The issue with that Munger comment is whether some of the businesses you mention (AAPL, MSFT) will indeed have that profitability for the 20-30 years to come. My opinion: best case, they might look something like IBM, worst case, something like Sun Micro. Unless if you are capable of actively trading that and sell at the right time, better stick to indexes on the long run.

3 Likes

I assure you it is a contrarian indicator meaning that you are climbing the wall of worries. If you would see yourself swimming in gold, I would start worrying.

We are not following the same bonds. iShares Swiss Domestic Government Bond 7-15 ETF is still mostly down, and going flat and downish:

1 Like

Interesting points. ![]()

As always, the unanswered question is “When?”

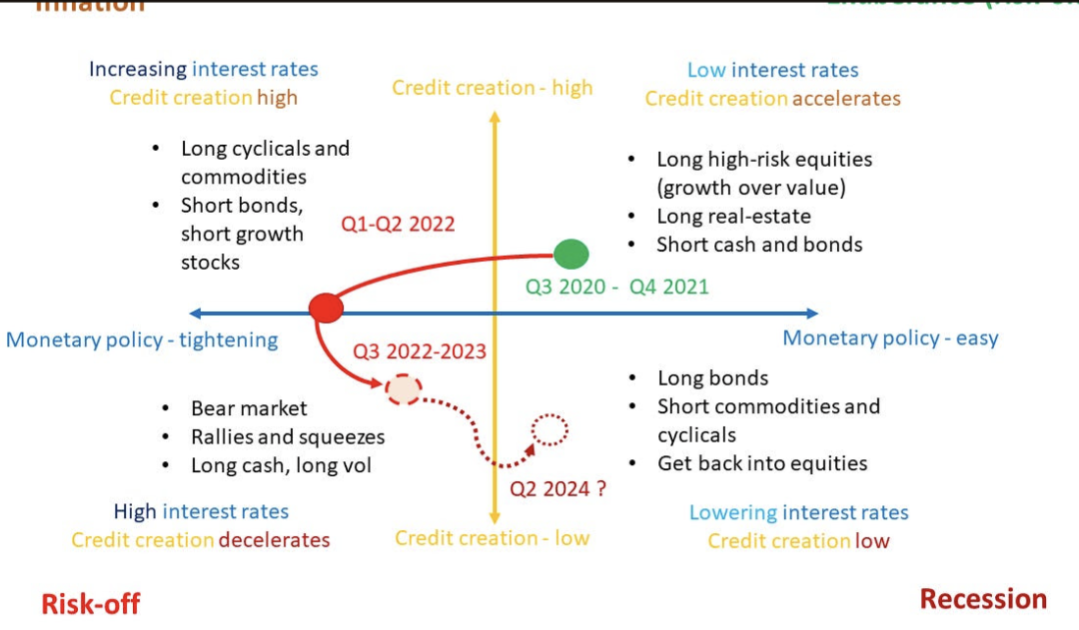

I’ve also seen some interesting cycle timelines like this:

What’s the opinion on this view?

Where does this “rule” come from? ![]()

1 Like

The 30-70% looks close to Benjamin Graham’s: “the investor should never have less than 25% or more than 75% of his funds in common stocks.”

I would selectively count or not count my pillar 2 assets for the purposes of this rule, depending of how I assess my temperament in regards to holding my allocation during a downturn. I’d think what matters psychologically during a downturn is what we look at. If we look at our total net worth, then that’s the number to use for me. If seeing a part of our portfolio ((one of) our brokerage account(s)) going down causes us turmoil too, then it may be worth it to be more conservative and assess our risk tolerance on that part of our portfolio more than only on the whole. My own personal view based on my assessed own temperament is to take a holistic approach and count everything, including pillar 2, in my allocation.

I understand the purpose of your post and I salute it, the time to assess our risk tolerance and eventually adjust our allocation is now, before taking the plunge, and not when deep under water and grasping for air, but I’d underscore that what you seem to be talking about is adjusting our actual allocation, for the long term, not timing the next deep and prolonged downturn, which we may already be in and going or which may occur in 2-3-5-10+ years (but will most probably occur at some point, potentially without warning, so we should be ready).

3 Likes

I don’t rule out a final rally in the next 12 months. I was 60/40, but now at 70/30 as I got too tempted and bought some stocks as they trended lower the last few weeks.

Guess this it where it comes from, indeed. Thanks for that link! ![]()

I suppose the best strategy those days is to split the typical monthly buy in 4 weekly task. A DCA of a DCA if you prefer ![]()

ES already broke support. If it’s not just a deviation, 87 coming for VT

I wish I’d shorted more yesterday!

2 Likes

it always like that ![]() if today was going to revert, you could have said, fortunately I didn’t short much.

if today was going to revert, you could have said, fortunately I didn’t short much.

If you stick to your plan with the right size, SL and TP then you are good

2 Likes

Yes. I was hoping for a bounce to short some more ![]()

Boughts some MO today too. Not a big fan of the management of MO, but hopefully they learned the lessons of the last few tragic acquisitions and do no more silly deals.

So I know that “Time in the market” > “Timing the market” but for someone that has quite some money in the bank (i.e. way more than needed for emergency fund) and is starting investing more actively/seriously now, what are your guys thoughts on the current state of the market?

I have been buying some shares and filling my 3rd pillar but numbers only go down, which is fine, I understand that the strategy only makes sense long term (see beginning of post) but would you start/keep buying now, or hold off with the money in some savings account and wait for better times.

Again I know it’s all wizardry ![]() and nobody actually “knows” but what are your thoughts/arguments. Apologies if this is not the right post but it seems to fit the title.

and nobody actually “knows” but what are your thoughts/arguments. Apologies if this is not the right post but it seems to fit the title.

I’d say this is a very good time to actually experience what your risk tolerance is, so I’d invest the money you can afford to loose right now at your self-assessed target asset allocation.

The earlier the experiences are done, the bigger the expected returns of the knowledge gained and the lower their costs.

6 Likes

Just bought some monthly VT ![]()

It will go down again next week, but it’s fine. That’s mean I will buy more shares next month !

6 Likes

To sum up: Risk parity portfolios start shining, eh ![]()

Rough numbers:

- ~100k CHF in the bank (about 75k CHF now in savings account).

- ~20k invested in 3a with Finnpension. Red.

- ~10k invested in crypto (mostly BTC) Green.

- ~10k invested with Selma (since 2021) Red.

- ~2k invested with IBKR (started last month) -

Some notes. I am aware that the amount that I have in the bank is, let’s say, sub-optimal. I’m keeping a high liquidity because I might need them for a Real Estate deal in my home country. Nothing is lined up or even close, just something that me and my partner are semi actively looking into. I could invest them in IBKR and sell them if needed in 6months/1year but the way things are going it’s probably best to leave them in the bank, especially in CHF. It’s also not 100% needed, it would just decrease the amount that we would need to loan out, which given the current rates in the eurozone we want to minimise.

Selma is how I first invested, quite a bit in the red at this stage but such is the market. Haven’t really touched it since 2021. The plan is to use IBKR now. I could probably lump sum about 10/20k there + 1-2k per month. That’s is in line with what I said above.

The crypto investments I wouldn’t touch. I understand that it has a much higher % than it should in my portfolio but that’s just because where I started. If we look at what came out of my bank account it was actually a rather small amount.

I understand the idea but I’m not sure if I fully agree. Disclaimer I’m still very much new to investing so I’m probably wrong on most things, but here are my thoughts.

I wouldn’t say I have the highest risk tolerance (hence the initial question) but also definitely not the lowest/low. From my side at least there’s a difference in trying to time the market by selling/buying somewhat frequently (which I’m not planning to do) vs choosing a time or times to enter the market which is basically what I am asking about.

In the same note I also find it easier to hold while the market is in a down trend than to jump in at said time, especially when it seems like it just will keep going that way (so not necessarily to buy the dip). I have kept what I had at Selma and kept buying in to 3a even though both were very much in the red almost from the start ![]() . From crypto due to luck in timing I was very much always in the green, even though how much varied, greatly considering the crashes it had. I first bought in 2017 so it has been quite a ride, but considering I was basically always green it wasn’t that bad tbh.

. From crypto due to luck in timing I was very much always in the green, even though how much varied, greatly considering the crashes it had. I first bought in 2017 so it has been quite a ride, but considering I was basically always green it wasn’t that bad tbh.

1 Like

To be transparent. I started investing with SELMA too. In April 2021, I decided to invest on my own by choosing one of the most popular ETFs and implementing a simple, passive strategy: invest X amount every month on day X regardless of the market situation. I also apply this strategy to my 3a and to crypto.

In 2021, I followed this plan to the letter, except for the 3a account where I lumped the entire amount on the first working day of 2021 (as a test).

Then in 2022, nothing went according to plan. Because of a difficult personal situation, I preferred to invest in myself and keep some money in a bank account. It was only at the end of the year that I took some of my funds out of the bank and put them into my 3a.

In 2023, I reimbursed myself the funds taken from the bank, and then I put my strategy back in place: DCA on IBKR, 3a, crypto. And I have to say that even if the market is fickle, I feel very free. I’m devoting more time to myself: sport, couple, friends, training, work.

If I didn’t stick to my plan, I’d be asking myself every day: what am I going to do with the money in the bank? Do I buy a car? A new PC? Do I lump sum now?

By automating my investments, I don’t ask myself this question any more, I take advantage of the market as it rises or falls and of the dividends that allow me to buy more and more.

I personally feel free by doing this and I can devote more time to the present moment.

Last info: IBKR = red, Crypto= red, 3a= green.

5 Likes

Depending on how serious you are about finding an opportunity in that direction, that would be shorter term money for me, so savings account or very conservative investments, in the currency of the prospective loan/asset expenditure.

The alternative is to consider investing more aggressively an opportunity cost for that purchase and to either accept the potentially higher borrowing costs at the time you will make that real estate purchase and/or taking invested money out when it has lost some or possibly a huge chunk of value.

I’m dealing with a lesser investable amount than you do and had adopted the later positioning. I’ve gotten out of the market at the point where enduring further losses would have endangered a real estate deal I am interested in (though that happened just one month before closing).

One of the important things in investing, which I believe you understand, based on how you formulate your thoughts, is that you’ll be alone to deal with the consequences of your decisions: none of us will loose any money because of it. Being able to minimize regrets and live with the consequences of our own decisions is an important trait for a successful investing career. I would tend to trust myself over others when it comes to deciding whether I have enough information or not to feel confident, and to pursue the investments I want to pursue when I do feel confident enough, as long as failure won’t put me in a desperate spot where I wouldn’t see a possibility for a good outcome anymore.

This is kind of the point I was trying to make: no matter your decision, chances are you will make “mistakes” and experience losses, either direct (the market falls and you were invested) or indirect (you were standing on the sidelines and everybody else’s assets are skyrocketting as the market did rebounce). I find important to get enough exposure to that early enough so as to get a better feel of what my actual risk tolerance looks like as early as I can. That, to me, is worth loosing a chunk of my initial investment (which was less significant than yours is), going into the market with my eyes open on the fact that I am taking risks that may result in a loss of money, but a gain in experience.

You seem to have some exposure to that already and only you can assess how much learning about yourself you are already doing, what more learning being more invested could bring and what degree of losses, if any, that could be worth for you. You might be invested adequately relative to your goals, including the real estate one. If that is the case, then my comment doesn’t apply to you: you are aldready doing fine on that regard.

You have mentioned a partner in your message. I would also make sure you both are on the same page before making my final decision. They might have a more conservative or a more aggressive temperament than you do, that can impact your investing decisions, in particular whether the money you expect to use for real estate in a few years can be invested at all or should be kept conservatively.

5 Likes