It’s not black and white. CVS announced closure of what, 1000 stores? Mix of experimental or trashy locations, lack of inventory, true high shoplifting, going-out-of-business-location. When there is money to be made in retail, they would have stock and display. Maybe that neighborhoud is unsafe and was picked for clicks, out of the other which will be shutting down soon.

I expect US to continue leading long term, regardless which too-old-to-govern person is president. Is it declining from peak? Sure. Is anything else ready in next 10 years to take over leadership? Not so, IMHO.

Edit: Reminds me of a quote I read in FT comments recently - dont bet against he US economy and the swiss franc.

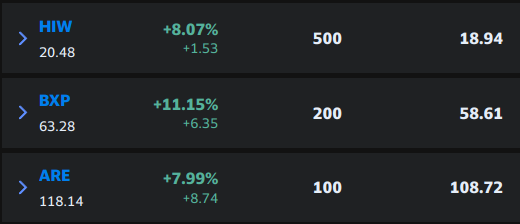

I like ARE, too (and incidently bought my latest tranche on Nov 30 for $109.29 … … I don’t like bragging about it, though, as this will inevitably jinx the valuation since the market (timing) gods consequently punish anyone challenging them vocally).

I like ARE because

they’re still (slightly, ~5%) growing their Adjusted Funds From Operations (AFFO)

they’ve steadily grown their dividend since 2010 at a nice cliff (10% CAGR over 12 years, about 6% in the past 5 years), currently yielding just above 4%. Going forward I would expect them to grow the dividend at the rate they can grow AFFO, i.e. ~5%.

they seemed just about fairly valued around $110

they are a niche Office REIT that owns collaborative life science office space: them getting lumped in with the Office REIT GICS sub-industry helped with Mr. Market taking their valuation down because of the WFH-makes-office-space-superfluous narrative, while in practice the ARE tenants actually need to do most of their work in the office as that is where the lab equipment necessary for doing the work is located

I like neither HIW nor BXP, though. Even if they look undervalued both feature no (AFFO) growth and froze their dividend (admittedly probably a good idea given they can’t grow their funds from operations).

Perhaps a nice bet for the market (and/or Office REITs) bouncing back short term, but - for me at least - not a long term investment.

I dithered a bit too much on this. They are all about 20% up (or more) when I figured they were oversold. I have to agree with you on ARE and also the HIW/BXP scepticism.

I’m still don’t like buying REITs at this stage as I’d rather buy them in a post-capitulation market. But I figured that even though I feel the big crash is coming, there’s no way to really guarantee when that will come and I figured you could still earn money holding through the tough patch.

While I agree that everything is set for stocks to run up further, we also know that sentiment can also turn on a dime. But as one commentator said previously “while the music keeps playing, we have to keep dancing”.

VIX is surprisingly low given the potential for big movements in either direction.

The bottom is in. Powell just spiked the punch bowl and started the after-party. I’ve been waiting years for the melt-up to happen and it feels like Powell just fired the starting gun for the mother-of-all melt-ups. I just wish I’d closed my SPY short before his speech!

I’m just stunned. I thought he’d do his usual push back to stop markets getting ahead of themselves, but he was just limp. How can this not trigger a massive santa rally?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.