Yeah, in hindsight I would have taken a different approach but we have the amortization contractually built into our mortgage - so no way back.

Besides, it gives peace of mind knowing that the house is substantially paid off (already).

Yeah, in hindsight I would have taken a different approach but we have the amortization contractually built into our mortgage - so no way back.

Besides, it gives peace of mind knowing that the house is substantially paid off (already).

We set the mortgage payment such that we pay approximately the market rent. This way, our housing cost is no different whether we are renting or buying, but in practice, our ‘savings’ go up due to equity build-up: due to the very low interest rate (we got 0.75% fixed for 10 years) most of it goes to repayments.

What I mean is that it’s not really an expense, it’s (forced) savings/building equity. (You wouldn’t count adding money to your investment as expense, right?

![]()

Why not a mix of both?

In this type of situation, what I do in my budget (mobile app and banking assistant from my bank) is include my investments as expenses. However, when I do my monthly or annual review and compare my expenses and income, I exclude (filter out) these investment expenses. In itself, it is an expense (my money leaves my bank account and goes elsewhere). But it is money that will be used much later (house, retirement, other things).

This allows me to track my expenses while excluding this type of expense as an “expense” in my monthly/annual balance sheet.

I do the same thing for taxes. I include them as an expense and factor them in when calculating my savings rate. I also exclude them to find out my savings rate without taxes.

Too early for 2025 figures? Books are basically closed ![]()

Some 95k for a family, excluding taxes and amortization (not an expense to me, either).

15% below 2024.

Child care is up and took the prime position, but housing is down a lot due to lower interest. Comparable cost like food, health insurance or transportation are more or less flat.

Ah, yes, got what you mean now. Yeah, it’s a balance sheet transaction but not a P&L one. Still, it places a demand on cashflow:)

Didn’t hit my savings goal of 50k this year due to several new hobbies (motorcycle and NAS at home), but still decent enough.

| Earned gross | CHF 145’470 |

|---|---|

| Earned net | CHF 133’370 |

| Taxes | CHF 23’000 |

| Spent | CHF 67’700 |

| Saved | CHF 42’660 |

Will retry next year ![]()

You can always try to save next year, but you can’t go back and have the experiences this year. My philosophy is to always keep FIRE goals secondary to life goals.

True. Had probably the most amazing summer in the last 15 years. So it was well worth it ![]()

2025:

+1.0M income

-0.2M spend

-0.1M donate

+1.6M NW

Will try to do better in 2026😂

Wow, will take me still a few years to reach that income as it is from stocks only. But then my spending is way lower even I have to support my father and my mother in law.

Donations of 100k? I had to intervene my mother in law to buy a shitty dishwasher for 150 Euros when hers broke down.

Once my wife and I were married she looked puzzled when I asked her about her pension and suggested she ask how much she could pay in to reduce her pension gap. It took much less time to get her to agree ( ![]() ) to me giving her the money to make a very substantial 2nd pillar payment. The tax benefit was substantial (I had ‘peaked’ with my comp/ben while still employed + getting a severance; her comp/ben was a small fraction of mine and still is thanks to FIRE).

) to me giving her the money to make a very substantial 2nd pillar payment. The tax benefit was substantial (I had ‘peaked’ with my comp/ben while still employed + getting a severance; her comp/ben was a small fraction of mine and still is thanks to FIRE).

I told here there’d be a time where I would never be working again and she’d still be working and taking care of more of the bills so we’re all in the boat together now. In fact, I’ve come to realize that her not working would be rather expensive… not only in terms of losing the comp/ben, but also it triggering that both of us would have to pay AHV until retirement (and I believe it would be based on assets… so a rather big hit).

Additional realization this year was that having my 2nd pillar moved to 2 foundations with Finpension (Freizugigkeitskonto) has been a very, very positive step. As it stands now, my 2nd pillar grew close to 10% this year and that’s despite keeping a sizeable portion in cash and bonds as dry powder in case of a market drop. If I can manage 10% on my 2nd pillar for another 10 years than that’ll be a major positive surprise from a retirement perspective. The downside is that it makes me not be so interested anymore in getting a moderately compensated job because I’d lose a big chunk of annual benefit by having to switch my 2nd pillar back into a crappy return pension fund. Still too young to retire, so I’ll have to search a bit for a better way to organize a new job - e.g. not go on payroll but simply invoice my services.

Definitely you are this place’s GOAT.

Very similar story here. I didn’t expect such a post on a mustachian forum but I also have to say: it was amazing and totally worth it, spending more. Spending on what matters. Minimalism and not frugalism. A transition.

I’ve had some hard core saving years and these are over at least for now. Let’s see if it changes again in the future. But I don’t see myself going back to pure frugalism. Minimalism it is for now.

This transition is sponsored by salary increases aka funded life style inflation. My saving rate somehow remained above 50% making my ingrained mustachian calm down.

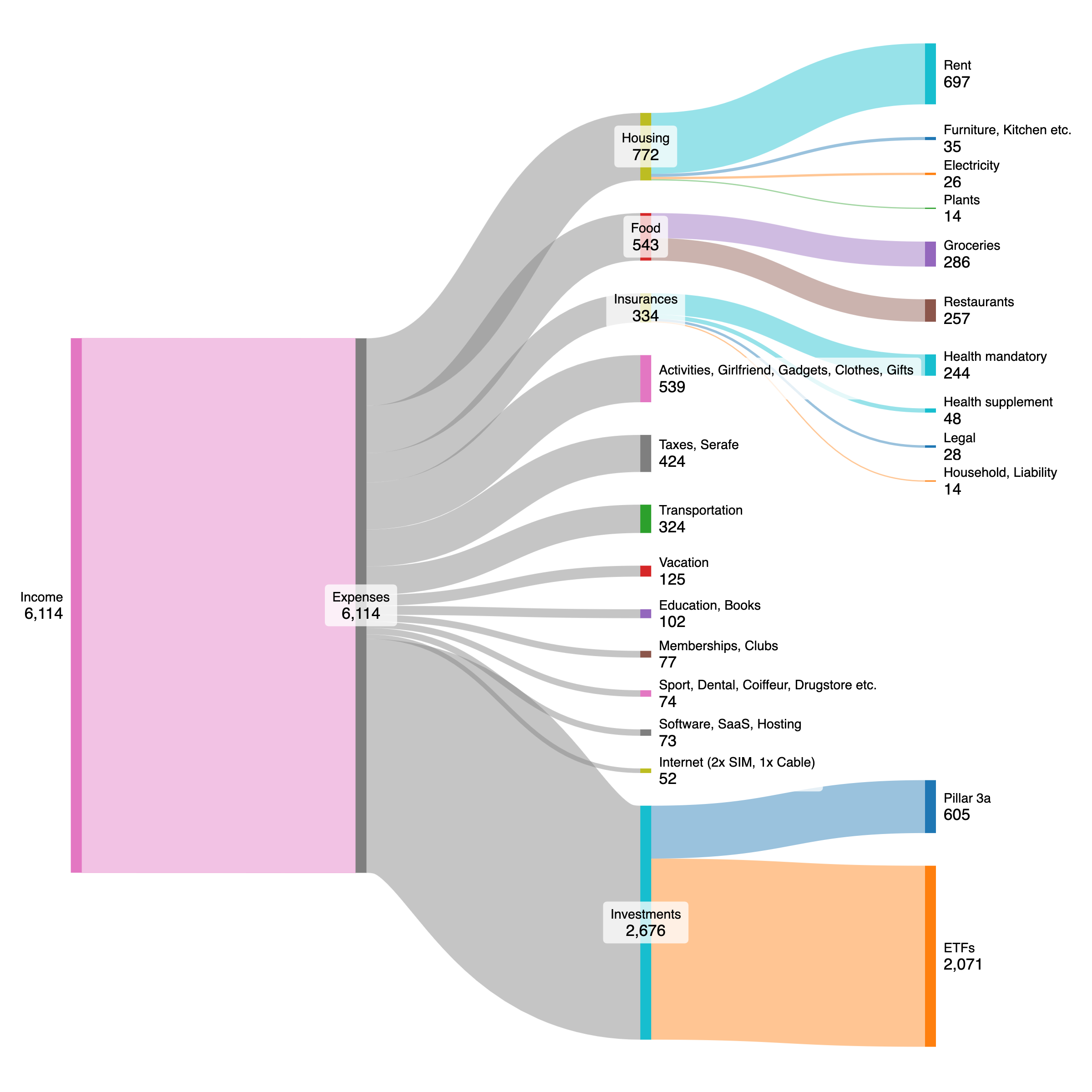

Monthly expenses (Sankeymatic).

Time to look back at the total expenses for 2025:

Family of four in a mid-sized Swiss town, living in a rented apartment.

Total yearly expenses CHF 101K (w/o taxes, my wife spends some of her own salary, which is not tracked).

Saving rate (w/o taxes): 42% (better than last year)

Biggest items:

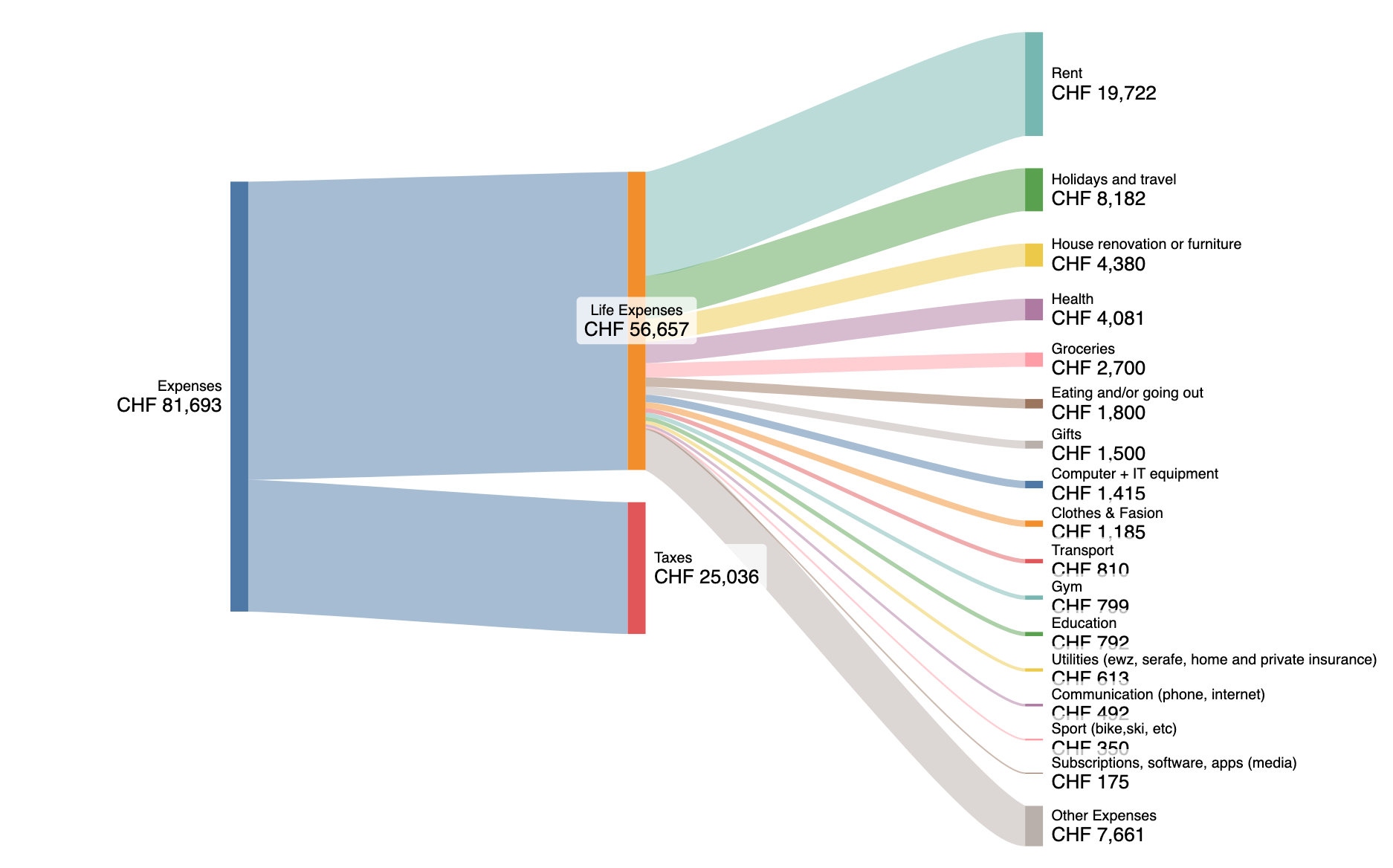

Another year, another balance!

Zurich, 36F, with partner sharing costs, no kids.

The main changes:

What is considered a tax? 25k seems a bit much to be taxes only.

Edit:

My bad, i didn’t see, that it only shows expenses and no income. ![]()

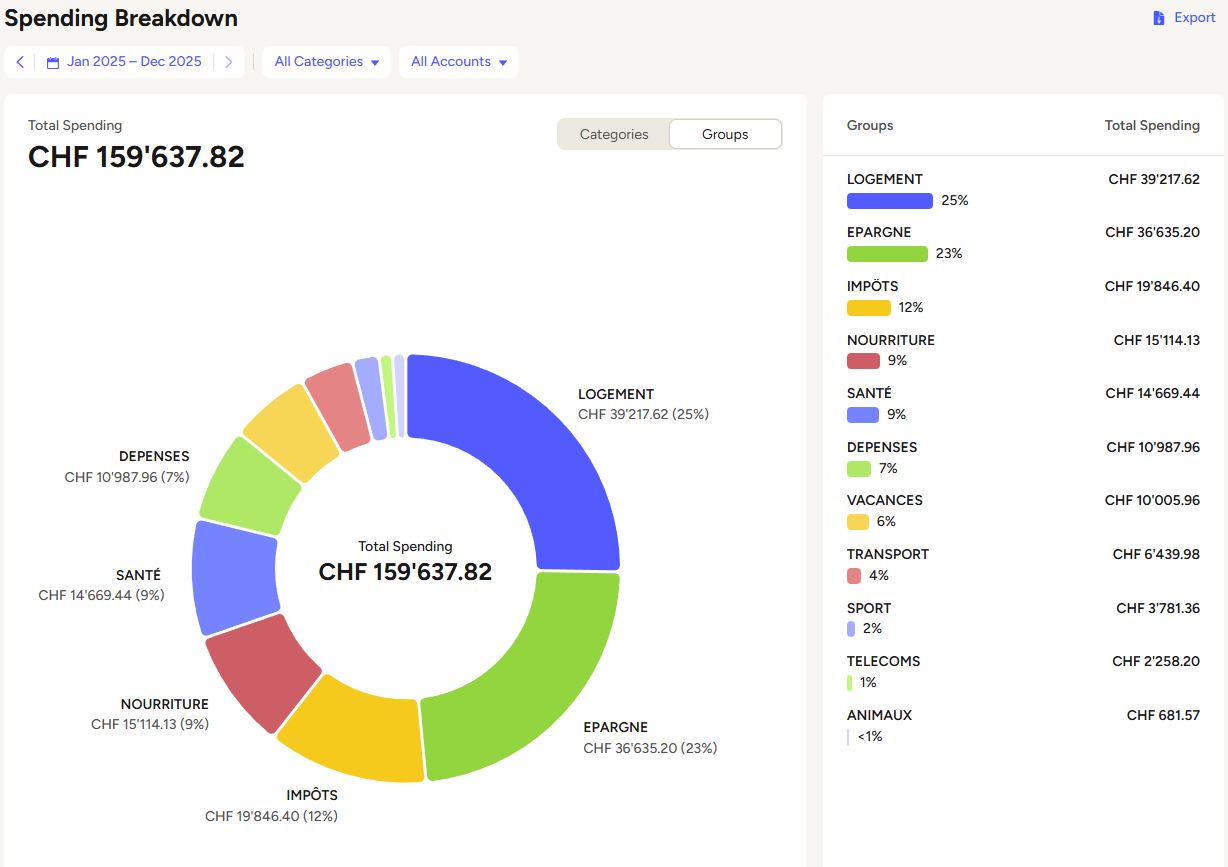

The years go by, but they are not all the same. This year, 2025, has been emotionally difficult from both a personal and professional point of view.

Professional

I changed jobs in March 2025, becoming a Law Clerk (Judicial Assistant; I write decision against the Governement or the lawyer) in a court of law, working at 80%. I live in Fribourg, but I work in St. Gallen, renting a room for my working days (+610 CHF per month). My salary has decreased because I am working at 80%. The promise of quickly increasing to 100% and getting two days of homeoffice has not been kept. I know that working 80% is a dream for some, but for me it’s hell. I’ve noticed that the less I do, the lazier I become. This isn’t right, it’s not me. For the year 2026, I plan to train in areas that interest me and look for a new job. Perhaps as a lawyer in Geneva, Lausanne or Fribourg.

Personal

I’ve become lazier. I have a slower pace, I take my time and I notice that it doesn’t suit me. On the positive side, my girlfriend and I communicate more, and on the days when I’m in Fribourg, we spend more time together and have a better relationship. We had a wonderful trip to South Korea, a beautiful country that I highly recommend. Next year, we’ll probably go to Japan.

Finance

YoY: 18.74%

My girlfriend and I have seen our incomes decrease. My girlfriend has a new employment contract with more social benefits and no fixed term. For the first two years, she had a fixed-term contract, no social benefits and a salary that depended on her monthly hours. She was earning 100k a year, but now she’s down to 80k. I went from a hypothetical 107k to £100k this year. So, less money to save, but more to spend, particularly on my room in St. Gallen and a few nasty surprises. It’s a year to forget quickly, but that’s life.

Savings rate with tax: 23% (CHF 36,635 in savings)

Here are the details:

We are two mid-30 ![]()

PS: 400th posts ![]()