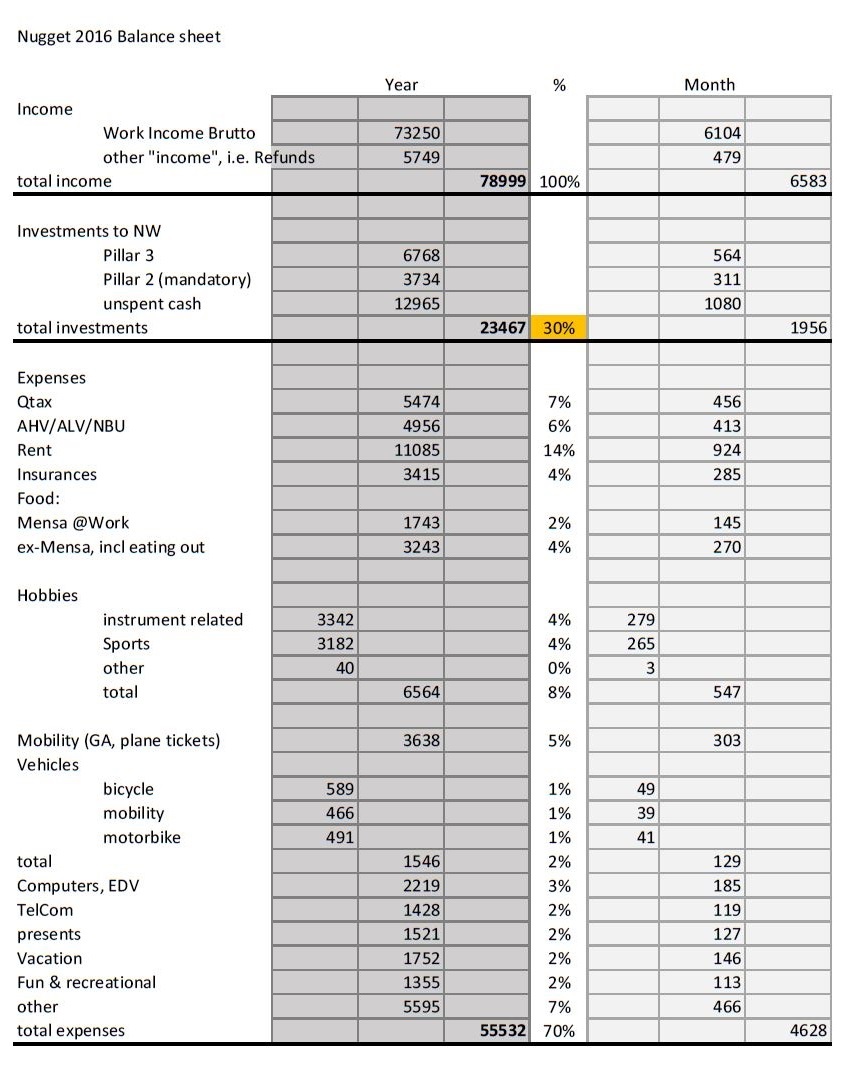

although there are 4 days left until 31.12, this should be the big picture This is a result of my current “get everything you need, then everything you want and save the rest” lifestyle. I am a single Zurich resident, living in a shared flat (“WG”). I am happy to achieve a 30% savings rate! but of course, more is always better… and I think this is a conservative guess:

I listed social security as expenses, although they earn me some social welfare claim.

most of my “other income” is refunds for expenses i did for third parties, but i did not resolve this properly. substracting this from both income and expenses boosts my savings rate!

some people say I should not list taxes and social security as expenses, but rather remove them and use my netto income as reference. this would also increase the savings rate percentage. however, i have my own opinion about this

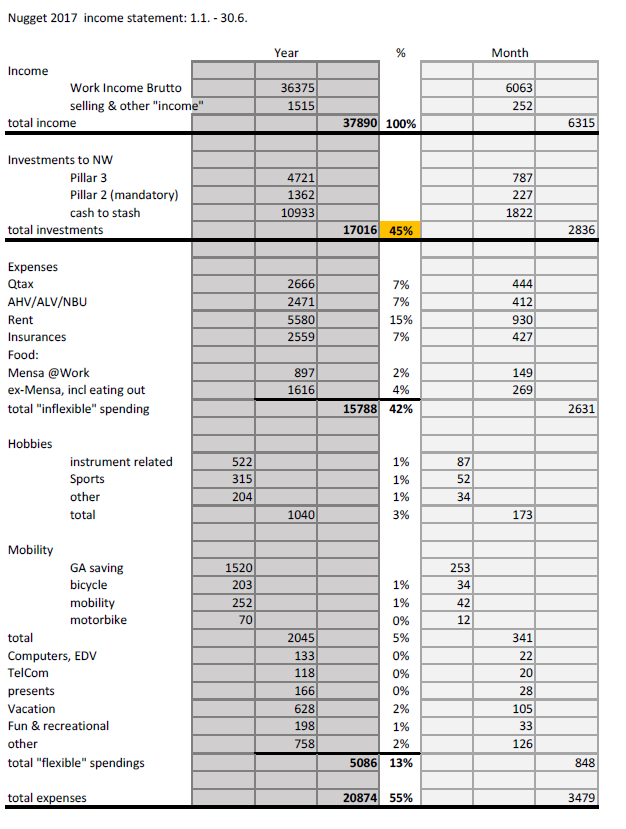

For 2017 I clearly want to reduce some spendings. the big picture is dominated by my swich from being a PhD to (hopefully) working in industry, with 2-3 month of gap time. So the biggest single expenses are quite fixed:

rent: assumed constant

insurances: slight increase because of general healt insurance rate increase

food: should be rather constant. although, every frank spent at the mensa is worth at least 2 francs on hot meals outside of mensa. so once i am exmatriculated, these costs will rise unless my furture employer has a highly subsidized restaurant

mobility & Transportation: unless my future employer provides a GA, i will get another one most probably. almost constant.

Taxes and socual security is going to scale with my future salary and the non-salary in my gap months. hardly any control here, about constant expectation. maybe slight increase.

What I expect to decrease during 2017:

hobbies: 80% of my 2016 spendings were on long lasting equipment. there should be much less next year

computers: not gonna buy another one

presents: holy sh*t, i was not aware i spent that much. well, it’s marrying age in my social surroundings… needs a cut!

bicycle: mine broke beyond repair, and i expect the current one to survive a coupke of years!

wow, this is a substantial increase in spendigs from the time as a student 2007-2012, when I had a yearly budget of EUR 9600, about CHF 11500! well, back then were no taxes, social welfare, insurances, vacation, only rent and mensa

please feel free to comment! Add your balance sheets!

This makes me raise a question : should we calculate the saving rate as the brutto income or of the net (after taxes and contributions)? So far I´d calculate it in percentage of net salary after taxes(because it is really taken before i can do anything), but your document makes me realize that your calculation is based on brutto income. Of course when going from net to brutto the saving rate tends to be quite lower!

And I don´t want to nitpick but, for your financial culture, the document you provided in this topic is more an income statement than a balance sheet (a balance sheet would be a calculation of your net worth, showing your assets on on side and your liabilities on the other one)

Haha you yore right about balance sheet <=> income statement^^ I did mix up these terms quite a few time up to now.

I am not yet sure if I will present the actual balance sheet, anyways i need the pillar 1 and 2 statements for that. they should arrive in January.

about netto & brutto: for me the brutto is a natural choice as a reference. but yeah, nobody has made the codex of savings rate calculation so far

I actually forgot th CHF ~950 I will get back after declaring my taxes. well, let’s include that in next year’s balance!

[edit:] the presented numbers contay the 2015 tax refund, so this should be fine as is. next year is going to be similar. [/edit]

Taxes can’t be (legally, at least ) avoided, so for me it makes more sense to consider the net income to see how the efforts you make impact on your savings…

… and i do not agree that you cannot do anything about taxes there is 3a and other deductible stuff, with Quellensteuer not so much but with normal taxation, there is a lot!

I will clearly stick to using the brutto as reference, everything else is window dressing! Because then I can also substract CHF 500 per month for my rent “because a rent of at least CHF 500 cannot be avoided in ZH”. same with CHF 100/m for groceries, my complete health insurance which legally is not avoidable, since i have the lowest possible already. What other unavoidable expenses do you have?

This way i can easily get a savings rate of 50% and up.

I thought a lot about it lately and I agree that omitting taxes in Saving Rate before there is not much we can do about it is not a good excuse.

On the other hand, what is one of the main use of the saving rate? Knowing approximately when you’ll be able to retire, right?

Then when we want to plug the saving rate in the formulaes (for instance N = 25 (1-SR)/SR ), there is one trap to avoid : these formulaes assume that your expenses are the same after and before retirement.

Are we sure that taxes will be the same after and before retirement? I think it depend a lot about your investment strategy : dividends are taxed as income but capital gains are not (in switzerland at least).

So someone relying on ETFs with high dividends payouts will have to clearly think about taxes in his saving rate. In my case, I already told that I am using a Net-Net strategy, where most of the gains are from capital gains.

In conclusion, it is up to everyone to see how his taxes will be affected after retirement. Because including taxes in Saving rate can lower it of at least 10%, which when you plug it into formulaes, adds a awful (and possibly false) lot of additional years to your estimated retirement date.

Now I think you have a valid point indeed. The SWR caclulation traditionally is done with the netto income. alright, from this perspective, you approach is fully legit!

And on top of that the individual situation: I myself don’t have a clear FIRE goal in my mind, i only want to get “rich” asap^^

In my opinion, there’s not much one can do on the taxes which are somehow “fix” as they get subtracted directly from your monthly income, such as AHV, IV, UV. Other taxes can be optimized (I’ve heard you can claim some deductions from “Quellensteuer” but don’t know the subject).

At the end of the day, apart from our percentuals, what really matters to you is how many CHF you are able to put aside!

so, if i substracted the Taxes and AHV/ALV/BU from my income and spendings, my savings rate goes to 34%. A very unprecize correction of the “expenses” that were refunded and went to “income” it goes to 37%. ther you go

I am still a PhD and will continue until well into 2018, so the big boost in salary has to wait unfortuanately

apart from that, looks like i could successfully boost my savings rate from 30% in 2016 to 45% in the first half of 2017!

whoop whoop!

the trend is clear: my inflexible spendings are almost exactly the same except for the insurances. this is due to the anticipated general increase in premiums towards 2017 for health insurances and that all my yearly premiums apply in the first half of the year.

for my variable spendings, i can proudly look on some optimizations! And to be clear on that: I am highly happy with the way I live my life, and regarding the Fun & recreational category: I was not three times happier about it last year

for those that want me to substract QTax/AHV/ALV/BU from the balance, this math trick would boost my savings rate to 52%^^

and to all who didn’t know me before, I am single around 30 with no kids and i live in a 6 person shared house in zurich, with fantastic ratio of price vs. living standard

Well done @nugget! from 30% to 45% with a PhD salary is quite an improvement!

Somehow you should look for a second income to boost your savings. (just a suggestion )

25 times your annual expenses.

let’s assume you have 5k CHF expenses so 1.2M in investments will buy your time in this earth

How far are you from that?

Choose another country, let’s say Romania, that’s just way too cheap!! compared to Zurich so, you’ll only need Half a million to live for the rest of you life… and buy your time back.

That is why I created this thread. If you know a foreign country particularly well, or plan to spend retirement in another country than Switzerland, feel free to explain why in this topic!

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.