I found more examples at Bogleheads for US and international markets, but they arealready a bit outdated.

…

Background:

After running well with my original portfolio from 2017, i thought after 6 years i should update it. Markets have moved in the mean time, so have economies and so forth.

What is a current combination of ETFs that create an all-world portfolio?

What is the methodology, and where comes the data from?

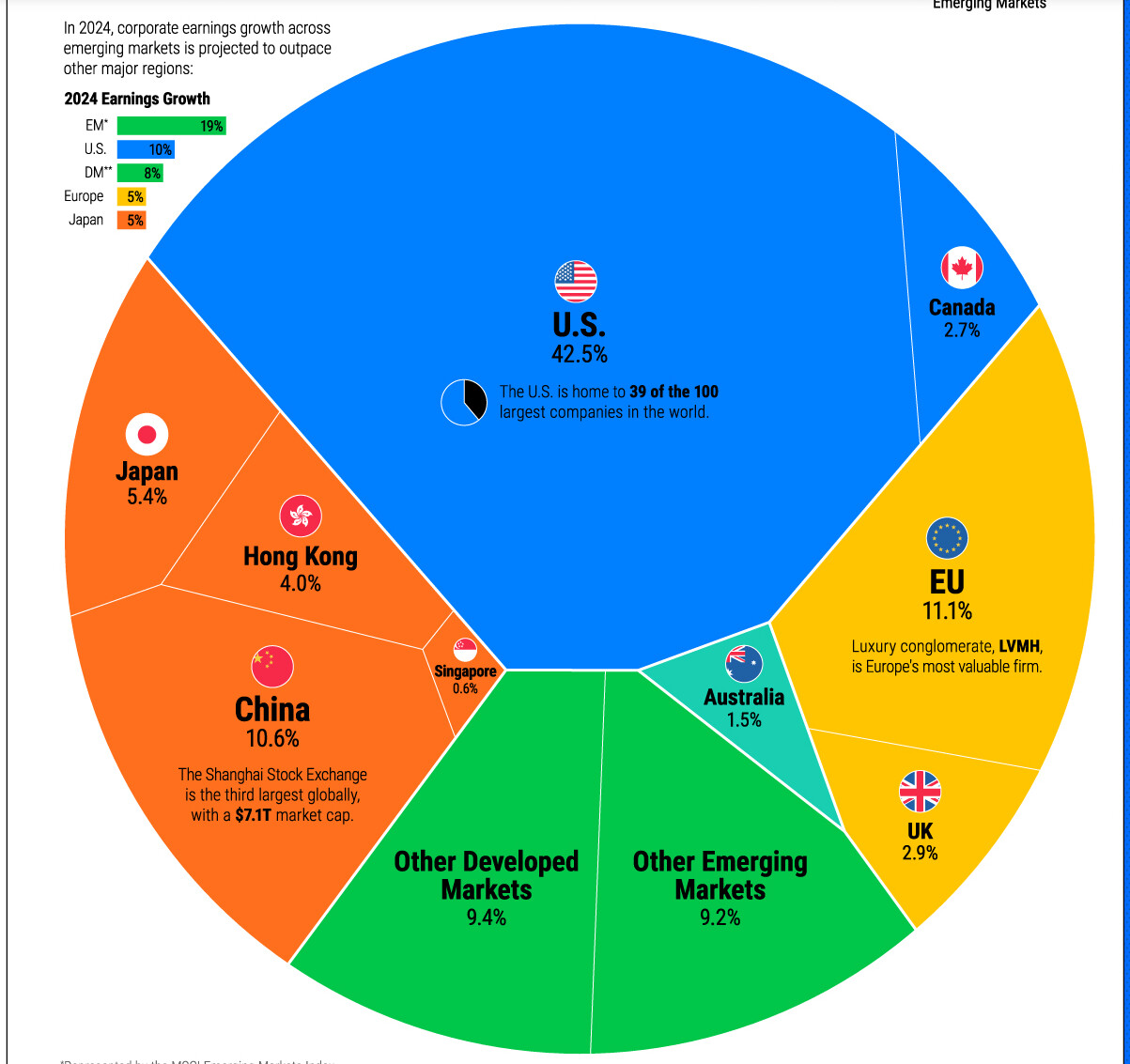

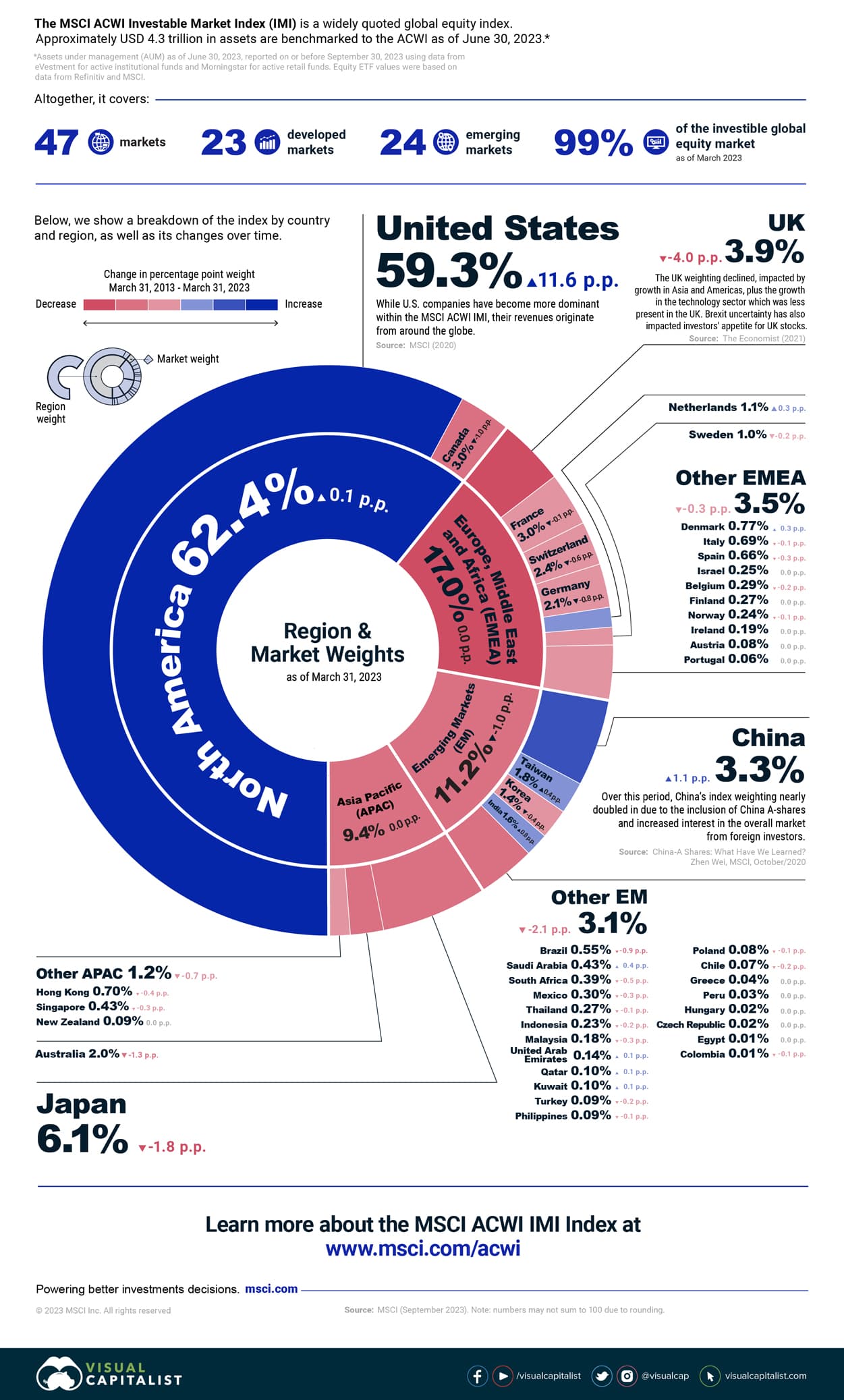

for example, Visual Capitalist has a nice chart (however it being static and not updated) with data from sifma :

thanks all for sharing your allocations.

However I am looking more for a methodology to come up with it for examle

why 60-30-10 and not 58-31-11 ?

well the answer should be “because this allocation comes closest to representing while respecting the constraints of <whatever limits you, for example portfolio complexity>”

I remember thinking along the lines of

“FTSE All-World has 55% US, 10% EU, 15% APAC and 20% EM, and this can be recreated with varying levels of sophistication by combining the following ETFs: … while paying attention to ETF X has exposure to the developed ex-US World and thus overlaps with ETF Y…”

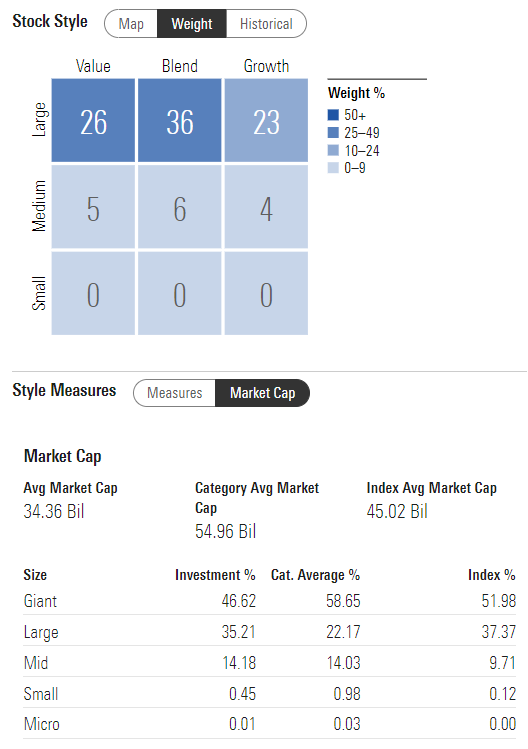

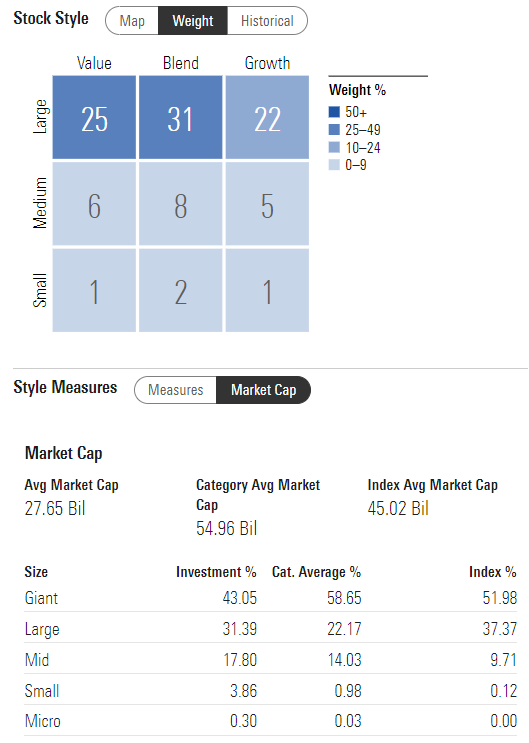

Could you please explain what you mean by the size tilt? Is one large cap and another not. Sometimes I struggle to see the difference between some of the different Vangaurd ETFs.

For example, is the only difference bewteen VXUS and VEU that VEU is sampled (vs index replication)? It also seems strange that this results in a higher expense ratio whereas I’d expect the opposite.

Maybe for more control. e.g. if you already have single stock holdings in the US and want to maintain a certain ratio of US to non-US could you decrease the VTI vs VXUS holding.

Interesting. In the description at the top it says for VEU and VXUS: “Category: Foreign Large Blend” so I assumed it was the same and thought the median market cap might have been due to the indexing vs sampling difference.

The no direct exposure to the IRS, free US weighting 6 funds porftolio:

US - 61%: SPYL

Canada - 3%: CSCA

Dev Europe - 16%: IMEA

Dev Pacific ex Japan - 4%: CPXJ

Japan - 6%: XMJP

EM - 10%: EIMI

Israel is ignored because a rounded 0.20% makes 0%.

The no US, no EM 4 funds version:

Canada - 10%: CSCA

Dev Europe - 54%: IMEA

Dev Pacific ex Japan - 14%: CPXJ

Japan - 22%: XMJP

The choice of funds can be optimized, broad discretion has been used to select accumulating variants with some kind of attempt at balance between TER and AUM. I don’t guarantee that all are investable by individual investors.

Weightings from VT, funds selected for their non-us domicile, capitalization structure, tax pseudo-efficiency, pseudo low TER and pseudo decent AUM. The main goal is to avoid direct exposure with the US tax system and tax authorities, along with allowing a more free weighting of the US components of the portfolio (for less or no exposure to them). As you can see, that comes at the cost of complexity and fees.

Well, it’s not 100% IRS neutral since US companies are exposed to US taxation and WHT are witheld on the dividends the fund receives but I would consider VWRL as a suitable no direct IRS investment fund (as is SPYL which I used in my first suggestion).

My first idea was to avoid the US altogether (so no US companies) but I’ve grown more tolerant with time and would now just underweight the US, while still not wanting any direct involvment with their tax authorities so that gave rise to my suggestions above.

I went down the rabbit hole of a global 1 fund (VT) vs 2 fund (VTI+VXUS) vs. 3 fund (VT+VEA+VWO) vs 4 fund (VT+VEA+VWO+VSS) solution. I couldn’t figure a couple of things out.

From what I can tell some US residents go for 2 or more fund solutions for tax reasons and in this forum I read often about the higher AUM and slightly lower weighted TER of 2/3/4 fund solutions. Plus other factors such as China-A shares not being in VXUS.

I think what seems appealing to me is the fact that having VT split in 2, 3, or 4 ETFs offers more flexibility when selling. E.g., at the time of retirement Ex-US outperforms US, one could sell mostly Ex-US for most gains. I wonder if my thinking is completely off here?

I think with auto-investing tools I also don’t see having 2 or more funds as a downside. I suppose slightly more time for tax declaration but as long as this would be a handful of funds I wouldn’t see a problem.

Where I see a downside to a multi fund approach is the chance to under perform the benchmark. For example, factor tilting and deviating vastly from the benchmark. However, this is where I am confused with regard to rebalancing.

I read that all funds are market cap weighted and there is no need to rebalance. Whereas others argue that one needs to adjust every time when buying the funds depending on their current value. Not sure if this even refers to the same?

Lastly, for Swiss investors. I am aware of the advantage of US-domiciled funds to reclaim the 15% WHT. Is this purely decided if a fund is US domiciled or depends on the portfolio and requires a certain % of US? So in other words one would be able to reclaim with VT but not with an Ex-US fund like VXUS?

It comes down to your strategy and regional allocation. It seems you want to be passive but with some sort of active intent. So based on what is your active intent, you might need to choose funds accordingly.

If you want to invest in whole world and don’t care which countries represent what, then got for VT (or an alternate from ishares or SPDR even though 1-1 equivalent doesn’t exist)

If you want to play with allocation to US vs non-US then VTI and VXUS would work out well

If you want to play with allocation to Developed world ve emerging markets then VEA, VFEM might be needed

Some people use two funds to diversify and harvest tax losses but not sure if that is actually relevant for people living in CH. And some might own two different funds from different fund houses to mitigate fund house specific risk.

Just keep in mind to always look for tracking difference of ETFs you choose. I notice that people are very much worried about TER while ignoring tracking differences. A very good example of this is VWRL where 0.22 % TER seems quite high while it’s tracking difference versus it’s benchmark is almost zero.

The 15% WHT topic is about US portion of the stocks within ETF. If the fund is domiciled in US, then you don’t lose that 15% WHT but if the fund is domiciled in Ireland , you lose it. However for the stocks which are from companies in other countries , this would depend on tax treaty between US and other countries or IE and other countries. I remember seeing on this forum a very good analysis about US vs IE funds in terms of tax advantages. Try to search for it.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.