This is good, just note that the minimum investment of 100k CHF is the maximum protected by the depositor’s insurance. And these are standard conditions of Swiss banks.

I got a call from the ZKB a few weeks about regarding our company account.

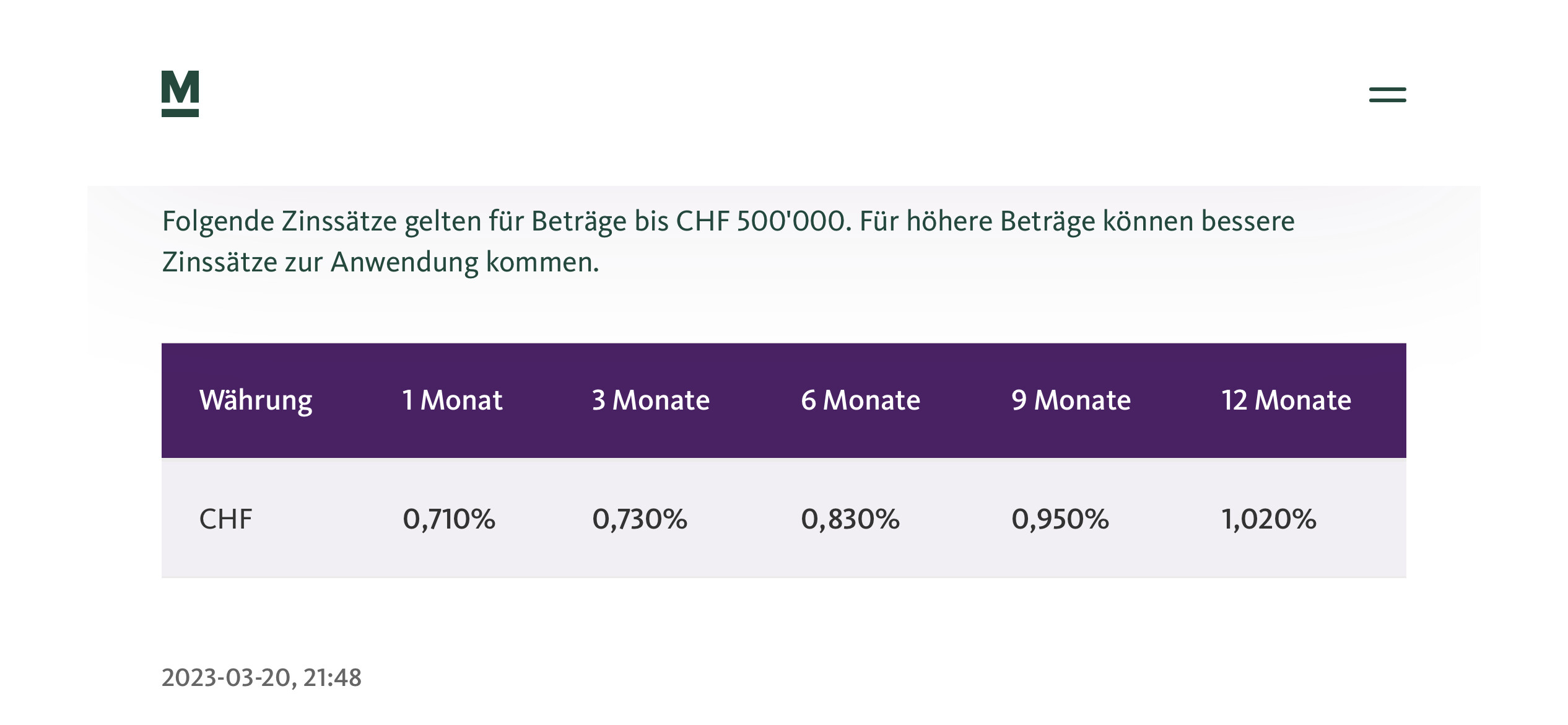

The current rate (12.07.2023) is 1.37% interest per year when you commit the money for 3 months. The longer you commit the higher the yearly interest will be. There are no further fees involved.

The only downside is that the minimum amount to commit is 100k. Unlike savings account there is no threshold where the interest will drop. To the contrary > 1 Mio. you get better conditions, at least that is what I understood. Unfortunately I am not in the position to commit > 1 Mio.

Never heard about it, no.

But would consider it at certain times, yes although min. 100k is a bit high entry amount.

Is it protected by the 100k Einlagensicherung? SGKB only refers to its safe via its Canton Guarantee. Only a few KB’s still have this, for example ZKB doesn’t have the Canton Guarantee AFAIK.

Does one have to ask the rates by mail/phone etc. (is that how you got the 1.37%?)? I couldn’t find anything on SGKB site.

edit - sorry, you said ZKB called you, so hence the rate source (in your case)

Fixed deposit accounts are becoming more common (in Switzerland medium-term notes have traditionally filled this role). They are virtually identical to medium-term notes in terms of depositor protection and interest rates, but the difference is that they are an account and not a securitized note. A possible advantage over medium-term notes is that no custody account is required. But most Swiss banks do not charge custody fees for their own medium-term notes.

It is actually opposite, ZKB has a full guarantee of all deposits by the state (Kanton Zürich), and therefore one of few commercial banks in the world having top credit rating AAA.

The interest rate is published daily so you have to inquire via telephone / e-banking. From what I understand you get payed the fixed rate on the day you start the Festgeld for the whole period you commit the money.

I know 100k is a rather large amount. I won’t be able to do this with my private accounts.

Management defined that the goal is to be able to pay the company Christmas Dinner with the interest by the end of the year

I got this offer by mail (I have a savings account there).

Bank CIC (Schweiz) AG.

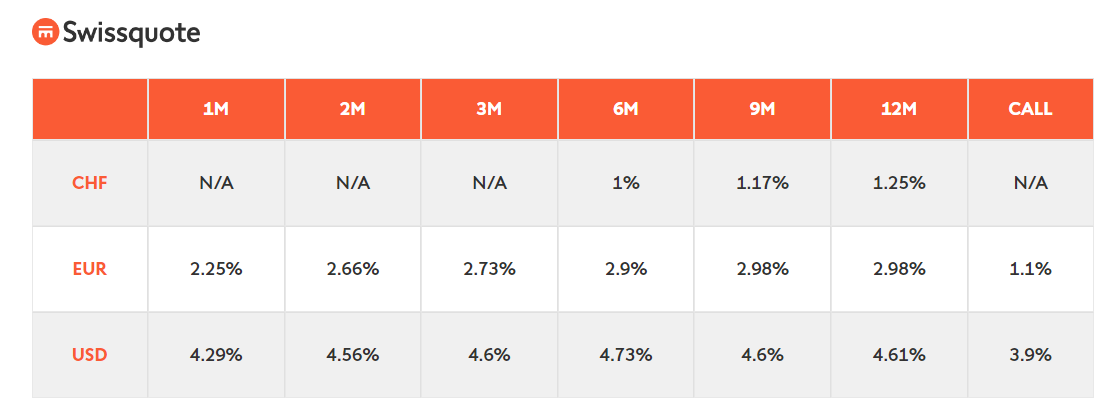

Das Festgeld FLEX, welches normalerweise erst ab einem Anlagebetrag von CHF 5 Mio. erhältlich ist, gibt es derzeit bereits ab einem Mindestbetrag von CHF 50 000. Die Laufzeit dieses Angebots beginnt am 2. August 2023. Wir können Aufträge bis zum 31. Juli 2023, 12.00 Uhr, entgegennehmen.

Die Konditionen

• Mindestanlage: CHF/EUR 50’000

• Beginn Laufzeit: 2. August 2023

• Laufzeit: 12 Monate

• Währungen: CHF/EUR

• Verzinsung CHF: quartalsweise, durchschnittlich 1,95% (Q1: 1,80%, Q2: 1,90%, Q3: 2,00%, Q4: 2,10%)

• Verzinsung EUR: quartalsweise, durchschnittlich 3,95% (Q1: 3,80%, Q2: 3,90%, Q3: 4,00%, Q4: 4,10%)

• Kündbarkeit: alle drei Monate auf den Zinszahlungstermin (3 Tage vor Ablauf der drei Monate)

• Kommission: kommissionsfrei

Do you mean “Festgeld FLEX” that I posted about on July 18th.

I felt it was the best offer atm, for CHF, at a Swiss bank, for what is essentially withdrawable every 3M.

But the way the offer was quoted to me, it was for starting latest begin August, so not sure it is still available. You’d have to ask.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.