A quarter of equities in SMI would be too much for me with the three top SMI holdings already making up 47% of the SMI market cap. Switching to the SPI would reduce the concentration risk at least a bit. I hold 10% Swiss stocks myself (also out of a total of 60% stocks) but a quarter of those 10% are invested in individual Swiss stocks with mostly domestic revenue.

Your currency exposure section doesn’t make sense to me at all. Neither is VT 100% exposed to USD, nor is SMI 100% exposed to CHF (far from it). Similar for other positions.

I’m not convinced of a single CHF bond fund, so I use a mix of the following indices / bond funds:

SBI Corporate: iShares Core CHF Corporate Bond ETF or UBS Index Fund Bonds CHF Corp NSL

SBI AAA-AA: UBS Index Fund Bonds CHF AAA-AA (I would probably switch to AAA-BBB if I started now)

SBI AAA-BBB 1-5: UBS Index Fund Bonds CHF 1-5 NSL

Global Aggregate (CHF-hedged): iShares Core Global Aggregate Bond ETF

The goal was to not have too much duration risk (reduce volatility), have some corporate bond exposure (despite higher correlation with stocks) as the yield of gov bonds in CHF is extremely low, and some global diversification (currency hedged but exposed to global interest rate changes).

I don’t think a total of ~30% US stocks is something that is too risky for now. And you allocated a sizable home bias. You could look into value funds which have lower US weights and some academic justifications. E.g. MSCI World Enhanced Value from Ishares or Xtrackers with US at ~40% weight. But Swiss tax treatment is unfavorable for UCITS dividends (dividends in general), and value has higher dividends.

Swiss CHF ETF

Echoing @jay: Use an all-caps market ETF instead (e.g. SPICHA from UBS, there is also an Ishares one). Novartis, Nestlé, Roche go from ~45% to ~35%, top 10 from ~80% to ~65%. You could replace some with SPI Mid-Size (SPMCHA from UBS). But a total of ~5% in NNR is not that concerning.

Cash

I’m not sure it is usefull in Switzerland above daily “emergencies” and short-term expected expenses. You can get immediate liquidity from a credit card. And anything long-term can only realistically be caught by social security, or a much larger portfolio, or getting more from your human capital (work more).

But to ward against a loosing access to your capital event, I would at least not put it in the same space as the rest of your capital (IBKR). Interest is 0 anyway and you need a real bank account anyway.

Commodities

I think there are better diversifiers than a long commodity derivatives basket. Managed futures (thread) would be my first line diversifier (e.g. DBMF UCITS ETF). But as with all assets, you need to have enough conviction to avoid adverse buying and selling behavior.

Real Estate

If you don’t own real estate it could be a good diversifier. Swiss real estate funds are not included in stock indices as far as I know. Funds with direct holdings (thread) have a very favorable tax treatment. I don’t know enough about this asset class to say if it is worth it. The funds are somewhat diversified but this is no index investing and there are probably intricacies that I don’t fully understand (e.g. agio).

What is your reasoning on including bonds and REIT? Ok, I can see how RE can give additional diversification if you don’t own a house yourself.

But for a 30 year old why would you bother with bonds? What’s the point if your timeline is 20+ years?

For the gold ETF the TER is something like 0.4% no? Why not go for cheaper ones like WGLD which is 0.1%?

What is the point of having a larger exposure to swiss market? Why not just weight it according to the whole world? You are already somewhat more exposed to switzerland by living/working here.

This is not a dig or even a siggestion, but genuine questions as I’m also currently restructuring my portfolio.

What is your reasoning on including bonds and REIT? Ok, I can see how RE can give additional diversification if you don’t own a house yourself.

I looked up a bunch of direct and indirect RE instruments, they come with hefty entry and exit fees in CH. Also, tbh, they did not perform that well as I expected and were actually quite volatile, so I shifted that part into equities.

But for a 30 year old why would you bother with bonds? What’s the point if your timeline is 20+ years?

This is to be diversified, inspired by the Bogleheads.

For the gold ETF the TER is something like 0.4% no? Why not go for cheaper ones like WGLD which is 0.1%?

I wanted to have a physical, Swiss-Domiciled solution where I can invest with CHF (I know, this does not actually matter because I am “buying gold“. However, I earn in CHF and I like to spend CHF.)

What is the point of having a larger exposure to swiss market? Why not just weight it according to the whole world? You are already somewhat more exposed to switzerland by living/working here.

I believe that CH economy has an edge due to monetary policy, international companies settled here, and sovereignty that will play well in this decade.

Do not forget your 2nd pillar in the grand scheme.

Many/some of us here simply count that as “bonds”, since (at least minimal) positive return is guaranteed.

UBS also offers a gold ETF with domicile and physical storage in Switzerland, and it’s also traded in CHF. The UBS ETF has a TER of 0.23% while the Swisscanto ETF has a TER of 0.40%.

but what about liquidity and spread. so many times i see a product with cheaper TER but that have very low liquidity and large buy/sell spreads which make the products quite expensive and possibly hard to liquidate in troubled times.

Is this really a problem or more a fear? (I don’t know) As I understand it, there are several market makers and arbitrage trading across multiple exchanges and even etf vendors. And if you save TER% over decades, it’s not such a big deal if you pay extra on a purchase/sale due to spreads.

Spread may be a concern but liquidity should in practice never be an issue with official ETF listings during regular trading hours as, to my knowledge, all reasonable stock exchanges mandate market makers for ETF listings. There is typically also a maximum spread defined for market makers but that may be fairly large. In my experience at SIX, spread is usually acceptable at least some time each day, even for ETFs with a very low trading volume.

I would certainly not blindly go for the ETF with the lowest TER but for long term investments, yearly fees quickly become more important than transactional costs (to a certain extent).

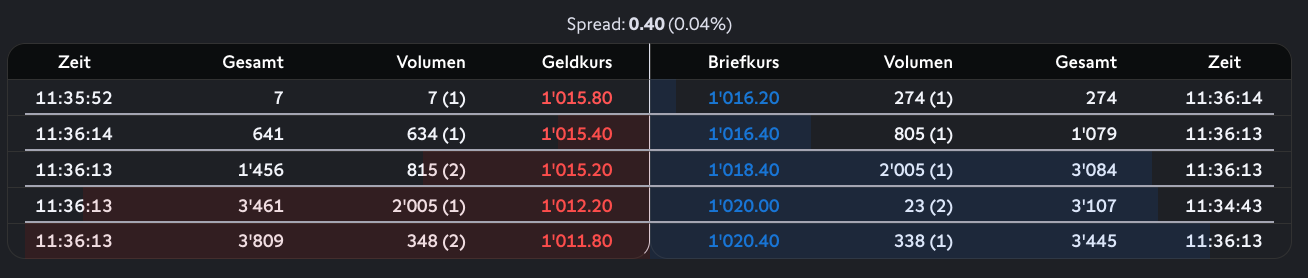

I give an example. ZGLD currently has spread 0.511% and volume of 5.95K.

GLD has spread of 0.043% (and that’s currently outside market hours!! during market hours it is probably 10x less than that) and volume of 345K.

So you have about 60x volume and maybe 3 orders of magnitude on the spread.

Now of course, how much this matters depends on how long you hold and how often you trade, but also critically if you need to liquidate something during a volatile market, then maybe the price moves aggressively against you.

That would indeed be a large spread but I currently see a spread of 0.04% for ZGLD up to CHF 7k and 0.08% up to CHF 278k. If you’re checking SIX at IBKR, you may not have the full market data.

Some ETFs have a fairly large average spread but the spread is usually not that bad the whole day. All things equal, I would certainly prefer ETF listings with higher volume as that typically results in tighter spreads, but for long term investments, I think it’s usually not a huge concern.

This may be a significant concern for active traders and may also be a concern for people that don’t pay attention to the spread at all, possibly simply using market orders.

I’m certainly not dismissing the spread concern, it can make a noticeable difference. However, if you invest long term in an ETF with a large enough AUM and not blindly use market orders, I wouldn’t worry too much about the cost of spreads.

This is to be diversified, inspired by the Bogleheads.

But bonds? Your portfolio already looks quite nice in terms of diversification. Again, not an expert, bet bonds historically were used as a hedge agains stocks, but it is not the case anymore + the returns have been abysimal.

I believe that CH economy has an edge due to monetary policy, international companies settled here, and sovereignty that will play well in this decade.

In what sense? You expect larger returns from the Swiss economy?!

Keep in mind that Bogleheads is primarily a US resource.

If you base your finance on CHF currency, high-quality bonds in CHF have very low yield. Lower quality and longer maturity hardly improve it. Then you are taxed on distributions (coupons), which are much higher than yields, and all in all you lose on bonds in CHF. International bonds won’t help: you have higher taxable distributions and expected depreciation of principal in foreign currencies.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.