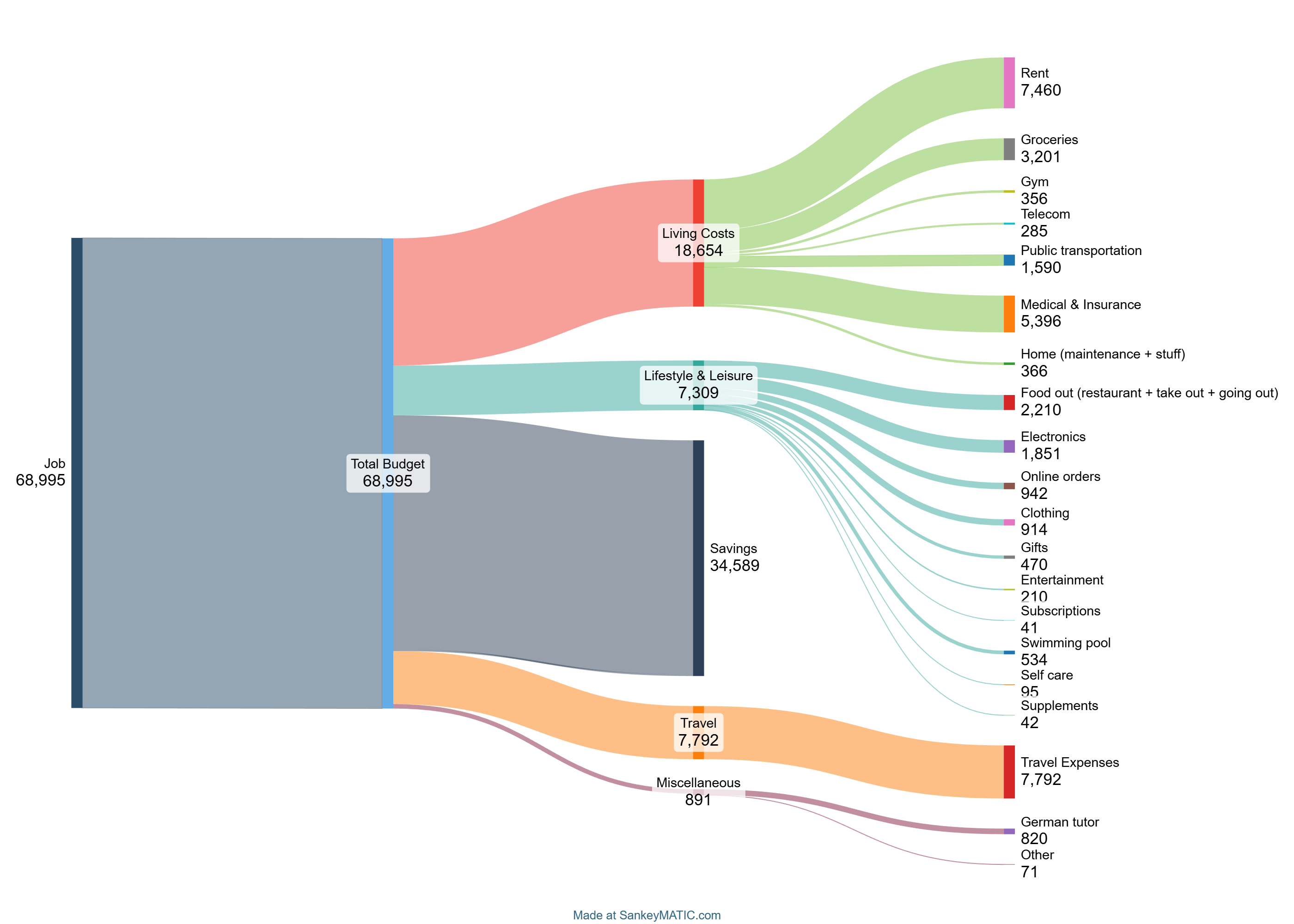

So I think this my first time posting it here, single early-30s household in region Zurich.

Required expenses: 38k

Rent: 24k

Health Insurance: 7k, got the private thing + free choice …

power: 1.2k

internet+phone: 0.5k

groceries: 5k (not fully fixed but I can’t really go without any)

serafe: 0.3k

Wants: 33k

travel: 15k (14 trips, most weekends, but 3 half-weeks and 1 1.5 week vacation)

Electronics: 8k (let myself go a bit this year )

Language lessons: 3k (hobby, not german)

Other paid activities: 1k

train: 1k (optional because my commute is by bike, probably includes some travel by train)

gym: 1k

medical: 4k (finally got my eyes lasered)

Didn’t bother categorizing: 5k (mostly odd restaurants, music tickets, clothing etc. I couldn’t bother to categorize)

total spending: 76k

Given that 2 years ago (didn’t do the exercise last year) I was around 58k, I clearly started spending more, but outside of health insurance my needs didn’t increase significantly, and my phone/internet/power bill are actually down a bit due to me optimizing.

Currently at ~270k/year post-tax income, and near FI in NW (depending on exact withdrawal rates and tax, as well as my doubts in my ability to get another apartment to rent without income in this market), so figured I’d try spending a bit more to try to be more active & social. Looks like things are going in the planned direction without irreversibly increasing needs, so the direction seems reasonable to me. However I’m a bit surprised at the yearly total for electronics, so I might try to be a bit more conservative there.

your expenses while working can be:

.

1a) more than what you’d probably spend when FIREd (commute and transportation costs, work clothing, stress related expenses,…).

.

1b) less than what you may spend when FIREd (less time for leisures and hobbies).

.

I would try to assess whether the target of 70k expenses while working is bound to translate into 70k expense when FIREd. If some expenses are bound to disappear, I would list them and give me some leeway in 2026, starting to really work on them only once FIREd or in the last months before it.

I’m sure you have done it and the reminder posted here is enough for you but if the goal is truly to reduce the “everything else” expenses by 10k, I would list which specific expenses are my target in order to help me focus on it and straighten my mind when I think about doing more of the things that pump them or cancel the related subscriptions/activities if that’s what’s applicable.

Exactly. It’s less about savings rate (another 50k more or less year won’t matter too much) and more about knowing I can fit into a FIRE budget at reasonable SWR. I see lifestyle inflation as dangerous, at least until I get a few years of FIRE of some sorts behind me, maybe until after a first market crash and re-assess what my spending can be.

Thank you for the advice and the kind words! Luckily I think I know pretty well what expenses I can “avoid” and have it fully in my control. I just need to be mindful.

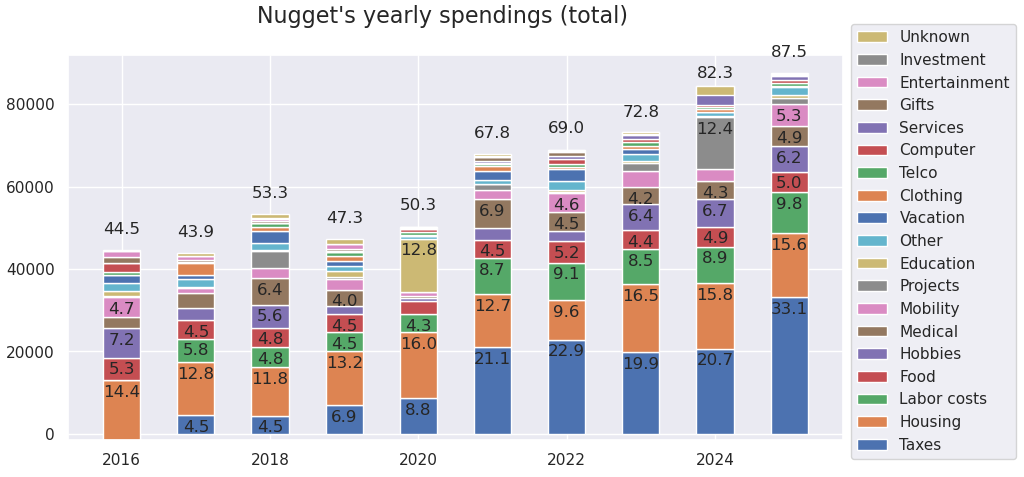

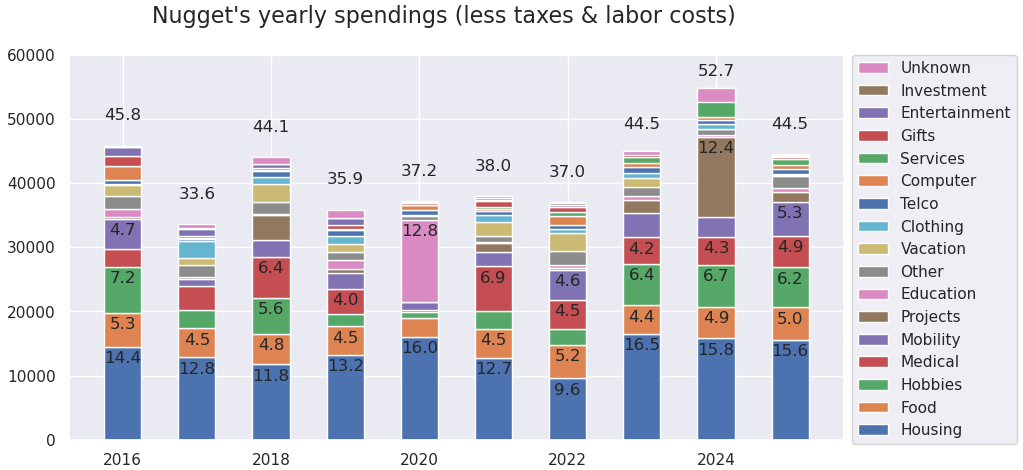

male, late 30s, no kids, city of zurich. since 2.5 years in a shared household with my partner (instead of a WG). The numbers below are my personal expenses plus half of our shared household expenses

overall a steady increase in expenses. maybe some lifestyle inflation

There are lots of inconsistencies within these charts, for example transition from source tax to standard taxation, household changes, job changes, pandemic, weird bookkeeping practices & tricks, etc… but overall they are pretty accurate

I wonder where i got that number from, 8 years ago

Yeah nah… I’ll stop making predictions now.

But 2025 covers pretty much all expenses for 2 people.

(incl. German lessons, some business stuff of my wife)

Total: 90k

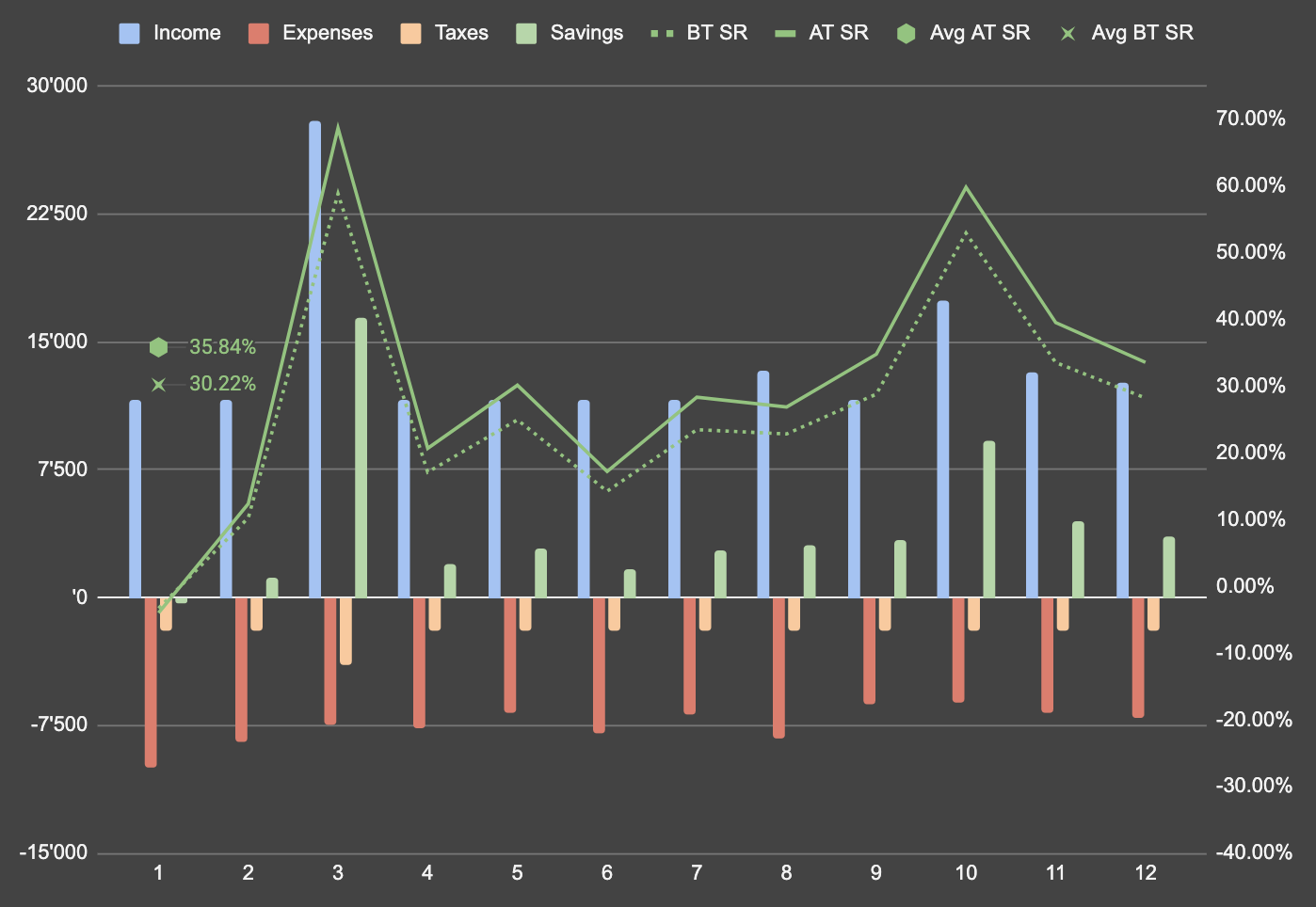

Savings rate:

Pre-tax: 30%

Post-tax: 36%

Post-tax incl. P2 employer contributions: 40%

Historic summary

Year

Expenses

SR (BT)

SR (AT)

SR (wP2)

2021

62k

N/A

34%

N/A

2022

63k

37%

45%

N/A

2023

62k

38%

47%

51%

2024

80k

32%

38%

43%

2025

90k

30%

36%

40%

Monthly breakdown of top 90% expenses (excl. taxes):

I do track the two (or even 3) savings rates - before and after taxes - using “tentative” amounts as best estimates.

Just not showing them in the expense categories above,

since they are probably least interesting to discuss,

and not really something too much in my control to adjust for.

(Tax optimizations being separate topics)

What would be the reasoning for including it (at least the income tax)? It’s cost of income acquisition not actual money you spend.

Esp. for people with high income it’s not very useful for FI planning, if you were to stop working it would dramatically go down (my taxes are much higher than my living expenses).

Shares of @dbu & Sons fell sharply in after hours trading today after the company reported a lower-than-expected saving rate for 2025 and downgraded its growth outlook for 2026.

Analysts commented that without major changes in leadership, the stock is now a strong sell.

It could but it’s usually a much smaller cost (and most people would still eat even if they stop working, and with subsidized lunch it might even be more expensive )

For me the biggest argument to not count income tax is that it increases whenever you earn more, which makes it sound like lifestyle inflation when you look at graphs. (And it’s the expense that’s the easiest to fix, just earn less )

I think it could make sense to include wealth tax but I am neither interested in the income tax.

I want to estimate my monthly or annual budget , I will need to support after FIRE. Your income tax will certainly drop significantly but not the rest except if you decide to relocate to a cheaper city/country.

This annual budget could help you define a FI number based on a Safe Withdraw Rate.

I consider wealth and dividend income taxes (and fees and inflation) by defining an expected net return that is lower than the expected gross return. While that’s not completely accurate (e.g. due to tax progression), it is simple and should still be more realistic than estimating taxes as a fixed amount as part of expenses.

It may be different for countries with capital gains taxes where the taxes paid each year might correlate more with your expenses, but in Switzerland taxes are (mostly) independent of other expenses as realizing gains doesn’t affect the tax amount.

I am doing a follow up to my last year’s breakdown. Honestly, I cannot say enough how happy i am that i started tracking my expenses, and i have almost 100% understanding of where i spend money, it makes so easy to do some simulations or backtesting(what would it be if I moved into my own appartment, how much hit to my savings etc)

About me:

Early twenties

Live in a WG

Biggest changes this year:

Income didn’t change that much(higher base, but lower bonus this year, so accounting for inflation i am paid lower)

Consistent with my german tutor(99 lessons this year!), slowly getting to B2 level

Not so much nasty surprise expenses, but i was battling a health issue through the whole year, so that increased a lot. Thankfully it’s getting better and i hope in a few months would be completely over.

In 2025 i spent more for travel than rent, lifestyle inflation yay A lot of travel and small trips which added up

This year i really want to move to my own apartment and i am horrified by the prices

Salary is already Netto without income tax and social contributions

Note to fellow forum members: by excluding income tax, we are treating it as a non-discretionary item. Yet, there are a few ways to actively manage it down. Also the net salary is influenced by the choice of pension fund contribution which can be considered a part of savings. Even the employer pension contribution is a kind of saving. (Yes, yes, this is a rather academic view)

Side note: why put gym and swimming pool in different categories?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.