In this case there is no difference. However lots of people have concerns about keeping a huge part of own wealth in US ETFs.

Of course for 3a products you are also not taxed on dividends, but considering that US stocks pay less dividends than stocks from other (developed ?) countries, you don’t win here.

Disclaimer: I am no tax expert and others here are way more qualified than I am to talk about these topics. I also don’t know Finpension funds which I haven’t studied at all.

MSCI USA has a dividend yield of 1.29% - while MSCI Europe has 2.44%.

So you’ll optimise the tax advantage by

going 99% US in pillar 3a, thereby saving 15% withholding tax on every 1.29$ paid out and not “not paying” income tax on 1.29% dividends.

…while shifting your European holdings to a taxable account and paying income tax (at which rate) on a higher 2.44% dividend yield?

PS: I won’t dispute that one of the quotes above suggesting pension fund funds for US exposure was from myself - it just doesn’t seem though-through if/when this increases your share of higher dividend-yielding funds in taxable accounts…

Purely from costs and taxes point of view one should do exactly the opposite - keep only Europe+Japan in 3a and maximize US at IB. But this move is more of a tactical nature. One of the issues is the potential loss of access to US ETFs. Second is that I committed to buy certain developed markets ex US ESG ETF, which wouldn’t be possible if 1 comes true. So I want to buy as much as possible of it now, and for this I increase US allocation in 3a and decrease at IB. If 1 comes true, it would be easy to increase US allocation at IB via options and decrease this allocation at IB. Not very straightforward, but these are my thoughts now.

I noticed that all or most of the index funds offered by Finpension (Index funds – finpension) are accumulating. So in that case, does the dividend yield really matter? I must be missing some point here…

So looking at the index funds available at Finpension one could go for the following fund I suppose?

CSIF (CH) I Equity Europe ex CH ESG Blue ZB CH0507420005

There is also a non ESG variant but seems to perform slightly worse YTD. Note that the ESG one is new so there is no data for previous years in order to compare.

I think it really depends on your portfolio allocation and your personal objectives. I’ve just opened my portfolio today and will transfer only starting in Jan but Ive decided on a single fund (see below) for simplicity like a few others have mentioned already. This is in complement to my 2ème, my existing 3ieme (that is in « gage » for 1 more year) and my FIRE fund that is also only 1 fund for now.

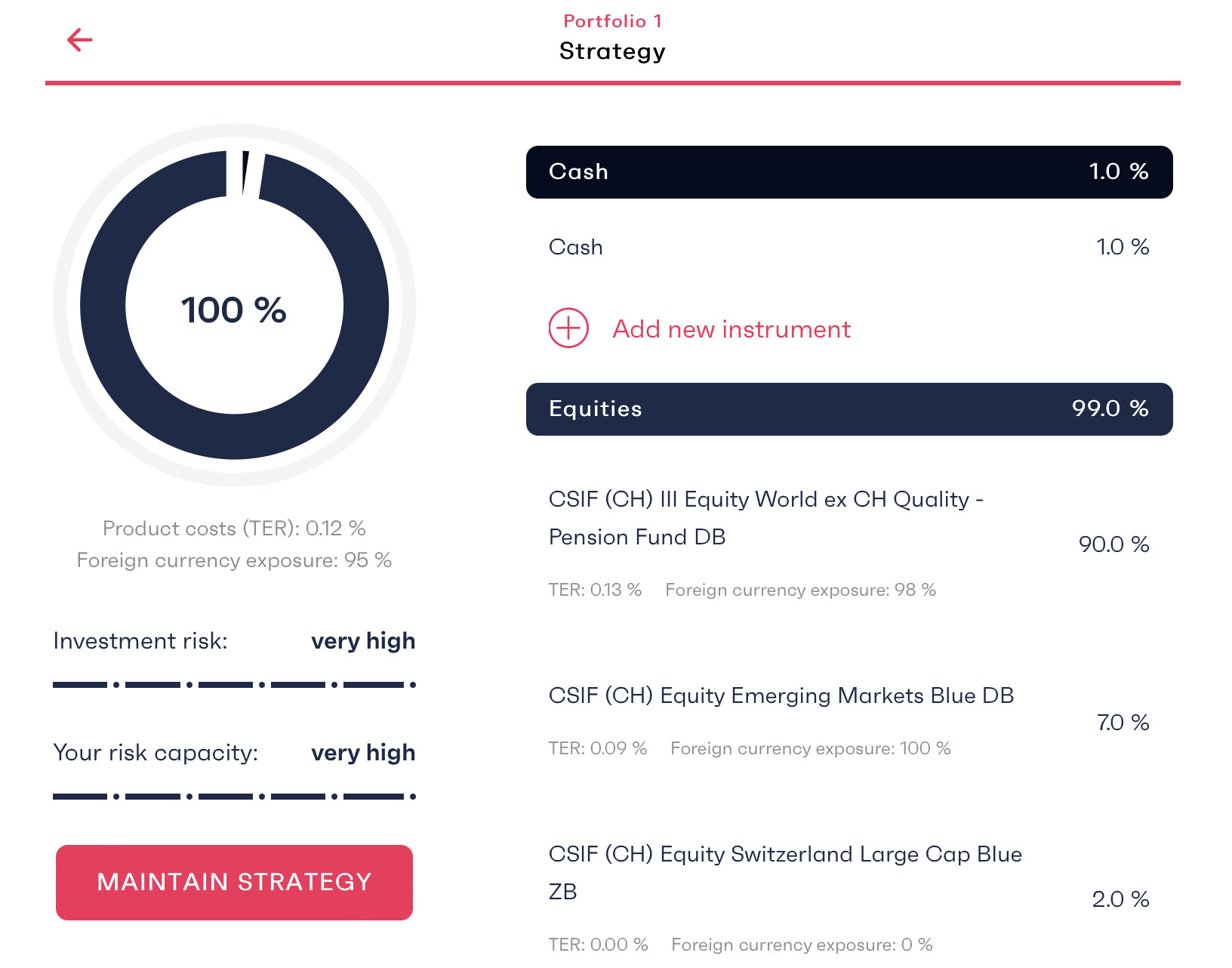

99% fund, 1% cash

I am curious though, what’s the main advantage for the « quality » fund? And to be honest, in my opinion 2% on a 3a portfolio is a bit overkill especially if you have more than 1 account for your 3a overall (just based on +- 6833 chf per year max)

Actually reading other posts, I changed with this one that I am attaching now. this would be my first 3a and I currently have no other investments on other platforms. As for why the Quality I have referred to this post: If I was an index investor

From what I understand there are not so many differences between TER 0.13% and 0.00% compared to the benefit of the quality, then I am ready to receive corrections.

Excellent read, thanks for the link! Really deep exchanges and some parts over my head - but very interesting to have read different views. I like the principle of the quality fund and I may consider having one of my future profiles at Finpension use it to see/compare but 1 fully passive fund in my first portfolio there is easier for me to live with for now.

This is my setup, a lil less expensive but a little more diversified into Switzerland.

Made 29% this year with a one-time lucky purchase (2021 max amount on the 5th October).

I’m a very happy camper so far and I’m seriously thinking about transferring the rest of my 3a from PostFinance75 also to Finpension.

This time next year (2022), I’m hoping to convince my bank to pay out my current 3a depot (that’s invested) on to my two 3a banking accounts with them. They seem to be ok to do it when they release my gage in jan’23.

If confirmed, it would allow me to both transfer a majority to the fund i mentioned already and maybe a smaller portion on the quality index…something to consider if it works out how I want.

Between my 3a and my wife’s 3a being transferred it could be a way to be slightly more aggressive for 10years on a very similar approach.

if it’s only on one, I’d stick with the main fund I mentioned above and maybe use the quality to start a new portfolio from scratch.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.