One thing that has been bugging me since quite some time, is whether I should invest the bulk of my portfolio in VT or VWRL. I think the forum is split on the matter. Some users want absolutely the lowest cost possible, others don’t want anything to do with USA.

I would like us to debate one more on this issue. It’s an important decision to make and recent events in USA make it valid to discuss again:

Biden announced a $2 trillion stimulus plan. This could be just the beginning. The money has to come from somewhere.

A proposal has been made in California, that if you spend there at least 60 days in a year, you will be forced to pay a wealth tax for the following decade. This seems quite absurd to me, but only shows that the imagination of politicians has no limits when it comes to taxation.

To recap, the list of pros of US as domicile:

reclaim the withholding tax on dividend (15%), in theory cutting cost by 0.2-0.3% per year

higher trading volume => lower spreads

lower stock exchange transaction costs

higher AUM => more robust funds?

lower TER => is it really directly comparable, though?

Ireland:

simplicity

no worries about US estate tax

holding UCITS ETFs, not domiciled in the US

And to top it off, a poll, just to know what is your current preference.

But you’re not avoiding TSLA, are you? What’s the share of TSLA in your portfolio? I don’t think there is a difference between a US-domiciled single share and an ETF, or?

I actually have a few TSLA shares as the only US asset in my “long” portfolio, which doesn’t pay dividends for now anyway and which I won’t hold “forever” as with ETFs.

Retroactive liability I consider as very unlikely. And there are already active liabilities under the tax treaties (iirc everything beyond 5M USD in assets in US is taxed under US law, no?)

I generally will start bothering if I’m reaching those territories or if Biden lowers the amounts.

All I care about are costs and returns. I don’t have any issue with IBKR or US in general and the tax treaties exist (up to 11M).

But I’ll probably transfer chunks of my ETFs from IBKR to a Swiss broker once I reached a certain amount (200k+). So I’ll probably keep ~200k in assets in IBKR and the rest in Switzerland in the future.

Estate tax exemption has been raised to around $11 million during Trump reign. But it’s a good point. Biden could lower or abolish this exemption. I added it to the list of IE pros.

It’s important to distinguish the domicile of your assets (the ISO code at the beginning of the ISIN) from the location of the custodian. This thread is about the former. It’s possible to hold VT via Swissquote, as it is to hold VWRL via IB. Broker risk is a good point, but I guess it’s best to be discussed separately.

in the quoted post you provided has some numbers, but how should I know if it’s correct? Does the US-return include reclaimed withholding tax? If it would be the case, that the performance difference between US and IE is not a given, that would strongly speak in favor of IE, and 75% of forum members would be making a mistake.

I’d like to invest 100% in VT, save for fun bets on BTC & TSLA. And I think it’s best to keep allocation to a separate thread. I’d only like to tackle to IE vs US battle here.

and I assume if the US is like most countries, many of the proposed bills are like posturing to get media attention, not a thing that has a chance of passing (but it did succeed on the former!)

There will always be some small differences between two funds that do not track the same index. If one did better in the past few years, then it doesn’t follow that it will happen in the next few years.

Also your data might be wrong, are you sure that you used gross income and not the net income?

VT is up 80.38% in the last 5 years while VWRL is up 77.62%(Total return data from vanguard). The difference is 35 basis points per year or quite close to the ~30 basis points difference in cost + tax that you would expect.

They list the net income under gross income of the fund.

You can’t publish it because… it has data in it? So you tell me that I have to manually search for each year here, because you just don’t want to share?

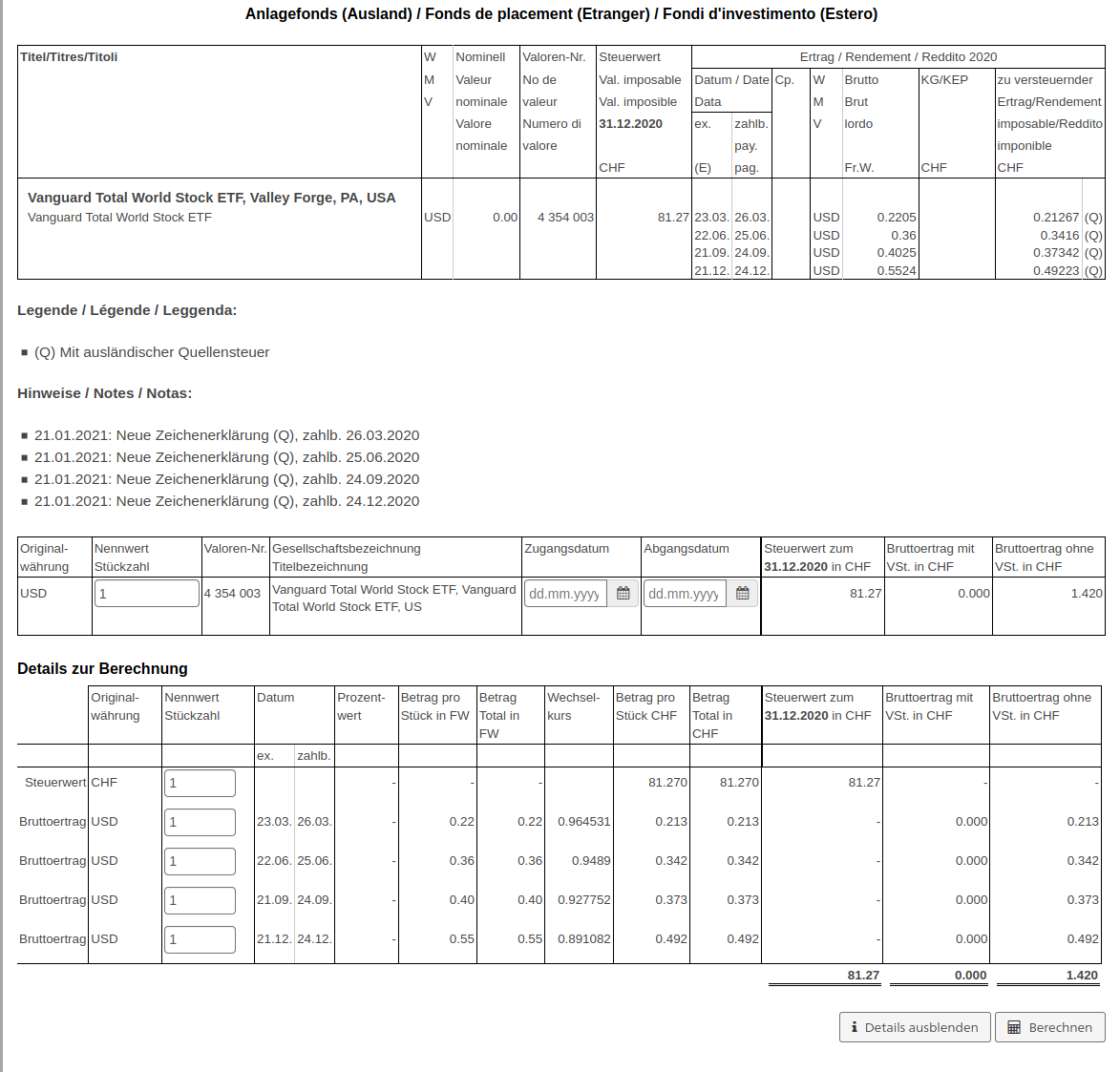

Anyway, ICTax gives you dividends and the EOY closing price, but the closing price is not comparable between VT & VWRL or between VOO & VUSA. It’s because the two markets close at different times. In a few hour, the price can change by a few percent, heavily skewing the return. How did you tackle this problem?

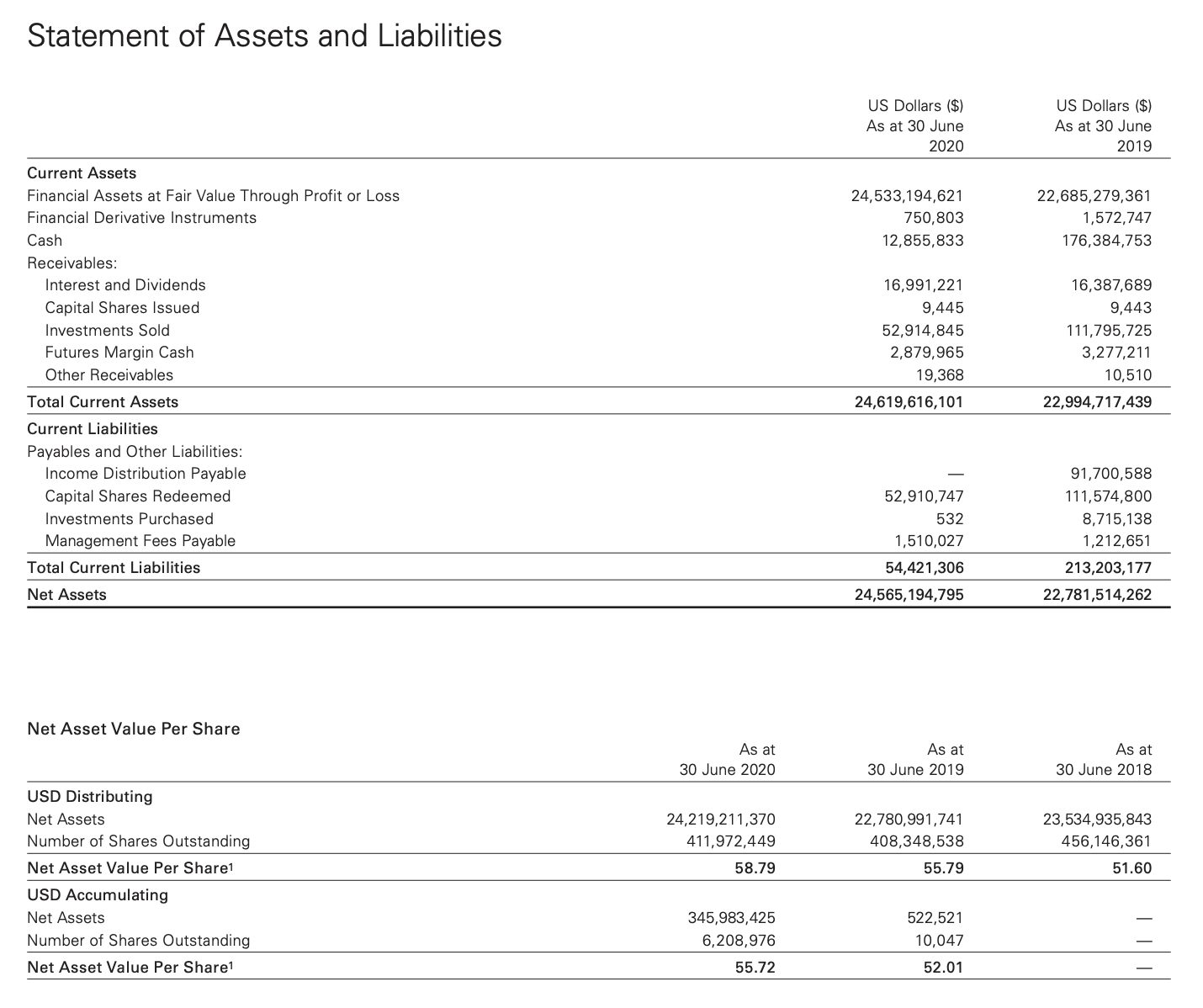

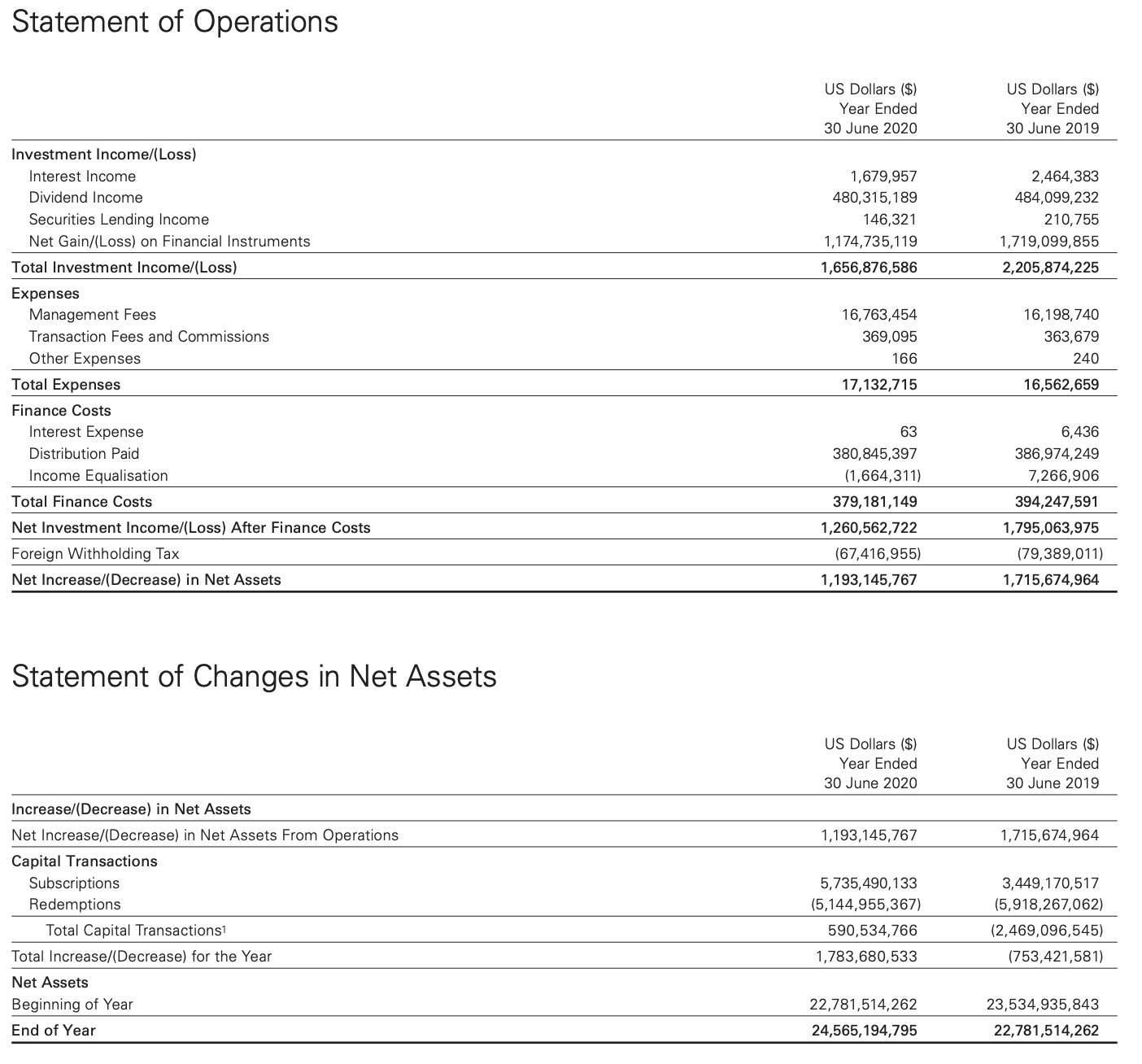

Dividend income: $480 million

Distribution paid: $381 million

Foreign Withholding Tax: $67.4 million

What would you like to calculate here? I don’t even understand why is there a difference between dividend income and paid distribution. Does the tax come on top or is it included? How to compare this to the US? It all seems a bit shaky…

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

What’s the share of TSLA in your portfolio? I don’t think there is a difference between a US-domiciled single share and an ETF, or?

What’s the share of TSLA in your portfolio? I don’t think there is a difference between a US-domiciled single share and an ETF, or?