Ah ok thanks So it includes savings from monthly salaries.

At first I thought this was just progression of already invested money and seeing it growing 50% I was reall thinking… what did I get wrong with ETFs giving an avg. of 10% yearly? Or are these guys going wild with high volatile investments? But that is not considered wise for FIRE.

It could be any of the mixes of those.

Crypto jumps, bonus payouts, RE reevaluations etc.

It serves as a solid motivation, don’t get overly involved in comparisons.

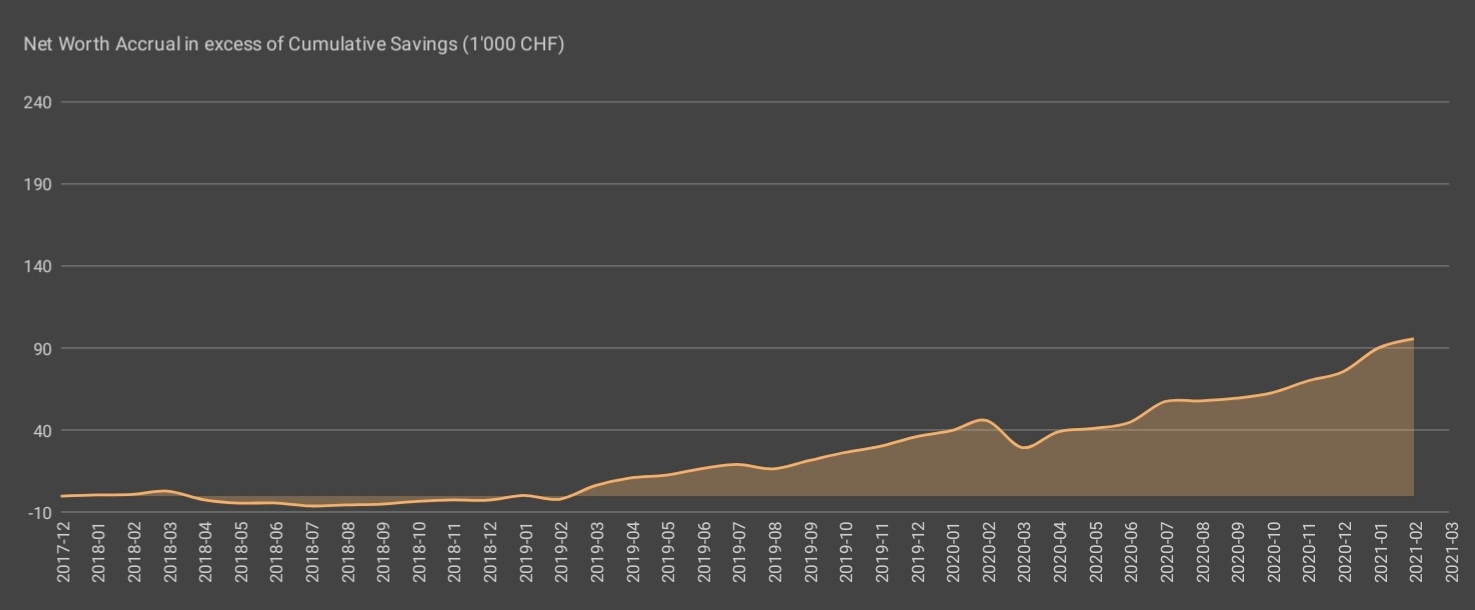

I am myself trying to track NW accummulation vs. just pure savings, to gauge how much being invested has contributed to it.

Looks a little something like this.

Started investing “properly” only with beginning of 2019, and the effect of it is markedly clear. (With 2 lucky strong years of course)

@dbu as said by @weirded, that is exactly what I had in mind.

Savings can differ per month or during the year, think bonus, taxes, unexpected expenses. It is interesting to see what amount was pumped in, and what was gained due to market.

Unfortunately, I have not tracked like this for the past 20 years of data I have…

This point came to my wife after I mapped all my net worth, divided by asset category. She asked me if my portfolio was “biting the market” or what was the performance of my assets… I can’t say, as I cannot separate growth due performance from those due to savings (net new money).

Hi,

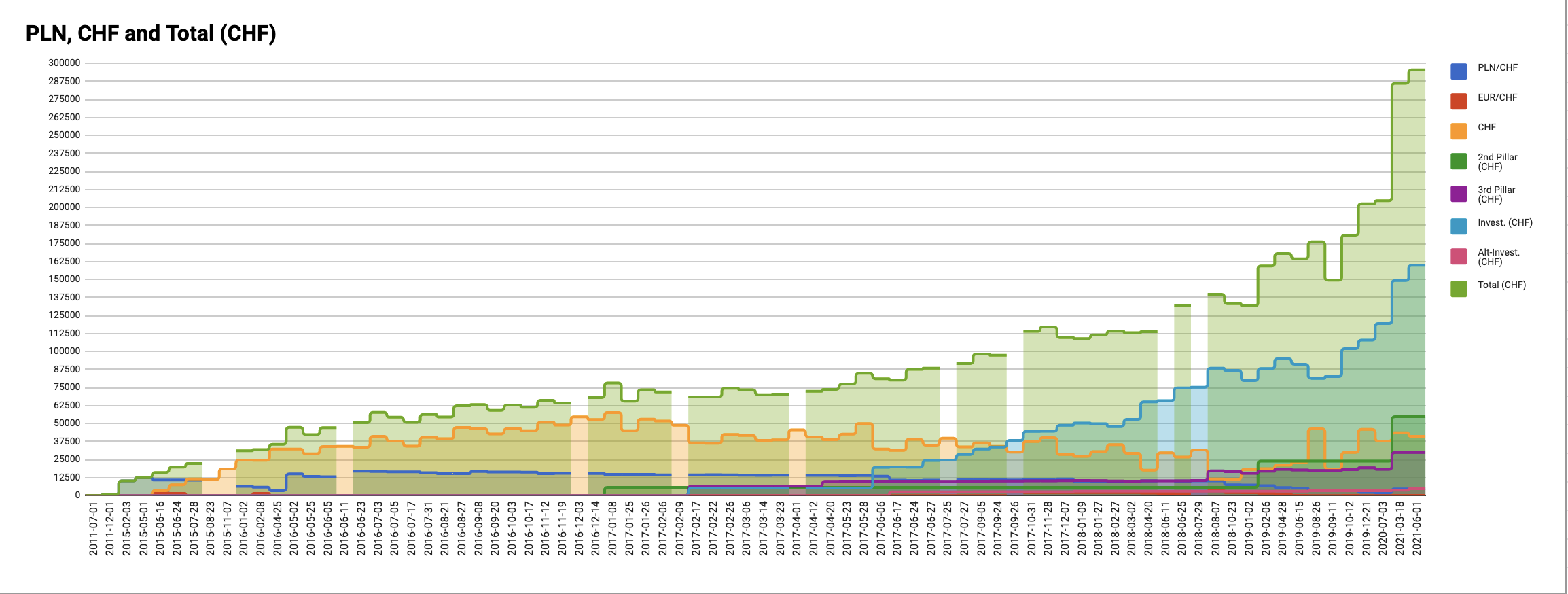

I’ve also noticed that the various graphs don’t take in consideration the currency exchange.

For example if I have 60k USD in stock A and 55K CHF in stock B, in the graphs it will show that Stock A has more % weight on my portfolio, due to the absolute value taken in consideration

Hey @danfaiz

Funny because I updated the sheet yesterday, specifically to fix this issue. Now the charts in the “Stocks” and “Crypto” tabs show the values converted in CHF. Check it and tell me if it’s what you wanted

Anyway, thanks for the feedback!

Thanks to you for the work!

Regarding the YTD % I am not sure to understand the formula, if you dont mind explaining?

As there is “net worth on 1st of January” (B31), I guess the whole column B for your January net worth, is to be filled up at the end of the month.

To make thing easier with number, if I start the year with 10chf (B31), and at the end of January I Have 15 chf, my YTD % increased of 50% (B29/B31).

But if at the end of February if have 20 chf, I should have an increase of 100% of my networth, but with your formula (C29/B26) it shows 66%

shouldn’t u always divide every YTD month by the B31?

An other little feedback: as the currency fluctuate, I actually do the exchange on that given day at the end of the month index(GOOGLEFINANCE("CHFEUR","price","2020/01/31"),2,2)

Or, if I use the automatic today date with the standard googlefinance("CHFEUR") formula, I will then “freeze” the cell value at the end of the month, by copying and pasting just the value of the cell, so my graph doesn’t change in time and I know exactly how much I really had at the end of that month

You’re totally right, it was a bug! Thanks for finding it and notifying me! The sheet is updated now.

And regarding your last remark, you’re right as well. The way the sheet works now, we’ll see old net worth values change slightly because of the exchange rate. Your suggestion will fix this, but it’ll add complexity to the sheet (have to change things if we use it next year, and stuff like this). I have to think of a way to make it work in an easy way. We can discuss this in pm, as I’m not sure it is interesting for everyone here.

Btw, the sheet is currently in french. If someone is interested to have it in English, please like this post, so that I know and can start the translation

Since you snapshot it just once a month, why even introduce complexity with having “live” forex rates?

(I don’t see how it would “add complexity”, as you state, to remove the currency conversion )

What I do is just literally google “X eur to chf” (or whatever your base tracking currency is) on the date of data entry, and put that into the sheet.

Then maybe keep another column which tags the original account currency (EUR/CHF/USD).

I meant that adding currency exchange for a specific date would add complexity when one wants to reuse the sheet for another year for example. Of course, removing the currency conversion remove complexity ahah. What I did in my previous sheet is that I have a cell in my sheet that converts currency X to currency Y, then I type the CHF value in the cell, as you said. It’s the easiest, I agree on this!

I did not. Only reevaluate it when informing the Bank that I will rent it out. Value increased and they decrease the amortization from 7k to 4k annually, as the apartment was evaluated for 250k more than I bought it 7 years ago.

As each sheet would be valid for a certain year anyway, you can add the reference to the year in a specific cell (e.g. in the first) tab and then embed it in the index formula which @danfaiz pointed out to make it more abstract / reusable

It’s not March but July last year, so it’s basically a year difference (I haven’t been updating my sheet because I wasn’t investing for a year - I got a little bit scared and a little bit confused with my life situation). And it’s not 600k, but 90k - jump from 204k to 295k.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.

So it includes savings from monthly salaries.

So it includes savings from monthly salaries.