I can see merit in a smaller allocation though in general. If we hit a big drawdown for example in the next couple years, MF would potentially shine here.

I would also say if you add like 10% MF, your returns over the long run won’t differ that much from your current allocation and you have some insurance.

Depending on your risk tolerance essentially.

If you are numb to drawdowns and don‘t care, probably not a big benefit here. People do however overestimate their tolerance for risk, especially since the GFC, there were no real heavy drawdowns anymore (ignoring the quick Covid stuff).

I personally think many people that want to be 100% equities may fare better with something like 90% equities 10% managed futures.

I’m not convinced yet and would like some official confirmation of anything that defines short-term capital gains as legally taxable.

E: From the refrenced Kreisschreiben No 15 I can only find this Passage:

Kapitalgewinne aus Termingeschäften (Futures und Optionen) sind im Privatvermögen steuerfrei (Art. 16 Abs. 3 DBG), sofern sie nicht durch das Gesetz ausdrücklich erfasst werden.

Another thing about taxes, specifically withholding taxes:

As we know US treasury interests are withholding tax free, but IB withholds 15% first on any income distribution. How is this handled for managed futures funds?

Will you also get a refund later when the percentage of treasury interest is determined, like when you hold a fund such as BND etc.? Does the fund specifically need to apply/provide documents for that? Do all funds do this?

Maybe @nabalzbhf you know something about how this is handled for other funds that are not pure bond/bill funds?

I would assume in US, each fund classifies their income into interest income & dividend income. If managed future hold pure bonds and not just futures of bonds, then most likely the interest would not be withheld.

They always have at least a modest amount of interest distributions from the t-bill collateral they hold for the futures.

Most funds are essentially 100% cash/t-bills as their total NAV, and the futures themeselves have no real inherent value, just the price movements of those will add/substract from the cash nav.

I would guess it‘s correctly classified, I was mainly concerned if that classification reaches IB and they make the proper refund.

Because as it is now, due to my high margin, I will probably only get nack like 30% of my withheld dividends with DA-1. And therefore any withholding tax I can get back otherwise has a 70% advantage

I was looking again at diversifiers and wondered whether anyone uses trend following and in particular, are any of you invested with DUNN Capital (which is the one I’m looking at because of their longevity).

And I’m thinking of trend-following as opposed to managed futures.

Dunn Capital does managed futures trend following as well for example.

Managed futures is a broad term and can mean a lot.

There is lots of pure trend following managed futures funds for example.

Alpha Simplex managed futures ucits fund could be interesting.

The company has a long track record and manages one of the biggest funds in the US.

Part of SG trend and CTA index. Founded by Andrew Lo

For Dunn, I just don‘t know of a way to invest with them in a cost effective manner from our position.

For reference, these are the current trend index constituents.

We can invest in ucits version of some of them like bluetrend (has a performance fee though) and Alphasimplex

I looked into it, find it very interesting as an non-collerated assets to the standard ETFs, but with a similar return over a whole cycle (+/- 5%)

Found it way to complicated and especially time consuming to find a fund which I completely understand and where I can also invest as a private person. Basically I accept the higher volatility of my overall portfolio (and maybe a slightly lower overall return through the rebalancing opportunity).

Once in FIRE and with more time to look into it, I will certainly have another look, since volatility will affect me much more (and it may have become easier to find the right investment vehicle).

I came to know about it through the “Finanzwesir”.

Well I mostly admired him for his transparency and openly explaining his change of mind. He also always communicated that reducing volatility through Bonds bothered him for a long time since it became more correlated and just reduced the potential income (kind of adding a drag).

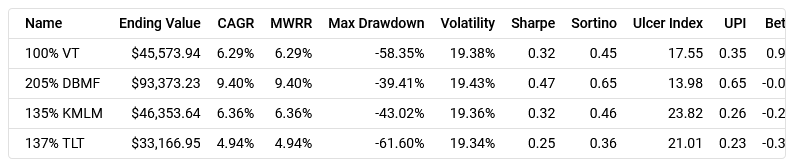

Or if you are open to leverage. Available cheap products (e.g., DBMF) don’t quite have enough volatility to keep up with stocks.

They start to shine when you compare apples to apples and lever them up to similar volatility. Here (testfolio link) a comparison including KMLM (simple & cheap managed futures) and TLT (long term treasuries) starting on 2000-01-03:

All funds were simulated. The weakest is probably DBMF that just gets the index they want to replicate backfilled (with some constant adjustment for fees). But real fund performance over the last 5 years even slightly exceeds those assumptions.

2000-01-03 is really unfavorable towards stocks. But 2003-01-01 is very favorable for stocks, and DBMF can keep up.

I charged some additional 0.5% margin markup on top of USD interest.

It gets even better if you start mixing them (testfolio link). Start date is 2003-01-01.

Now, one doesn’t have to be levered above 2x, but adding some managed futures seems to make sense (more return for less volatility and drawdown). There are the RSST and RSBT ETFs for convenient access to leverage. Alternatively something like UPRO can make some space for stuff.

One can also play around mixing in the seemingly bad KMLM, and find that this is its real strength (testfolio link). Start date is also 2003-01-01.

You go above 100% and use borrowed money, i.e. with margin.

For example you want 80% equities and then add on managed futures with similar expected return/vol., you‘d need to add like 30% DBMF and therefore would need to borrow 10% to get enough DBMF.

Then your portfolio would look like this:

80% VT

30% DBMF

-10% cash

KMLM has more more vol. and you‘d need less of it.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.