If you add unrealized gains (and losses) from the stock market to your income, you might also want to consider adding gains (and losses) from the value of your apartments to income. But I think these should be in a different category named “wealth”.

So you spent all money you made in 2024 and did not put any money for yourself and wife into 3rd pillar? Did you set aside some money for larger renovations in your 2 apartments? Do you have an emergency fund with cash at hand or do you have to sell some stocks in an emergency?

I think I am being insensitive but it feels like your wife is not pulling her financial weight in this relationship.

Hi, I think I was a bit too vague with just saying “education”. To clarify this is after my masters degree. I part-timed in a relevant field during the masters and already had some internships/work experience before that. From the point where I finished my bachelors if you adjusted my salary to 100% you would probably just see a gradual increase across several years.

Going straight to 7-8k netto would definitely be a bit steep unless you are in some really high-earning career paths (which I am not).

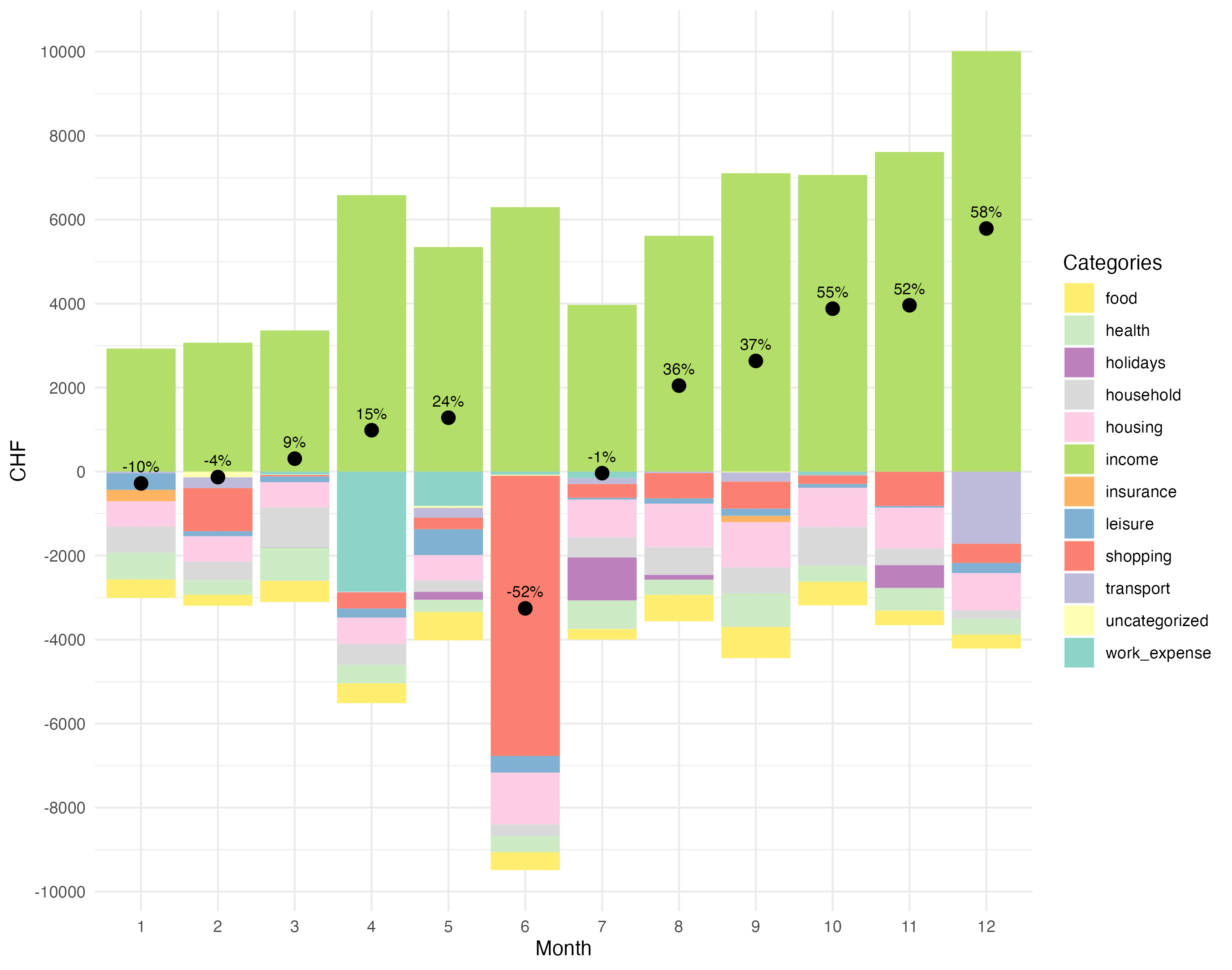

As we leave 2024 behind, I thought it would be interesting to share our balances and reflect on our financial progress over the last year.

It can be insightful to see how others have grown their savings, investments, and overall net worth, and I wanted to see a baseline of what is common for us Mustachians.

To start, here’s a quick summary of my 2024 financial situation:

Net Salary 2024: CHF 63’200

Starting Balance (01.01.2024): CHF13’280

Ending Balance (31.12.2024): CHF66’450

Total Savings: CHF 47’370 VT ETF Growth: CHF 5’800

I was quite surpised to see how much I was able to save, even with my very low fixed costs.

My savings rate is 75% not including fixed costs.

Without the fix costs of CHF 12’000 (Tax, Healthcare, SBB, Phone), I technically have a savings rate of 92% which is kind of insane but something which makes me very happy. I am very grateful to have this situation currently and know that in the future it will be much less.

I look forward to seeing others share their final verdicts for last year, looking at just VT itself, it was a good year for us.

If I remember correctly, you are not living by yourself yet. Right?

So I think rather than looking into savings rate, you should only look at expenses which are typically called „wants“ because most likely the majority of „needs“ are covered by parents

Typically people have three segments

needs (rent, food, health insurance,other important things)

I would actually suggest to think about it the other way. You have 63k Net salary (after tax I guess?), but in reality it is more like 63k + costs covered by parents (rent, food, …). Assumed that this fraction is 1000.-/month you would have a net salary of 75k-80k with savings of 50k. Still super high (~66%), but if you move out, that’s the value I would rather try to keep, since the 75% will be crazy hard then.

However in the end it’s all just mental gymnastics anyway.

For probably the first time in my life, I am looking forward to the end of the year. Because this year is the first year that I have tracked my expenses completely!

I had tried to do this before, but always gave up after about two months.

I do not track my expenses. Anyhow, I don’t pay rent and drive a 22 years old car and I never pay for holidays as I have a beautiful holiday home.

I can deduce my spending from my take-outs of the stock broker account plus my AHV pension. For 2025 (until now) it is CHF 27630 taken out and CHF 5355 AHV pension. Wife made 27k, so total is around 60k CHF. I did spend most of it in Euros this year anyhow…

Kind of low, the tax lady will again ask why my estate did grow that much. I seriously must start to spend more. I already fly business or if available first and did eat only in Restaurants for about 6 months (but that is dirt cheap in Spain). Was about to buy a new car this year, but then I prefer to spend it on my neighbour who is out of job and drives me around for some little money. Never have parking problems and can drink wine whenever I want…

Just to be clear: everybody who works or has ever worked for me in my company or privately makes or made more money than he could make anywhere else, that is how my company did work and how I tick. For me it is little money, but for my neighbour it is not.

I think it was one of the Albrecht Brothers (founder of Aldi) who said: “I pay 50% more for double the work!”. I don’t need double work, but I like it when the work is done all right and when people like to work for me.

Spain is fucked, my driver sometimes works night shifts, 10-12 hours, black, for 50 Euros.

Everybody says I’m crazy to pay that much, because that is more or less what a taxi would cost me. But then I have a lot of reserve drivers, everybody wants to drive me. In Spain taxis are very unreliable and there are no Uber where I live. Anyhow, Spain is the only country in the world (I think) where Uber is more expensive than taxis. This is because of corruption and a monopoly situation.

I’ve never tracked my expenses. During 2025 I have been very disciplined at tracking dividends received plus additional income from writing options. Just to get a sense of the kind of income I could expect to generate from investments.

Having read this thread, and realized how modest from an expense perspective so many live, I am going to consider whether expenses are something I want to put effort in tracking during 2026 - i imagine it’d be helpful to identify some things I could/should cut (substriptions, etc.). The flipside is that the majority of expenses are ‘fixed’ - i.e. roughly 130k CHF / year in mortgage expenses. The interest is the smallest part of that, the majority is amortization as my wife and I had committed to paying down a substantial part of the mortgage during the first 5 years (on top of the 30% downpayment we had made from our funds, and the 10% we paid down from an unexpected cash inflow). We’re on the conservative side here and would like to get to 65% of the house paid down fairly quickly. The amortization is paying down the relatively high fixed interest part of our mortgage (rest in ultra low SARON + very low 7 year fixed) so there’s an easy return on those payments.

That’s superb. Not having expenses rise along (or exceed it!) with the growth in comp/ben is so important. Plus, by not getting used to living excessively, you’ll also be better able to live reasonably post-FIRE.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.