So here is my first financial net worth post.

Looked it up last weekend and realised that I have over 500k CHF in equities… so I am 25% done on my way to 2 million.

Then there is 100k+ CHF in Pillar 2, and another 70k worth of real estate.

Next update when I cross 1 million in equities likely in 4-5 years.

I’m not sure if there’s enough content for multiple threads. I track my NW monthly but post it here only quarterly (I think I missed my Q2 update though). I don’t mind other people posting more frequently because it can give more context to current events.

First time I post it.

I don’t include 3a (31k) and 2pillar 100k …

It’s not much and this year I have not been able to contribute a lot (only 3a). Burn out and reduced my %.

Fortunately I’ve been lucky with my tradings

Also i’ve started with huge debt

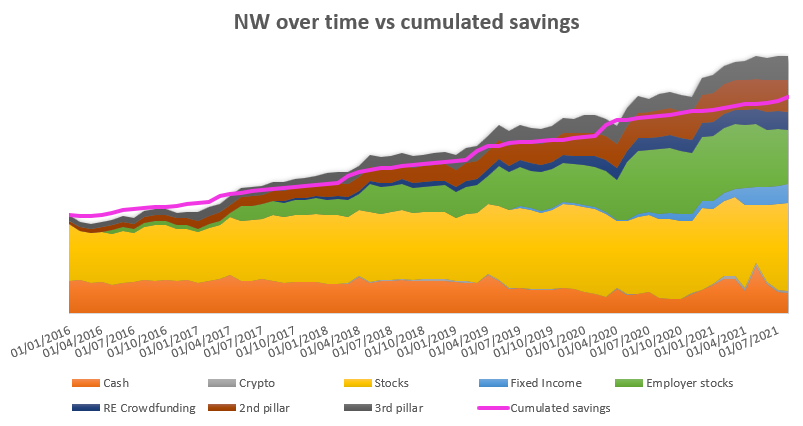

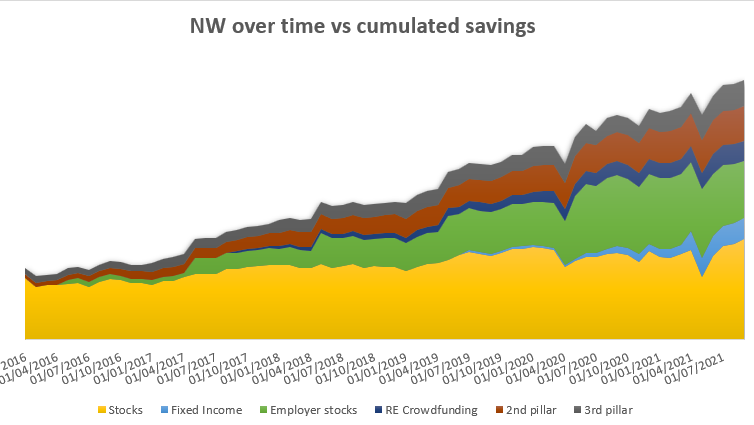

Ok, so here you are all with your fancy charts and insights and I’ve been just a tracking ant. After some scripting, prices retrieval, study of 2nd and 3rd pillar statements and even finding some “forgotten” crypto, I was able to produce this (as well as to semi-automate the data export from GnuCash so that I can keep this updated with the only effort of tracking transactions, not valuations).

I have less detailed information before 2016, so it is what it is. I have therefore equated cumulated savings and NW on Jan 1st 2016.

I have borrowed your idea of plotting the cumulated savings on top on the NW, which leads to the following interesting comments:

I have changed my mind and I now consider 2nd and 3rd pillar as part of my NW. I should maybe apply a discount percentage to account for taxes if withdrawn, but that’s just a quick Excel formula so no pressure.

At the beginning I would have been better off without investing as I was “losing” money.

Despite wasting a lot of money cancelling my 3rd pillar insurance in July 2020, it is hardly noticeable now.

Corona shock brought me down to a situation where if I hadn’t invested a cent since 2016 and invested everything then, I would be richer than today.

My compensation plan was a risky one. I have since changed employers and I’m slowly selling those now vested stocks. The new employer does not offer stock options.

Now that I have accounted for all the cash I have in different accounts, I realized that my equities asset allocation is way lower than I thought.

Income from stocks, fixed income or RE is translated into cash unless re-invested, however that together with valuation differences account for the delta between the saved money and the NW.

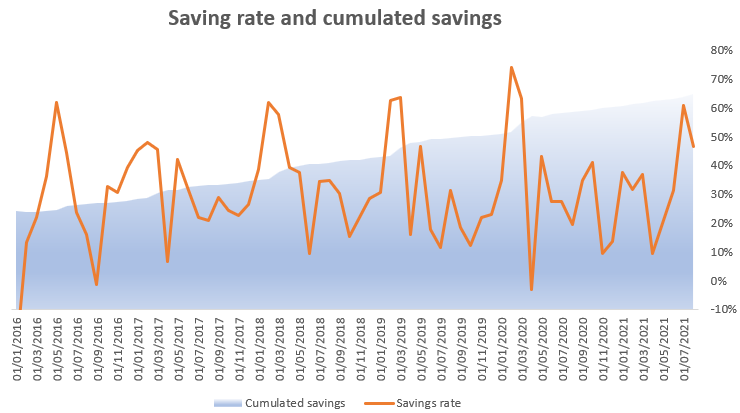

Although this belongs to my personal numbers thread that I will update as usual at the end of the year, my savings rate is really inconsistent:

I wouldn’t put much thoughts on that. 2016 was a bad year, which you couldn’t have known at the time of investing (but only in hindsight) and timing 2019 (which was an awesome year), then the Corona-crash isn’t something us mere mortals are able to do repeatedly. Would you be richer than today if you hadn’t invested at all? And if, through an imaginary thought process, you would have not invested since 2016 and until last year’s crash, what other thought process would have had you change your mind and drop everything in once the crash had occurred?

That’s something I have noticed as well. Mandatory 2nd pillar contributions give a good conservative basis to our allocation, it’s actually hard to be very agressive without a high net worth in Switzerland.

I’m not invested on margin. I bought RE in Bosnia for 16k, build a new gaming PC for 5k and took a 7k loan from my GF as my 10k emergency fund wasn’t enough to cover those “unexpected costs” lol. So my emergency fund is at 0 since 4 months and I’m paying back my GF till end of this year. But don’t worry. I’ll receive a bonus of around 16-24k in February next year. I’ll use it to rebuild my EF of 10k and invest the rest.

Just coming back from Bosnia and enjoying 50.- coffees I still have no clue what 16k would buy you . Did you write about that investment decision in some other thread?

520 m2 and 430 m2 land. One for my future vacation house and probably FIRE headquarter and the other for building something to rent out (it’s a 15min drive to the ski resort where the olympic games were played in 1984). But I will probably not do anything there in the next 10-15 years.

So, soaring until February, got it. xD Glad your relationship with your girlfriend is going well enough for her to lend you 7k to buy a gaming PC (and real estate). Though I guess it’s sort of paying itself off mining crypto.

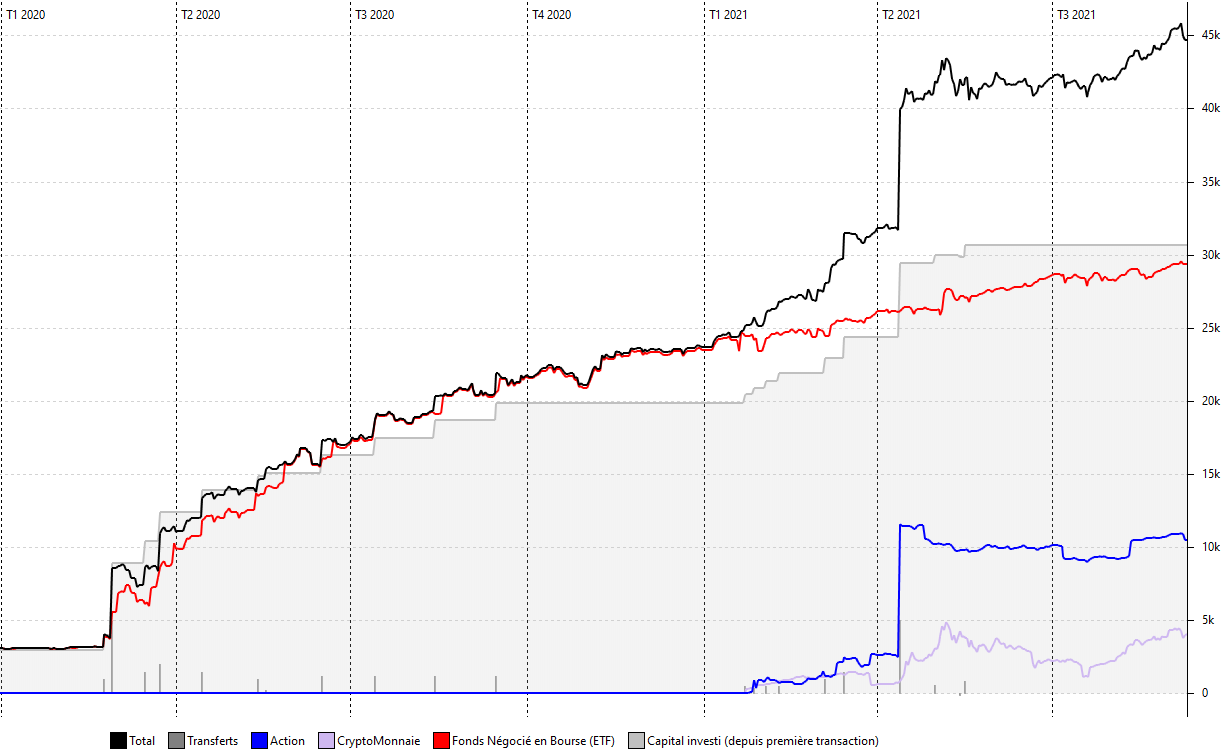

I’ve finally decided to share my (tiny) net worth.

To sum up a bit my situation:

I’m a trainee lawyer (1st of June 2021 to 30th June 2022).

I’m earning 3’500 CHF net per month.

I opened a first 3a account on May 2020 with VIAC (+30%) and a second one in January 2021 (+18%).

I’ve invested with Selma in 2020, and closed it in March 2021.

I had a lot of cash in January 2021.

I opened an IB account in April 2021 and invested 30’000 CHF on VT.

Since then, I’m investing 2’500 CHF each month from my cash cushion and save that I could make despite my unemployment indemnities and internship salary.

I’ve been investing in cryptocurrencies [Bitcoin (CHF 50), Ethereum (CHF 50) and Swissborg Token (CHF 50)] every two weeks with Swissborg since June 2021 (300 CHF per month). I am positive

The collapse in September is just because I have to wait the end of the month to put new data. But indeed, it’s a bit weird (or a prediction, who knows ?).

The area around the olympic villages is quite close to Sarajevo and beautiful. Currently most places are a pain to get to because of bad roads.

But there is quite some tourist potential. I’d guess the investment outcome depends a lot on how the country develops in the next decades.

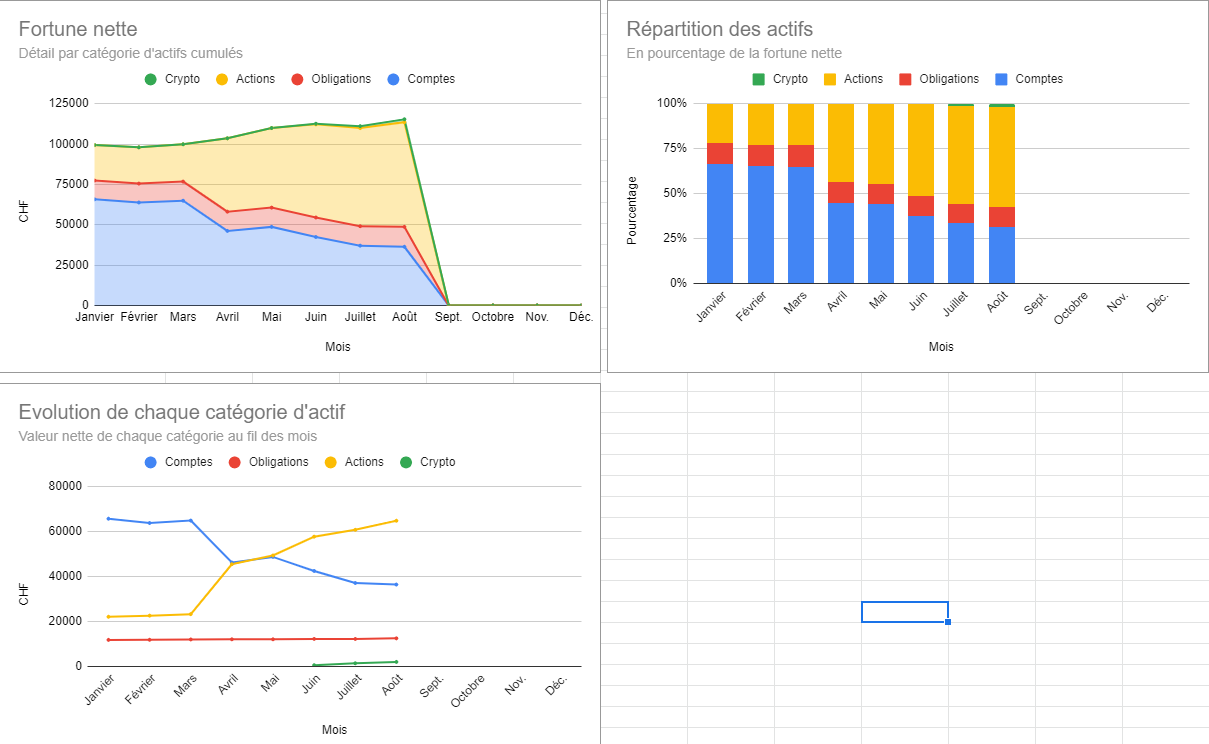

However I agree with you that the performance is not great. You can see I was doing OK before covid. Things are taking off slowly, but I’m far from a Mustachian allocation. Let’s say that I have made the mistake of wanting to be a stock picker and I have left money on the table. I’m transitioning to more and more passive index funds. In fact that is why there is a dent around June 2021: I sold a big sucky position and I bought VT with the proceeds. During that time (a bit over a month) the money was in cash.

Thanks for the insight. Still some allocation optimization to make. I’m (slowly) working in a graph that will let me see the allocation quite clearly. I have still a lot of “a little bit of this, a little bit of that”.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.