, this could be less and will decrease overtime anyway)

5% Cryptocurrencies

Another dumb question which relates to both portfolios. When a position grows, but you don’t sell it (cryptocurrencies in my case, but could be Emerging Markets as well). Do you sell it to stick to your plan (rebalance porfolio) or do you let it grow and change your plan? I do not want to sell my positions for now in crypto, but they grow like crazy - but the risk is of course high as well.

Portfolio ETF/Bonds

20% Bonds

10% World Value (MSCI)

10% Europe (MSCI)

10% Emerging Markets (MSCI)

10% USA Large Cap Value

10% USA Small Cap

10% USA Small Cap Value

10% Dax or Swiss Stock (home-biased)

10% MDax or Swiss Medium Caps (home-biased)

This is the profit oriented portfolio recommended by Gottfried Heller from his Book (‘Der einfache Weg zum Wohlstand’). He explained a lot of the basics for me and i am surprised that the main strategy is actually very similar to mustachian portfolios (although with a strong german focus) - makes me even more confident to take this route.

Next Step is to select the products and buy them somewhere. I would like to keep it simple and have only one Broker. It seems Interactive Broker is the favourite here or has anyone another suggestion or maybe bad experiences with IB?

The ratio of Bonds/Stocks would depend of your age/risk.

If you have stocks/bonds in the 3a, take them into account in the stocks/bonds allocation.

8 stocks funds are maybe too much and some of them are overlapping other. 10% for each fund seems quite arbitrary.

Why do you prefer MSCI instead of FTSE or S&P ?

ratio: yes, i should have more bonds for my age, but bonds are at the moment quiet low and i am ok with more risk.

3a: Thanks, this is a huge error - i will include it.

8 Funds: Maybe too much, i am not experienced. It’s about diversification.

MSCI: No preference, was just mentioned like this.

hey rogerized,

if you find some value-ETFs please let me know i intend to do some value weighting in my portfolio, but i hardly found any good etfs for me, except VBR.

Hi guys and gals.

We have some pretty experienced investors in this forum and i have a simple question. If you could put 200k in a passive ETF Portfolio - what would you do for a longterm lazy version? And would you split it over different brokers?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

i intend to do some value weighting in my portfolio, but i hardly found any good etfs for me, except VBR.

i intend to do some value weighting in my portfolio, but i hardly found any good etfs for me, except VBR.