With lower fees and no currency exchange fees, this solution is better than VIAC. I have started the process to move my funds from VIAC.

In short, you can replicate the VT fund for around 0.42% in your 3a.

An other way would be to have only “CSIF (CH) III Equity US Blue - Pension Fund ZB”. With this fund you would avoid withholding taxes. You could take VXUS in your non-3a account and thus replicate a MSCI World.

How about being patient for a month or two - I am sure VIAC (and others) will adjust their offers as they see competition stepping in.

Instead of jumping from one to another every few months as they compete…

Btw this is great!

Happy to see things developing.

Btw2 which organization/bank is behind them?

Edit: Ah I see: Custody bank - Credit Suisse (Schweiz) AG

Yes, I haven’t invested my 3a this year yet. If I had to invest right now, I would probably keep VIAC and just invest this years 3a limit with finpension.

The missing currency exchange fee isn’t an advantage for the already invested funds because I already paid the fee with VIAC. Then the funds are not invested for a whole month, missing around 0.5% of expected returns.

At the moment it is clearly a better offer than VIAC, so I hope VIAC is forced to compete.

Incidentally, this is the reason I still don’t have a VIAC account. Back then when the forum was full of referral codes, I refused to do it since they didn’t have a Web interface.

Deposit insurance is particularly relevant when cash solutions are offered. In this case, the bank where the cash is held must be checked in detail (Credit Suisse in our case).

As we don’t depend on a bank, we don’t offer cash account solutions. For this reason, the investments with us are not affected in the event of bankruptcy of the bank (99% of your assets are invested and not part of the bank balance sheet).

3a foundations are not permitted to conduct their own balance sheet transactions and are managed by a separate company (finpension AG). Consequently, only client funds are held in the 3a foundation. This is a regulatory requirement to ensure maximum security for the insured.

finpension is already well established in the area of 1e plans and vested benefits. Many innovative and reputable companies have chosen our solutions (some references are listed on www.finpension.ch).

Thank you very much for coming here to explain how your promising 3A solution works

I’m taking a look at your strategies, in particular Equity 100.

First question: in your overview for 3A funds I see this:

While the funds you invest in are all quoted in CHF. When does a currency conversion come in play?

Second (but maybe you’re not the right person to ask to): why Credit Suisse offers funds with 0% TER? Is there anything hidden? Extra costs on their side?

Inside the fund directly, like an ETF which is quoted in CHF but covers the US/world

The TER is zero (like for VIAC), because a contract has been done between Finpension and CS for the fees. These fees are coved by the 0.39% all in fees.

No this is not correct. It’s not the Bank account that is covered up to 100k but each customer’s cash assets. In case there is a problem with CS, each individual customer has thee deposit insurance priviledge of 100k. You can read about this in the "Mitteilung über die berufliche Vorsorge Nr. 139 on page 3 (https://sozialversicherungen.admin.ch/de/d/6604/download; unfortunaltey only available in German).

The management company finpension AG and the retirement savings foundation have to be completely separated. We want to give our clients as much as possible flexibility regarding the investment strategies but there are also some restrictions of course because of our investment regulations. You will see this in the app if you customize a strategy (eg. restrictions for Swiss equities because of the single stock limits, limit of the gold allocation etc).

KYC has no effect on a pension foundation because you become a customer of the foundation and not of the bank. We would like to make UX as good as possible and therefore do without it. An ID check is only required when a payout is made.

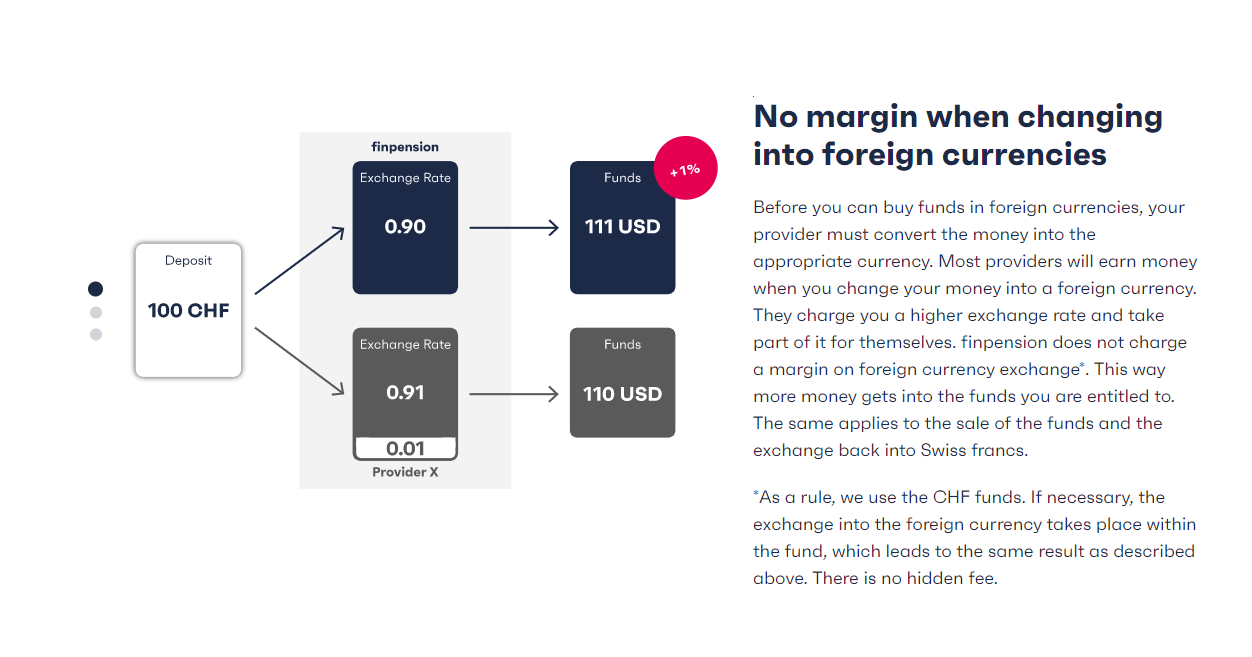

We use CHF index fonds whenever available. There is an exception if you customize your strategy and add for example CSIF (CH) III Equity US Blue - Pension Fund ZB as we have to subscribe this index fund in USD. Otherwise, there is no currency conversion. If there is one, we have a spread of 0.05% which is charged by our bank but there is no margin on our side.

0% TER classes can only be subscribed if you have a special agreement with the bank (institutional fund access; such agreements are usually only set-up for very large accounts). The costs for the use of this classes, custody and transaction fees are then directly paid by the couterparty (finpension) and not charged on the index funds. This is the reason why we can offer an “All-in-Fee”.

We found it important for security reasons to completely separate the 3a foundation from the management company so that we only have the client assets in the 3a foundation. Consequently, our fees are invoiced directly by the management company which has to pay VAT. I know that some other foundation have a bit a mixed set-up but cannot give you a final answer about how the mentioned providers handle this.

The currency exchange fee for 3a for VIAC is 0.75% and for vested benefit is 0.5% charged by WIR bank. This is a hidden fee and I only found out by accident.

Ofcourse this could reduce when they do netting and have to buy less USD.

You will have to pay the fee when you buy in and exit… so kind-of sick

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.