further, very interesting collection of portfolios here

the same page features a very nice portfolio finder to play with

please add you portfolios (or such you like) in the comments!

Today I have a more chaotic portfolio from my first investments last year. I need to redo it, and write down a clear strategy!

The goal is clear: maximize returns for my retirement that I currently plan in about 35 years. Full risk and return! I plan to go 100% stocks with some CH-bias. small and value weighting, as far as available on the ETF market.

Rebalancing: rearly or whenever fresh savings are available.

besides that I own:

the short term cash i need for living

pillar 1: bond-/ cash- like

pillar 2: bond- like

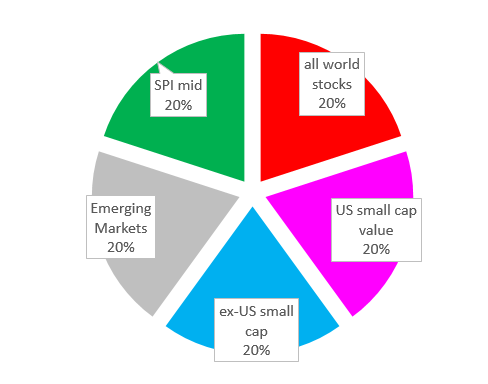

My ideal portfolio would be an equal amount of CHF in every company on the planet. However, I can only invest in what is offered via ETFs. From here, my ideal portfolio would be close to Merriman’s ultimate portfolio (see first post). Unfortuanately most of these ETFs are US domiciled, where the $60’000 cap comes in. So I boil it down to these 5 stock assets where rather reasonable ETFs exist. There is an Emerging Market small cap ETF, but a 0.74 TER is above my personal threshold. All in all 5 ETFs seem to me the higher end for my 50k depot, already 2 more than the lazy 3-fund portfolio.

I like MP’s 3 fund portfolio because of it’s simplicity, but the bonds don’t fit my ideas. I like the ultimate portfolio for its combined diversification and small value focus. however, it looks like ultimate only for us residents, and not feasible for starters.

I know a lot of Mustachian really like indexing and low fees ETFs, but I am more into Value investing, particularly Benjamin Graham’s Net-Nets investing (for those who don’t know this strategy, more details here). i like to pay as little as possible for the assets of a company. In my below portfolio, all stocks were valuated at less than two third than their net current assets at purchase date.

That means that if these companies were to go bankrupt today, and then had to pay all their debts, and had difficulties selling their machines and real estate, there will still be enough cash to pay shareholders more than what they paid for the stocks.

All lines are equally weighted.

The only thing I don’t know with this strategy is the lack of swiss opportunities. Nevertheless the portfolio has performed quite well so far. Plus I know that if a crash happen, I did not pay too much for these stocks so I have a big margin of safety.

@Julianek

I recently met someone doing the same thing. I do see the reasoning behind it. However, is that you full portfolio? And, is not some value-ETF doing exactly the same thing? maybe with less strict buying conditions, but broader diversified?

@nugget

Yes, this is the majority of my invested portfolio (>90%). The rest of my invested portfolio are small ideas I am currently testing. I also keep 25kCHF in cash for emergencies.

Regarding the ETFs, one specificity of this strategy is that it often targets very small caps ( most of them have a cap between 15 and 80 million USD). So an ETF cannot invest in these companies because if it did, it would buy such a big portion of the companies that it would influence in a significant manner the price of the stock. Plus, when an ETF has 1 billion+ USD asset under management, what would justify such a hassle when the stock represents around 1/1000 of your portfolio?

The advantage of that is that institutional investors are not in that game, so EMH is basically invalid here (the very fact that I can find all these companies meeting my criteria make the EMH invalid for these kind of market caps). So there is some significant money to be made.

The drawbacks are mainly two :

-As you noted, there is not ETF/mutual fund with low fees that does the same thing, so I have to pay more fees

-These companies are much rarer at the end of a bull market like currently, so it is sometimes difficult to diversify enough the portfolio. I was originally looking for american stocks (with the tools given by the SEC and yahoo finance it is really easy for a developer to make a custom engine that screens these companies), but i have started looking also on the japanese market too, more manually.

If someone is interested in this kind of strategy, i could do a more detailed topic thread.

By the way, it follows that with this strategy i am looking for a broker who is especially good for US markets (i.e, the fees for US stocks when buying from Switzerland are minimal). If someone knows such a broker, i’ll be very grateful if he could share it!

56% Emerging markets (VFEM)

6% Small cap US (VBR)

17% Large cap (VUSA)

21% swiss equities/SLI (SLICHA)

I find my portfolio too much expose to the swiss market. My optimal portfolio (I’m currently adjusting it) shouldn’t be exposed to the swiss market and should be high volatily/high returns:

50% Emerging

20 % Large US Caps/SP500

30% Small Cap

For Europe: past returns, GDP projection, european laws and cohesion between countries, I live there

For Japan : GDP projection, bad economy for years, aging population

It’s clearly a choice and most of my arguments are speculative

The only strong argument is: if you live and work in Europe you already have one part of the risk for this region.

Also, I’m young that why I have chosen a with high volatility without bonds.

@Dago In my opinion, your portofolio has way too much swiss equities/bonds. Do not forget, Switzerland is only 3% of the total stock capitalisation.

Hi there, happy to share. I like to keep my portfolio simple:

80% Vanguard All-World

10% Vanguard Emerging Markets

10% iShares Core SPI

(0% bonds)

Plus emergency fund in cash (three monthly salaries)

EM for additional growth, SPI because I live here / currency risk.

50% Vanguard Total International Stock ETF (VXUS)

50% Vanguard Total Stock Market ETF (VTI)

3m Salary in Vanguard Intermediate-Term Bond ETF (BIV)

1-2m Salary in Cash

For my child:

100% Vanguard Total World Stock (VT)

I am tempted to put more time in value investing but:

I don’t have the time to read company financial reports nor knows how to debunk them or willing to buy single stocks.

Smart beta ETFs (WisdomTree) are relatively expensive and small or have no history.

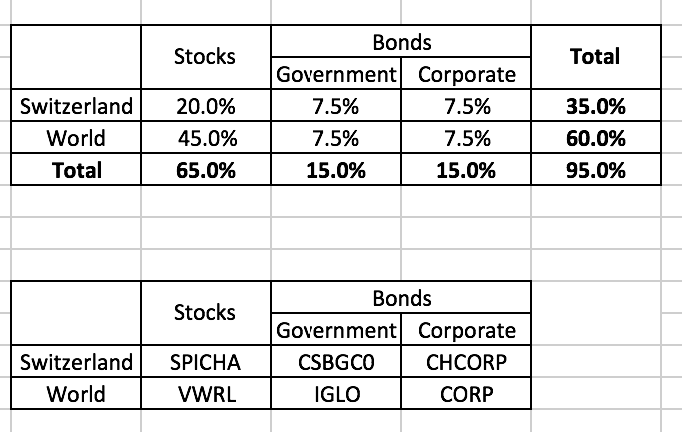

I have a comprehensive view of all my assets located on the different account (taxable, pillar 3, pillar2).

I strive for 80% stocks / 20% income (bond, cash etc). At the moment I’m still 60 % / 40% because my two pillars are pushing up my income part.

my 60% stocks are so divided:

75% international stocks, mostly Vanguard all-world and MSCI world which I estimate is followed by the pillar 3a passive funds (and taking away ~3% for CH)

12.5% Swiss large cap, coming mostly from my pillar 3a funds

12.5% Swiss mid and small cap, completed by buying mostly UBS SPI-Mid ETF

Hey Grog,

I was also considering how a potential pillar 3a could contribute to my portfolio. In case I went for the VZ solution, my 3a pillar portfolio would be

40% SLI

40% MSCI world

20% Bonds

however this is a bit tricky for rebalancing, and these are not exactly the incices i want to be invested in. plus the horrific costs of 0.68% p.a. If i’d put the same money on te SP500 in the hope of outperforming that portfolio by only 0.5%, the whole tax bonus of 3a will be gone. Hm, I am not yet finally sure what to do

0.68% is not bad. Don’t forget that in tax-sheltered account you don’t pay income tax on dividend and coupons.

Eg: you have 20% tax rate on your income. You receive 2% dividends. The additional expense to your TER in taxable account is 20%*2%=0.4%

This doesn’t happen in pillar 3a. So it’s much more difficult to outperform

I’m just starting out with proper investing (after years of mistakes…), so I went for a very simple portfolio:

90% iShares Core MSCI World (IWDA)

10% iShares Core MSCI Emerging Markets IMI (EIMI)

I’m still quite cash-heavy at the moment, so I haven’t bothered with bonds or anything like that. I haven’t put a lot of money on this yet, I’m just figuring things out, but I guess it’s probably safest to buy more regularly rather than do a large lump sum.

Why do some of you bias so heavily towards Switzerland? Is it because you have little cash and you use that to offset the risk? Should I be doing the same?

Hey Alex,

i think the only reason to have a home bias is because this removes currency risk of that oart of our portfolio. otherwise, i don’t know a reason.

My current 3b portfolio looks like this: Its not my retirement portfolio which includs pillars 1,2 and 3a so with this portfolio i have kind of a mixed/unknown investment horizon. thats why i mixed my asset allocation for the 2 time horizons 5-10Y and 20+Y

35% MSCI World

25% MSCI EM imi

10% MSCI Europe

30% Cash (fixed income substitute)

As i see now that i just diversified LC, MC Stock regions i want to simplify things and reduce the cash part.

Core

70% FTSE All-World

20% Barclays Global Aggregate Bond 1-5Y

10% Cash

Satellites (as portfolio and financial knowledge/MaxDD experience grows and interestrates climb )

MSCI World Small Cap

SBI AAA-AA Bonds

extend maturity of the Barclays

maybe EM and HY Bonds

Frontiermarkets if low cost is available and portfolio is big enough to make sense (this is just caused by the perfection demon in me who wants to bi invested in the last 0.whatever%. as long as i am not invested here i am mentally stable and still poor enough )

I dont intend to use value etf coz:

i think the products will not deliver what they promise (i think real value investing can only be done properly in a active manner, with all its flaws)

i dont think i could stand underperformance to the market for a long periode and would abandon the strategy

although i know that the value premium exists for a long time all these factor etfs smells to me like a trend. kind of the story if your hairdresser gives you a stock advice don’t buy it. if everyone opens factor etf to retail investors… by the way with the msci world sc i dont want to grab the small cap premium but rather be invested in the remaining 14% of the market.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

)

)