Thank you Bojack.

I thought along the same lines and kept the decision for 3 funds combo vs. 2 or even 1.

But that discussion is somewhat off-topic.

I now see that my original question was possibly unclear.

It went more along the lines of whether choosing something like iShares (non-US domicile) versus Vanguard/Schwab US-domiciled funds brings any added benefits (e.g. such as tax sorting simplicity) for their higher TERs tradeoff.

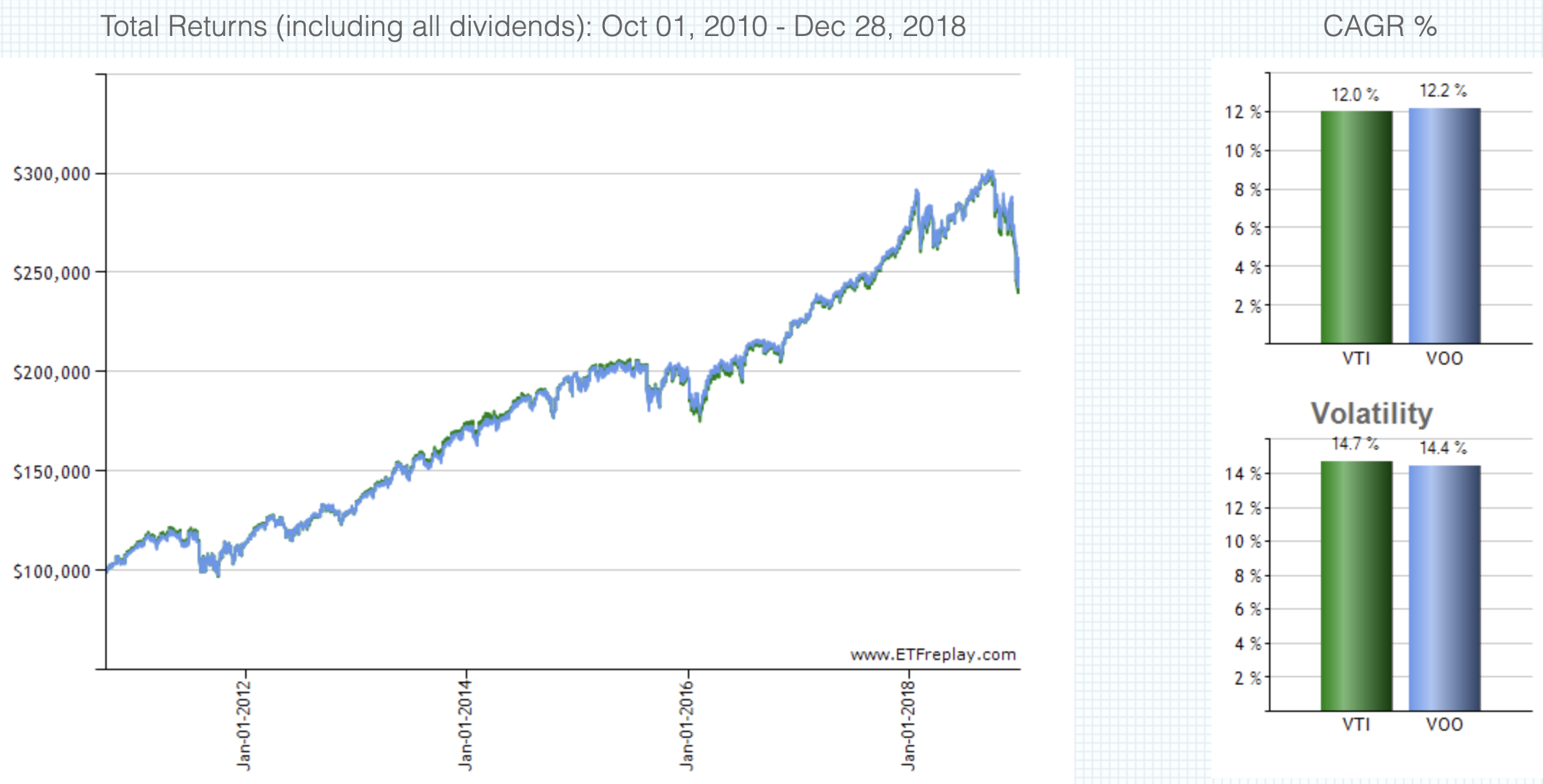

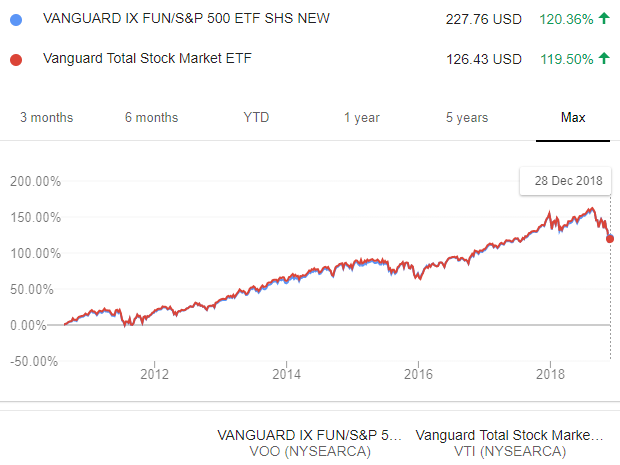

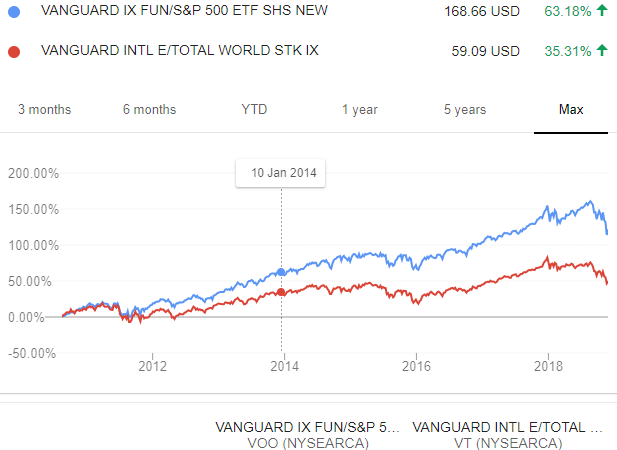

Btw I just compared VOO to VT, VTI and VXUS on Vanguards website. Even before the latest downturn, VOO outperformed all others with almost double the annual return rate since inception. It also has the lowest TER (same as VTI)

I dont see much of a reason to invest in anything ex-US … I do not see how they should perform better than the US stock market in the future.

The US might be screwed with their high debt to GDP ratio but so is everyone else

I am a beginner with investing.

As far as my research on index funds and what I understand from the different graphs and numbers,(Google finance mostly) I agree with oozoo on VOO being the best choice on ETF because:

it outperformed most other index ( except for market niches like Medical field for example)

if the SP500 goes down, it’s very likely everything else will follow ( medical, IT, real estate, consumer goods etc)

The SPX500 wiki page has an annualized return table. On the long run: 25 years it averages 11.93% with the low of 9.15% ( worst case scenario)

However, I’ve seen a lot of discussions on the forum, people opt for different ETFs like the VT.

Can someone explain what I’m missing here ?

Thank you,

People opt for something like VT because it follows a world index. You invest in the total market, not only US. More diversification, less risk.

It’s true that VOO / US has outperformed World / VT in recent years, but what is to say that will continue? Nobody knows that’s why people diversify.

Take the S&P performance with a grain of salt though. For the swiss investor earning his salary in CHF and living of CHF, one should account for the exchange rate CHF/USD. Look at CHF/USD for the last 25 years and suddenly VOO doesn’t look that good anymore.

You’re right about the exchange rate, I never looked at that on a 25 years time-frame: the $ fell from 1.5 CHF to about 1:1.

Also, in 1975 1$ was 2.5 CHF

Also, I found a site to calculate average inflation between 1993 and today: looks like the $ averaged 2.3% per year while the CHF 0.7% py.

If I purchase the VT is USD, what difference does it make compared to VOO ?

VOO is 75% of VTI. The remaining 25% are the remaining mid & small caps. Thus, you get a better penetration at the same cost.

What I don’t get is that according to etfreplay.com, the total return of both ETFs has been identical. I would expect VTI to slightly outperform VOO. Where did you get your data about VOO outperforming VTI?

Speaking of world vs US vs SP500, we already had that discussion multiple times, e.g.:

Tl;dr There were periods when ex-US outperformed US. Nobody knows if US will continue outperforming the rest. Some people think it will - like John Bogle; others don’t - like Burton Malkiel. Choose your bet yourself.

This was directly from Vanguards website. Their calculator stops in September however.

You are right, VTI and VOO are very similar in performance (the calculation since inception is a bit scewed since VOO was established in 2010 only), however VT & especially VXUS are not.

VTI is more diversified compared to VOO, it does make sense to change VOO for VTI

Can’t understand why people prefer VT.

Good point there 1000000CHF, maybe India and China will have increased economic growth in the next years compared to the US

However, the US has a diversified economy relaying on both foreign investments in the US and US investments in foreign countries

Past Performance Is Not Indicative Of Future Results. Especially Long Term. Example: Nikkei.

That’s the point. It’s a bet whether US will continue to outperform long term. Since most of us, are investors for very long term, we prefer to stay on the safe side and diversify the risk of US going into dogs in the distant future. We’re not traders, we don’t switch back and forth between allocations. We’re not chasing performance from one asset class to another bitcoin.

I would like to ask for help / your opinions on the following situation:

I’ve arrived in Switzerland at about 2 years ago and I’m planning to leave in 18 years (or before if possible). I’m 32 years old.

Currently I’ve my portfolio in my home country, where capital gains are taxed at 28%. Over there we use Acc ETF’s (widely seen as more tax efficient) so we don’t get taxed on the dividends (on our side).

In consequence, my fiscal address is now a Swiss one and in my country, my fiscal status is as “Non Resident”. In this situation, do I need to declare something to the Swiss Authorities? Like which ETF I do own, etc?

Also, I’m wondering about moving a part/most of that portfolio to Switzerland so I can benefit from the capital gains not being taxed. Would you consider that, for an 18 years period?

My intention is to “retire” out of Switzerland.

I’ll be seeing a fiduciary next week, but I would love to have others informed opinions.

Yes, you need to provide an itemized list of all worldwide assets in your possesion, since Switzerland has wealth tax instead of capital gains tax.

Double check if you trigger the capital gains by selling even if you are no longer a resident. Your home country may want to tax you based on where you were when and where the capital gain happened, not when it was realized (sale).

In any case, now that you are in Switzerland I recommend you open an account with IB and not an European broker, so that you can invest in US based ETFs (for cost and tax reasons).

I’ve been reading the introduction of this topic again. I thought that I would only be taxed on my “wealth”. I mean, after having declared all the assets in my possession, the Swiss Administration would apply a tax (annually) and that would be all.

But now, and for example I own shares of the IWDA ETF, I think that they will also tax the dividends that the found receive and will automatically reinvest. Am I (unfortunately), right?

If that’s that case, I think I’ll be better off having all my investments transferred to a new account, opened in Switzerland. In fact, my country tax capital gains for non residents at 28% as well. If I leave the assets over there, I’ll be paying taxes on the dividends to the Swiss Administration, and taxes on capital gains to my country. I would say that’s the “worst” of both worlds.

If for US stock the best are US domiciled ETFs, and for EU stocks the best are non-US domiciled ETFs, what do you think of using: 50% VTI + 40% XD5E (LU0846194776) + 10% sth in Asia?

Advantages I see:

effective 0% L1TW and L2TW on US stock

very low (0.03%) TER for US stock

decent (0.12%) TER of distributing XD5E built of EU stock which anyway would be highly represented in All-World ETFs (VT)

I am not sure how L1TW and L2TW looks like for Luxemburg domiciled fund made of EU shares, but supposedly better than VXUS, right?

Any suggestions for the Asia part - a distributing, non-US domiciled funds with low TER?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

{kind=link}