Thanks mate. I should really stop reading 20+ different sites at once…

That’s a good one. I guess I’m going to buy a frog soon

Aside from that, I guess it also comes down to: how soon are you planning to be FI? Of course: if your time horizon until you reach FI is 25+ years, then this is ok. If we are speaking about 5-10 years until FI, this difference in returns (S&P500 vs VT/VTI+VXUS) is something which plays a big role.

Thanks for the link. Didn’t know this video yet.

Some things to consider though: he’s talking about stock picking vs indexing. Plus, he compares picking single stocks vs one month US treasury bills. The timeframe of 91 years (video was released in 2017) includes a lot of up- and downturns, plus phases of really high inflation (where T-bonds most probably were also really high). What people also fail to mention: the options for investing today are completely different than 90 years ago (indexing, prohibition of owning gold, real-time access to market data etc).

So yes: we should go for indexing, and we should thank John Bogle that this is possible for us nowadays.

Regarding the 4% of companies explaining the return: why bother owning the rest then? Wouldn’t it be enough to create indexes for top 100 US, top 100 developed world, top 100 EM? Please note that I’m playing advocatus diaboli with those two questions Still, an interesting thought experiment.

It’s still very faint but anybody else feels like things are starting to get real in the US? Of course, whether any of that would have any impact on the stock market is anybody’s guess. I’ve stopped trying to understand how it reacts (or predict the Fed’s actions and how investors react to that).

Plus, it’s an election year. Interesting times we are living, for sure.

It’s incredible that racial discrimination is still such an igniting topic. I thought that in an age where persons of color have become stars in predominantly white sports (Tiger Woods, Lewis Hamilton) and where Obama was elected president twice, the tensions would ease. But the violence of the protests shows that many people still feel discriminated.

I find it very unfortunate that some people resort to looting shops and destroying private property. These acts do not help to get rid of the harmful stereotype. It appears that the protests are not only against police brutality and racism, but also against social inequality and capitalism.

It’s awful that USA is a country where you can have the highest standard of living, with IT salaries easily beating Switzerland, but at the same time you have poverty on the streets, unsettled racial tensions and a whole lot of craziness, which we seem to be free from, at least in the majority of Europe.

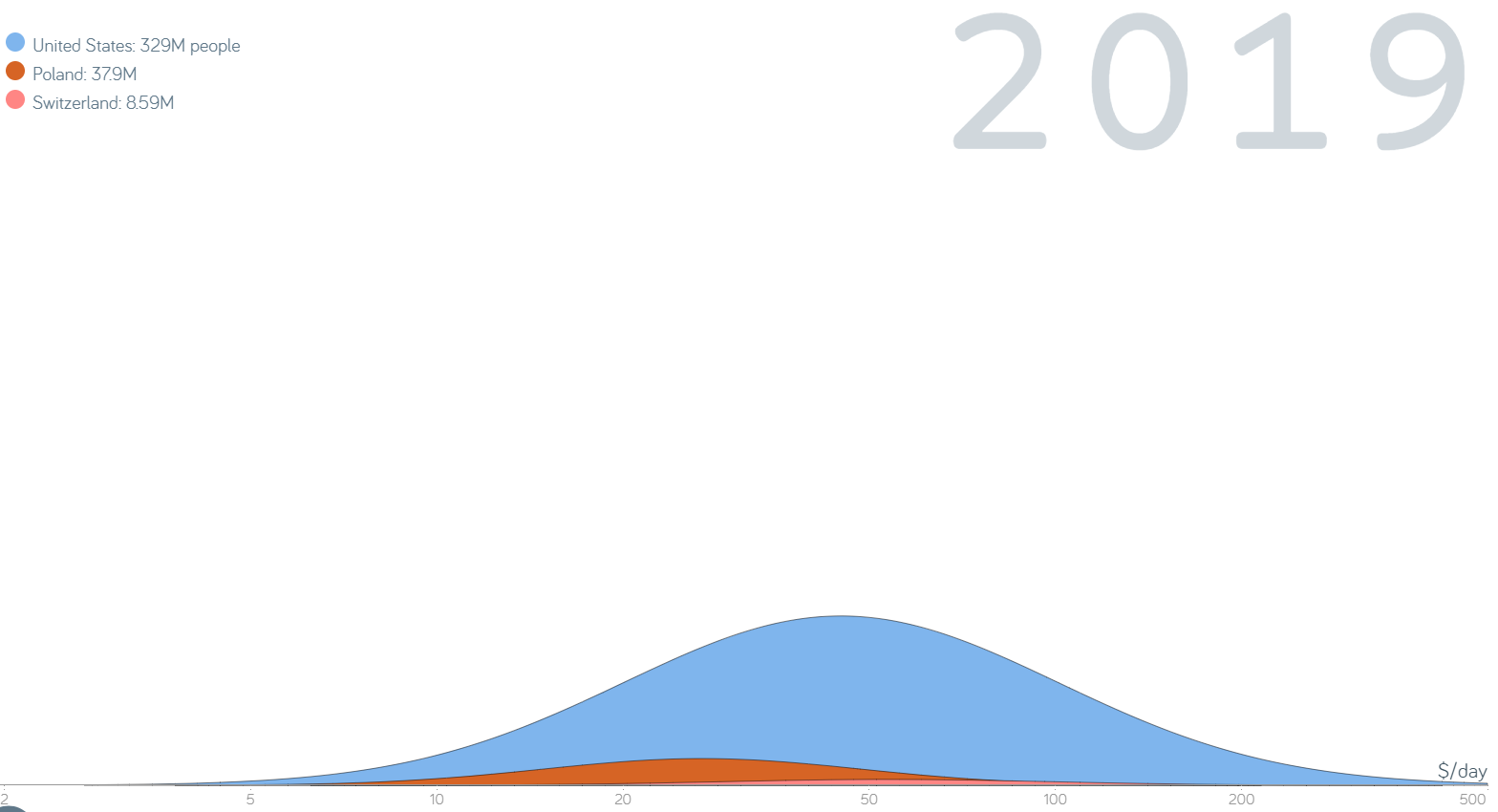

It’s hard to give a definite answer to this question. If you look at the number of people for each income level, you will see that in Switzerland the range is $10 - $200, in Poland $5 - $100 and in USA it’s $5 - $500. It’s like a parallel society where the poor and rich live next to each other. This reminds me of my visit to Cape Town, where this division is very visible.

So, no reaction from global stock markets to the protests going on. I’ve read a lot recently about the stock markets seeming overpriced and rarely having been so divorced from the overall state of economies around the world. I have 3.5k sat in IB. invest now, or wait?

Normally I’d always say “invest now, because nobody knows what’s going to happen, and overall the tendency is always an upwards one” but… for the first time ever, I’m struggling with that.

To put things in perspective:

How much are those 3.5k compared to your overall invested amount / net worth?

And how does it compare to your monthly savings?

It might be ir/relevant whatever you decide to do with it, so you might just go towards “time in the market” side, as it should win on average.

Indexing can make us loose view of the situation of individual companies. Courtesy of the bogleheads, I’ve stumbled upon this chart that shows it well : most of the economy is down but a few giants are carrying the index. I find the video in the link below particularly enlightening. Each dot represents a sp500 company, its size its marketcap and the colors sectors of the economy.

Personnaly, I’m with Ray Dalio : we are at a social crossroads. Some countries have the means to mitigate the effects of the crisis (those with debt in their own money), some are way more bound by external rules. Some people are deeply affected, some are brushing it off. The image sent by the markets breeds this idea that rich investors are getting out unscathed while the common man is suffering.

This can go any number of ways, ranging from « nothing changes » to the fall of the dollar, including social unrest and new world orders.

Things may change in the market when people/companies will have to sell their stocks to get money. The governments and central banks are trying to sustain solvency and mainly succeeding for now but this may change as the crisis draws longer.

No problem, I’ll make up another scenario for you:

U.S. presidential elections are to be held in 5 months time. Now imagine a hung vote with in one or more key states - similar to the 2000 elections and ensuing recount dispute for the Florida votes between Bush and Gore. Basically, assume the elections don’t yield a clear winner.

Only… this time Trump as the incumbent president is arguably a much, much more polarising figure than George W. Bush ever was. Add this year’s frustrations with Corona restrictions, high unemployment, poverty and racial tensions into the mix.

Given suitable election results and controversy, everything that we’ve seen lately may have been just a faint taste of the tensions, uncertainty and outright civil unrest that’s yet to come.

You’re right - it’s not a lot relative to net worth, and it’s about one month’s savings, though I’m expecting a fair few bills over the next month (taxes, Masters course fees) so maybe that’s why I’m hesitating. For once I’m going to follow instincts rather than principle, and wait a few days.

With my investments during the dip and extra revenue from salary my net worth is now back to what it was in January.

At this point I stopped buying. My allocation would indicate I should even sell some stocks… For now I am holding but if I would really follow my plan to the letter I should sell.

There’s one other bad scenario I became aware of today: A massive, rather soon, devaluation of the US Dollar. It’s a side remark in the Tagi interview with Albert Edwards, apparently quite a pessimist, but with some good arguments on his side (stock markets are high on central bank interventions, beware the hang-over).

I’m massively invested in USD assets (VT). The normal argument – to my knowledge – why this isn’t a problem is that currency movements usually are dwarfed by asset price movements, that in a globalised world in the end big companies’ earning are USD exposed anyway and that hedging is expensive.

But if a massive, US Dollar devaluation within the next 12-18 months is a realistic risk, shouldn’t I prefer currency-hedged assets? Like rebalancing from VT to the iShares MSCI World CHF Hedged UCITS ETF, for example (which I don’t much like, but it’s hard to find a CHF hedged world stock ETF).

And what makes you think that the CHF will not get devalued? Seriously, homegrown analysts who connected two dots and think they know something better than the market never cease to puzzle me

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.