Or as @Tony1337 said, you can do it yourself with a margin loan.

Costs are not the be-all-end-all if additional returns exceed them. A good part goes to trading expenses, but the TER for products in this area might still come down further with more competition.

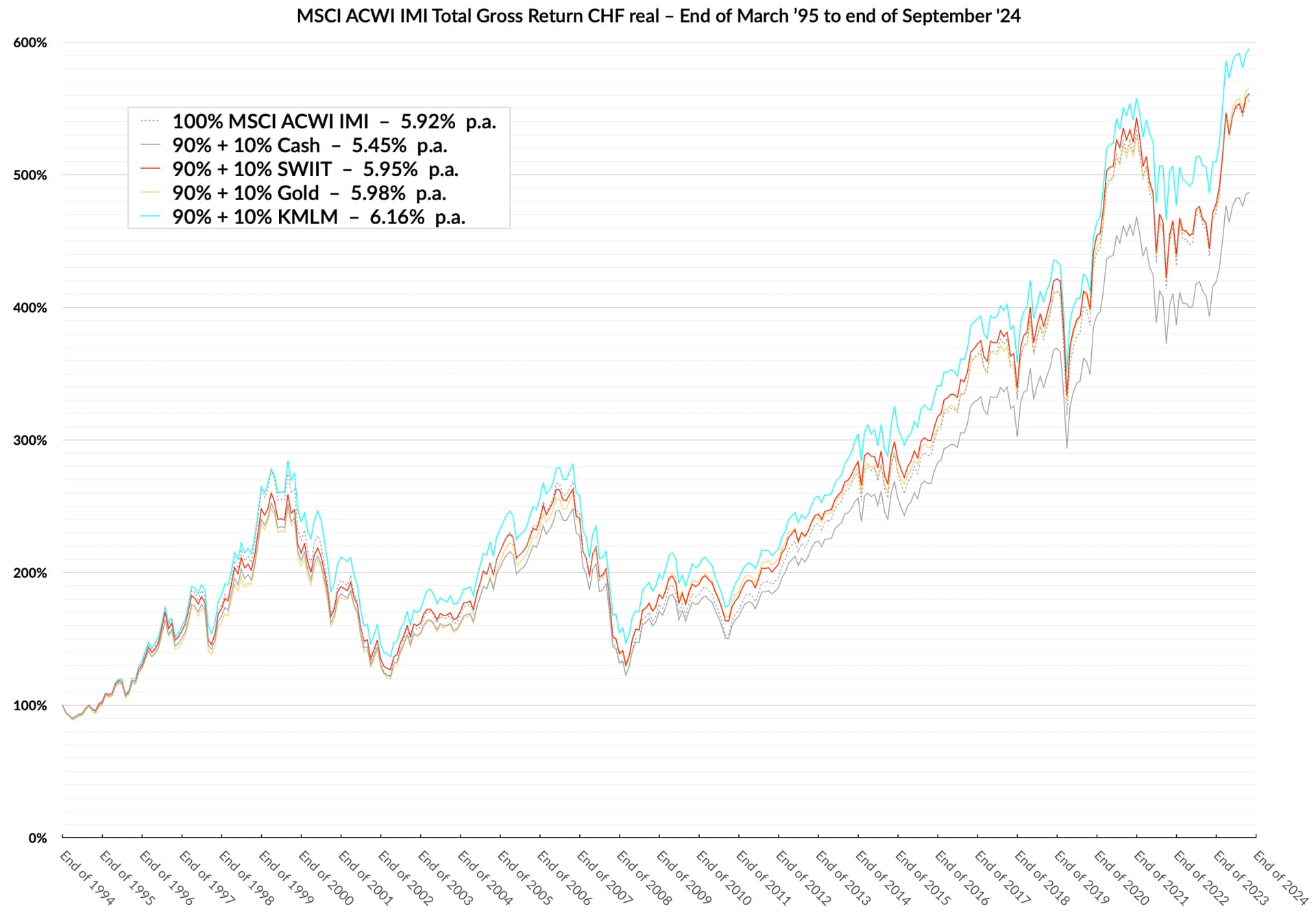

Probably because KMLM had a real bad 10s-decade, and we can not forget that we chose a starting point very favorable for stocks. The VT-DBMF-mix beats VT even with DCA.

I mean the extra performance of 70% + 140% MTBF looks great. But at what cost (risk) does it come? Leverage introduces extra cost (e.g. lending money) and more risk.

The problem with highly leveraged portfolios are that - in theory - they always outperform unleveraged portfolios. But the risk is very high. (Not sure how many can hold a big portfolio with margin. I surely couldn’t.)

I like the simplicity of VT, but you tried to show how MF can make sense. So why not use a portfolio like 90% VT + 40% DBMF. It has roughly the same performance like VT, but MF tries to up to time where stocks perform badly and it has less leverage.

In my opinion it’s also ok to underperform VT a bit, if there is less risk involved.

I’m not argumenting against the portfolios above, just trying to find a way to implement it.

I think it’s the risk parity principle. In general, to maximize your profit, you want all your asset classes at the same risk level (which should be the risk matching your risk tolerance), stock has huge risk, so you need to leverage the other assets classes.

The point is that if you have 90% VT, you should be ok with very high volatility, so if you don’t leverage the low vol stuff, you’re not on the efficient frontier.

(I say that but I have a classic 70/30 portfolio but in theory risk parity portfolio are supposed to be superior, in terms of risk adjusted returns)

The point is, that mixing in some low-correlation assets can improve all quantitative numbers (more return, less risk)

But I agree, qualitative risk changes by having debt in the equation. If that gets yanked at an inopportune moment, it won’t look good.

But there are less direct ways to get leverage than a margin loan.

The first bits of diversification brings the best improvement (per allocation size). There is no need to go full throttle on potentially data-mined high-leverage portfolios.

If one has a high enough net worth, you can also have a dedicated account at those asset managers. Alternatively, one can trade those futures contracts themselves. One can run either capital efficient at high volatility.

But both are considered your own trading activity and that can have tax consequences (professional security trader status).

I’ve been snooping around this thread looking for a potential diversifier away from equity for ~10% of my (small) portfolio for a while. The thing is, there are so many of these and I can’t claim to understand any of them, so thinking to just go with KMLM if I take the plunge, leveraging the collective power of the forum’s nitpickiness.

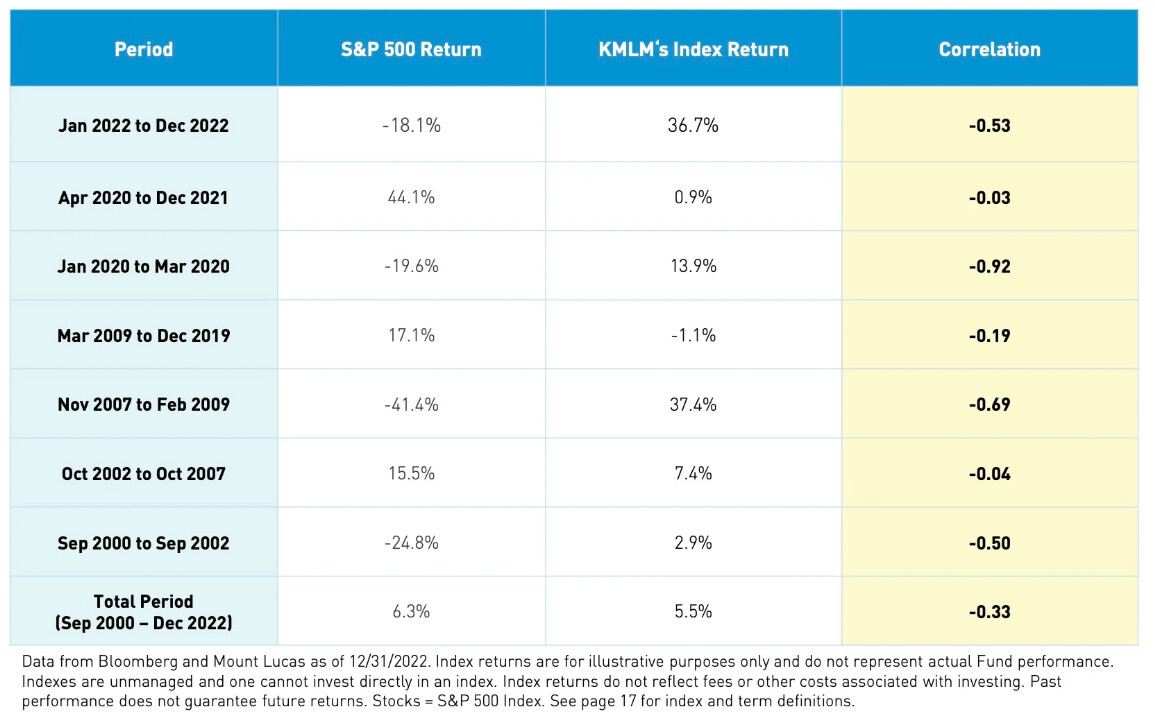

KMLM is probably one of the best ones to pair with equity, as it does not contain equity futures and has consistent negative correlation with said equities.

However, you absolutely need to be prepared for awfully long stretches of bad performance. And need to be aware of its purpose in the portfolio.

There is a saying for trend following funds:

They take the escalator down, but the elevator up.

While equities take the escalator up and the elevator down.

Meaning trend funds can have lots of years in a row where they just continously go down a little over time, but then have small stretches where they perform insanely well. Such as 2022

Equities are the opposite, most years they go up little by little, but then get knocked down by crashes in a short time.

Conveniently, the sharp up and down movements are opposite each other most of the time with trend/equities, hence why they make a good addition in a portfolio context.

My practical question would be though: what does an investor intend to do with them, other than keep as a hedge?

It’s not a trick or snide question, just thinking through scenarios: say an investor adds 10% MFs to their portfolio. I get that they will probably do a very slow slope up, or down or just sideways, until a volatile period, where they have shown they shoot up in value. What does one do in this scenario from a practical perspective.

Looking at KMLM, it did a +35% over about 9 months, and then fell back down to where it started in the next 4 months in 2022-2023 - very sharp fall, did you/would/should one sell at these spikes (of course…market timing…nobody knows when the spike ends)? If not then it’s interesting (in my uneducated opinion) as a portfolio theory idea but not very useful for smalltime retail like me in the real world.

Our perception is a bit warped, we didn’t have any longer stock bear markets for 2 decades now. Also, at higher leverage you really want to soften drawdowns.

But for the practical aspect: We want to rebalance without doing market timing based on gut-feelings. Calendar based or threshold based are both possible.

I personally use rebalancing bands. If actual allocation moves too far (some fixed relative percentage) from target allocation, I reset it to target allocation. The resulting cash (positive or negative) gets redistributed to the most dislocated allocations. For example my BTC holdings breached their band some days ago, and the money flowed into managed futures, which were under-allocated.

I think it is an ok process, but it could probably be further augmented. Maybe I could delay the breached rebalancing band trigger by some momentum based rule. I just didn’t find enough time yet to analyze it further.

The sharp fall came mainly due it distributing all these gains (majority as tax free capital gains) at the end of the year

US funds have to distribute futures gains at year end, due to regulation.

Still yes, rebalancing is key with theses funds. And something like 25/5 rebalancing bands make a lot of sense here.

They do have an overall positive expected return a couple % above cash, so don‘t only work as a hedge.

I‘ll edit some more stuff in when I have more time.

The partnership announced on Tuesday will start with an exchange traded fund that will track one of Bridgewater’s best-known strategies. State Street Global Advisers has filed plans with the US Securities and Exchange Commission for an “All-Weather” ETF, which seeks to profit in all types of market conditions by holding a wide range of assets. If approved by the regulator, it will be sub-managed by Bridgewater using its “risk parity” strategy, which uses leverage to weight assets by expected volatility.

I read that MFs need to distribute at year’s end, and also the discussion here that these are untaxable here (and long-term capital gains in the US?), but then if the fall is due to distributing the “rebalancing” is actually taking the cash distributed and plugging it elsewhere, right? Ie doesn’t need selling? Or you’d still rebalance with a 5/25 strategy anyway?

Possibly a stupid question/conclusion, but if the above is the case then it sounds like a great hands off solution.

US domiciled funds have to distribute, due to how futures work over there and they will have multiple types of distribtions at the end.

Some long-term cap gains, som short-term and also income from collateral & commodity futures.

Kind of yes, as in very good years it will distribute a lot. If your rebalancing date is at the year end anyway, could work right out essentially.

I would however say somethimg like a 25/5 rule is mire effective. As you rebalance more optimally here, due to the huge spikes that can happen.

Also you avoid some withholding taxes (on the commodity future distributions, as they come from Cayman subsidiaries and by US law count as income distributions therefore) and some of the taxable distributions, by selling earlier.

You can also use one of the ucits options, that are accumulating and have no withholding taxes at any level.

Yes I was refering to the US L2TW, just that it will be levied as the commodity exposure through the Caymans causes those gains to be definied as income. And income distributions are aubject to L2TW, unlike capital gains distributions that are withholding tax free, as well as the reimbursement on treasury income (from collateral).

I’m trying to find a new broker (for diversification) where I can buy the DBMF UCITS fund mentioned earlier (LU2572481948). Does anyone know if it can be purchased via DEGIRO, Cornertrader or Tradedirect? I tried reaching out to them but so far no definite answer and I would like to avoid opening an account to just close it afterwards because the product is not available.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.