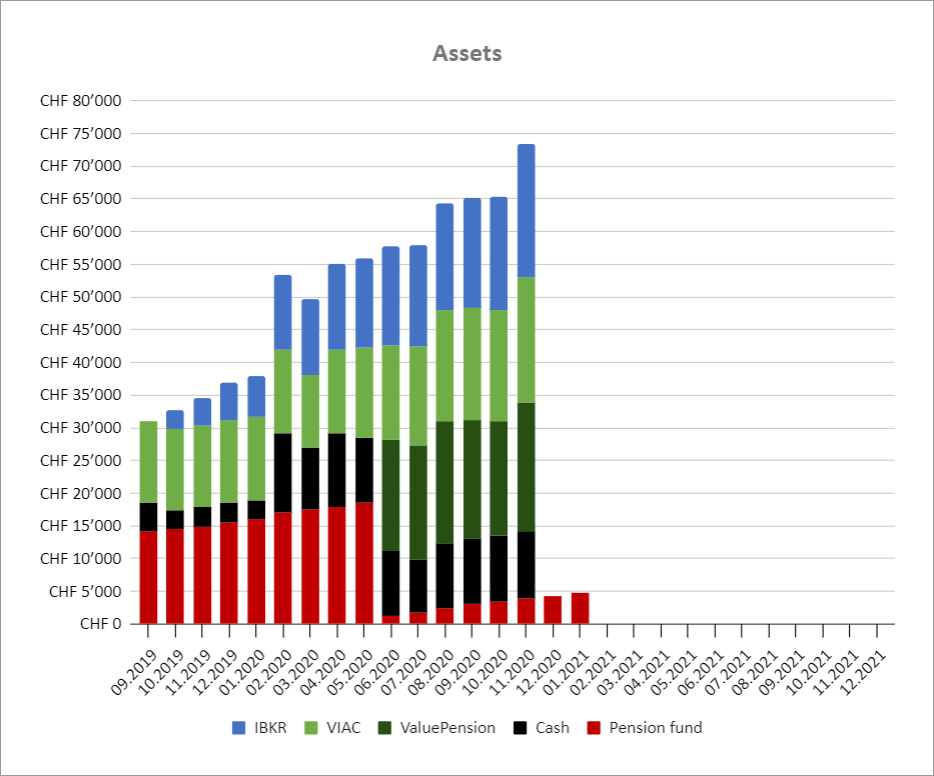

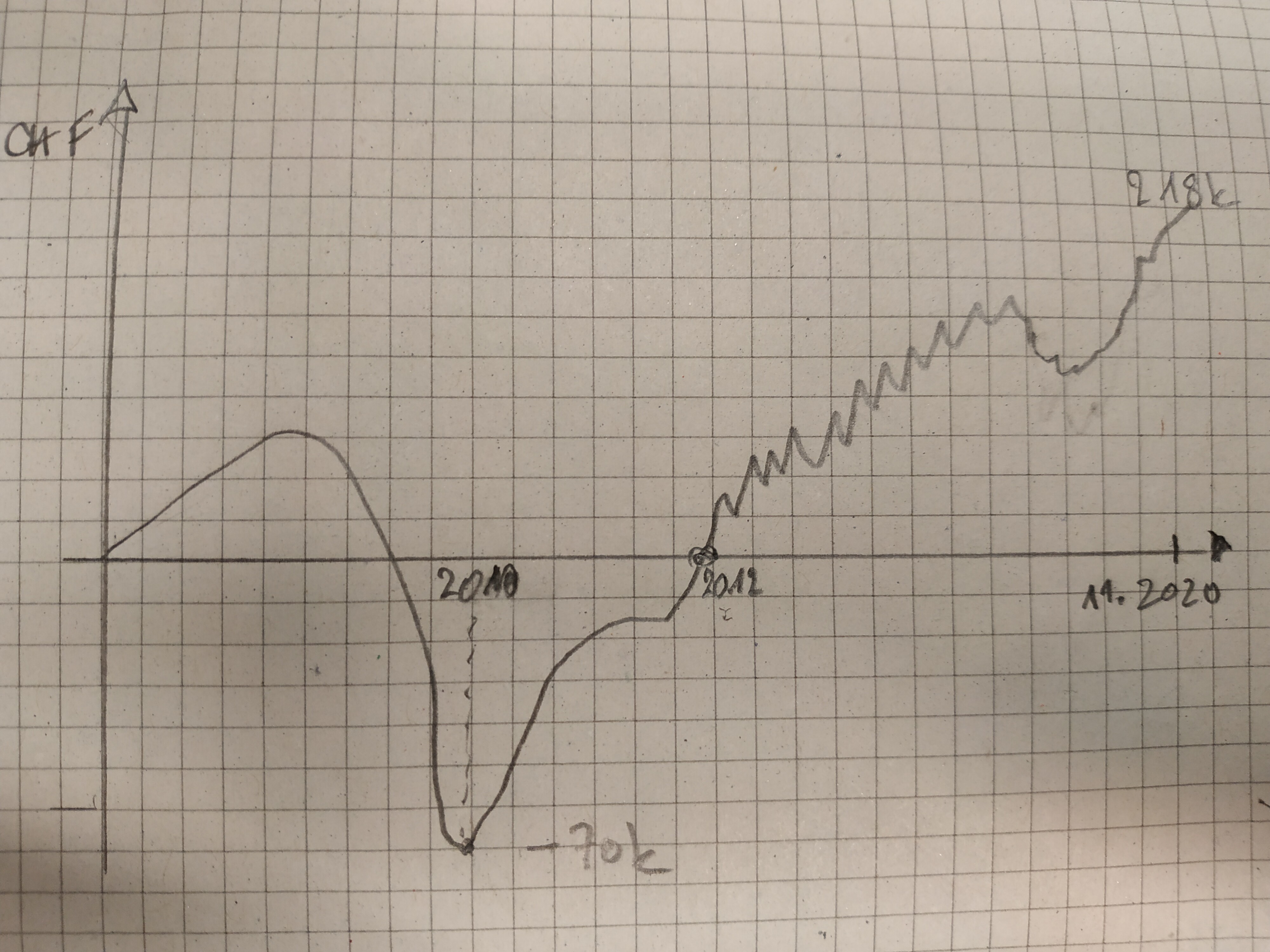

I started tracking it on a monthly basis back in September 2019 when I started investing. 3k cash reserve and most of my bankable assets in VIAC. Now after 14 months I progressed from 31k net worth to 73k. Despite higher expenses than anticipated a year ago (moved out into my own apartment and separated from GF, had to buy a lot of new stuff, did a hair transplant…nothing I planned on). And despite literally the worst market timing in the internet (I mean who invested 50% of his assets up till then on February 20th? Lol). So I’m quite happy with it!

My next goal is to hit 100k net worth. Depending on my bonus next February I’ll probably reach it in autumn 2021.

Current goal is to be at 375K by the end of 2021. We are going to have to pay a ton of fees for the house, so we are not aiming at a huge increase in the next 13 months.

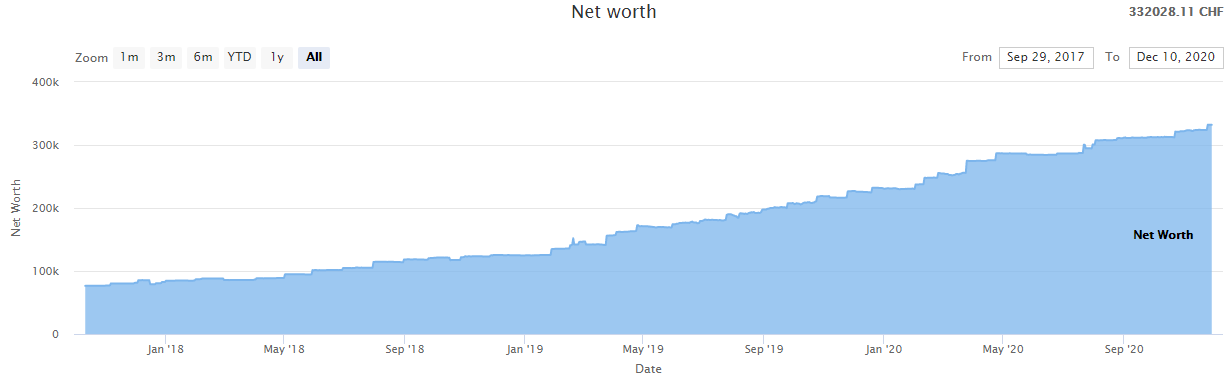

I started tracking systematically - as well as investing “properly” and seriously - only from Dec 2018.

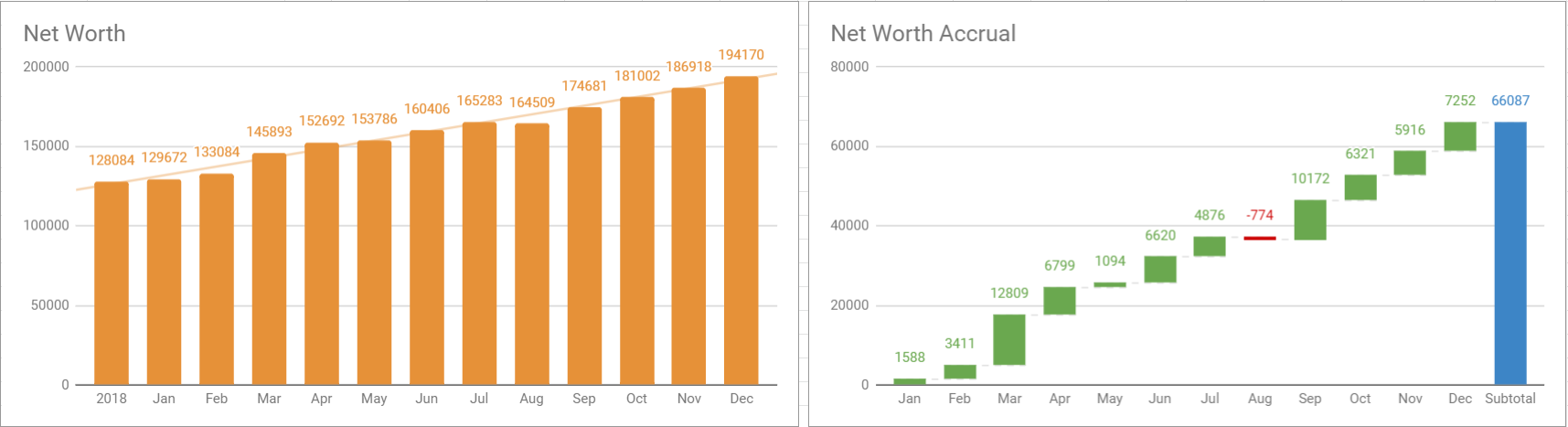

And now I realize I only have the year-by-year view - might create another “overall” sheet.

I am including the 2nd pillar in my calculations, but not the 1st.

2018 (approx.): 103k → 128k

the year I got the car, haven’t yet had any stock investments other than the company ones, crappy UBS Vitainvest 3rd pillar, and some crypto assets that declined from Jan-Dec by 8-fold (!)

2019: 194k

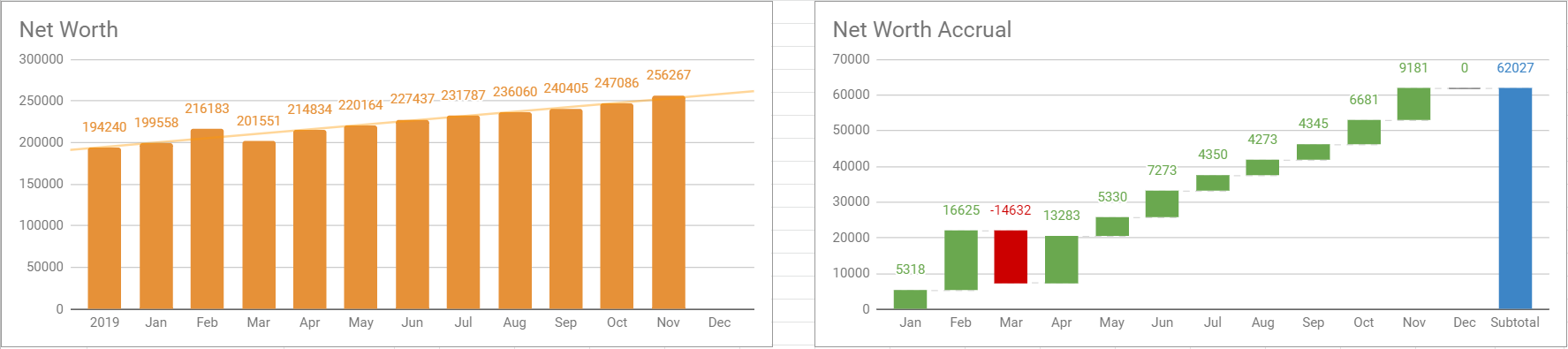

2020: 256k (so far until Nov)

nice to see how the March dip was just a slight slowdown in the grand scheme of things (on the other hand the drop was there in spite of the bonus payout)

Feb was when I got/sold some company shares that got un-vested, hence the spike

in July I bought a (small) motorbike - felt good to see no huge impact

42% net savings rate (i.e. after tax) so far this year

We are buying a house in 2020, so we went hyper conservative and converted everything in cash in late 2019. We did not want to take a chance at losing an opportunity. It turned out well. But it also means that we lost the recovery.

I made a typo - the charts are for 2019 and 2020.

First bar is “end of previous year” value.

In essence, I kind of “lost” 2 months of regular ~5k/month growth rate - which is to me quite amazing to see.

And a lesson in patience and power of staying (mostly) invested.

Good point, and a fair observation to consider!

I will analyze it a bit with that in mind - thanks.

I am in the “frugal/saving” mode since I got my first scholarship in bachelor’s back home (10+ years ago).

I just never tracked it seriously, as back then the stipend was the only “income”.

And first years of proper working I was just doing the saving part, not the investment+analytics part that much (or it was in a different format - via mobile apps etc).

I “standardized” it now in the last 3 years with a couple of sheets.

Must be the early enthusiasm many have when joining a new self-help group.

I do believe the observation might be biased from the frequency and volume of posting of members here. I mean…

Do you believe that having done something successfully over 10+ years makes you (more likely to) frequently post about it on public internet forums?

I don’t. I think it’s quite the contrary, actually. Many people who really do know their stuff and have done something successfully (or professionally) for a long time will only rarely chime in - if they even bother to register in the first place. It’s a thing that can be observed in many internet forums and online communities (though arguably less so on more technically/professionally focused niche forums).

As for me, as someone who’s actually “been on a 10-year savings journey” (but started out on very low income by Swiss standards for the first few years), I’m merely practising my English here.

So I’m very much at the start of my journey. Much like @stojano, I’ve made a few mistakes which led me to where I am, which I like, so nothing to change in hindsight but a good focus on my forward life.

I’m using LibreOffice Calc so, not particularly more sophisticated as far as I’m concerned… ^ ^

I sold it and have an exact figure of how much I made on it in the end after taxes and expenses. That’s what I linearly interpolated for the years of holding.

It has beaten the stock market (counting ROI on own capital of course) but not by a large margin. Cheap living costs and some tax savings is what I got out of it, mainly.

Refund amount that you can get, assuming you’re eligible for it (most third world nationals are) and single male, is:

min(pension part(~80%) of total employee+employer AHV contributions, round(<number of full years of work in CH> / 44 * 2370) * 12 * B20(current age))

Passport (not residency, anything non swiss is fine - you must deregister from Switzerland naturally) at the time of refund request is what counts for eligibility.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.