Dear all,

in the beginning of this year I implemented my stock-only asset allocation (see here) and I am quit happy with it.

Now following recent discussions about Brokers and dividend handling on the forum, I consider relocating everything except the SPI Mid fund to some US-listed Vanguard ETF in combination to switching to Interactiv e Broker.

Here I would like to discuss and find out what difference this will make in terms of expenses/ dividends/ taxes/ fees.

My considerations:

Vanguard-US usually offers the lowest TERs for any asset class ETF. For example my Vanguard FTSE all world vs. VT (Total World): 0.25% <-> 0.11 % (although slightly different components), or Vanguard FTSE Emerging Markets 0.14% vs. Ishares Emerging Markets IMI 0.25%

dividend taxation, as far as I summarized from other posts in his forum, are optimized when holding US-domiciled funds and declaring/reclaiming taxes with these two forms.

with IB transaction fees are lower, and virtually no minimum amount apply. Considering that with CT i do minimum transactions of CHF 5’000, this will be an advantage to have my funds distributed closer to my asset allocation.

currency conversion is much cheaper, and dividends are paid out in original currency without conversion

the two cons i can spot are a) with IB i leave swis juristiction and b) i have no experience declaring foreign property & dividends to taxes

What would be your ideas/ comments/ additional points/ rationales on this?

thanks for you comment!

You are leaving Swiss jurisdiction, but you are not entering US jurisdiction. At least they made an UK version of IB for European investors, and theoretically this should not be reachable by the IRS. As I am working in the financial industry, I witness how the IRS is every time trying to tax a more domains of US related assets (and the definition of “US related” is each time broader). The UK tax service is not so diligent so this is at least a relief for me.

5)b) should not really be an issue if this is just a form to fill. It will obviously take some time the first time, but I don’t think you should put into the balance to counterweight the financial benefits.

Yes, they’re even lower. I bought $100k worth of US funds paying less than 3 bucks in trading fees in total. And a couple more bucks to convert currency. It’s insane

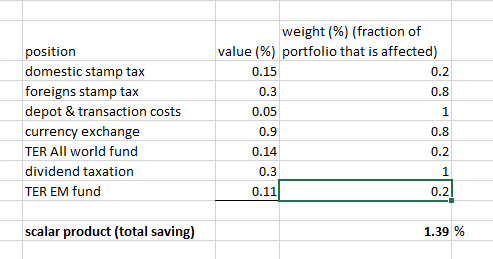

so, if i condense and quantify moving to IB and to US-based funds (for those parts of my portfolio that actually have US based underlyings or are only available in US) I see

0.15-0.3 % advantage on swiss stap tax (purchase & sale with 0.075% or 0.15% each)

a small absolute difference in transaction and depot costs: currently (<100kCHF) in favor of CT, later (>100k) for IB. Order of magnitude CHF 50 ~=0.05%, according to MP’s broker showdown

close to 1% saving in currency exchange, e.g. 0.5% buy and sale. applies to 80% of my Portfolio

0.14% TER savings for swiching from VWRD to VT

0.11% savings on TER for swiching from Ishares EM IMI to some Vanguard FTSE EM,

dividend optimisation: no Idea how to quanitfy. assumption: 15% tax reduction => ~0.3% overall saving

putting this together [fiddling with excel]

holy, this is a cost decrease of astonishing 1.39% !! and it is clearly dominated by the high cost of currency exchange. at this point it is even conservative since USD-dividends will be converted to CHF and back to USD before being reinvested.

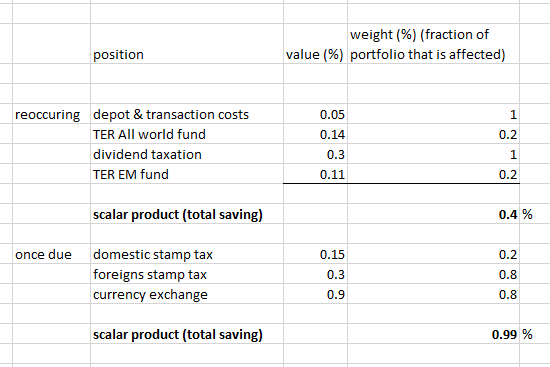

You’re mixing non-recurring transaction costs: trading fees, stamp duty, currency conversion, with recurring holding costs: TER, dividend taxes, reinvesting, account fees. It’s not exactly a fair comparison to just sum up both parts

It’s not charged on ETFs, so probably irrelevant until you start buying individual companies. And then for many blue chips you often have a choice to buy an american ADR to save on stamp duty and trading costs.

In fact you don’t have a choice

European investors are registered automatically in the UK branch. When you create your account at IB and you read the contract, you’ll realize that you are dealing with the UK entity.

That’s why I’m planning - once I’ll reach FI - to move some of my investments into Europe-based ETFs and move that stuff from IB to CT. It somewhat feels safer in CH (or even better I’ll move that investments to Liechtenstein).

Are you considering tracking error, like which index has a better history of tracking error? Is not something you can control, but is worth a thought.

And world ETF in US may not have tax treaties with some countries so you can’t presume you are getting all the dividends. You can only do that with 100% us equities ETF.

You should research with which countries IE has tax treaties, and the same for US.

US will still be ahead since are 55% of world indexes, but you can’t generalise it if you want to be rigorous

I don’t really think IE is better than US with respect to tax treaties, but I haven’t seen this summarized anywhere so far, and it’s somewhat hard to find hard data on this without having to dig through a ton of fund reports

One interesting advantage of ex-US IE funds for taxed-at-source-only swiss investors could be the lack of withholding taxes on distributions from IE. Assuming 10% fund-level withholding taxes for ex-US, that’d be all a taxed-at-source-only investor would pay (through the fund). Whereas for the same stocks in a US ETF, you’ll pay 15% extra of US withholding taxes on receiving a payout from the fund, making it 25% in total. But if you go through ordinary swiss taxation or otherwise have to pay tax on your dividends in Switzerland, it doesn’t make a difference as swiss marginal income tax rates are higher than 15% for most folks and so 15% of US taxes will be just absorbed by your swiss taxes.

for buying US-domiciled vanguard ETFs (such as VT, VTXUS, VTI,…) i’d pay

0.0035$ per share, min 0.35$ comission plus some minor (like tenfold smaller) other charges?

applying this for purchasing $1000 worth of VT @ 68$/share (ignoring currency exchange), this is 15 shares, resulting in 15*0.0035<0.35, so I’d pay 0.35$ for this purchase? seriously?^^ what am I missing?^^

this aims at finding the minimum fee% i have for not so big transactions: with CT, it is ~CHF 20, that is 0.4% for a CHF 5000 purchase. if this is significantly lower with IB, I’d be free to add funds more regulary in smaller chunks, and hence distribute them more evenly over my asset allocation.

With currency exchange (mid-spot+0.5%) the difference is even bigger - actually much bigger (e.g. for exchanging your 5000, they will take CHF25).

Since IB charges you $10-commisions monthly if you don’t have 100k invested, I also switched from quarterly to monthly investments. It’s a bit pain in the butt beacuse it takes time. On the other hand, as you mentioned, I get better distribution over time.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.