Do you have a quote for that? My guess would be that the US is also the biggest market in private equity.

You can check it here (scroll down to distribution of currencies)

USD makes up 61.3% of VT currency distribution. And yes, most probably that’s because the companies are listed in the US.

I meant a quote for listed companies having significantly different distribution from total companies (listed+PE)

I’m aware that VT is 60% US listed (which in practice doesn’t mean much, all the biggest companies have global footprint and exposure).

1 Like

Yes - the biggest market for both public and private equity.

Yes - but there’s a considerable home bias in American companies (I once looked up figures and mentioned them on the forum).

There’s two way of looking at this:

a) From a purely settlement standpoint. When you have cash in one currency and buy/sell a security listed in another, you’re paying today’s exchange rate - and once you sell (tomorrow), you’ll receive tomorrow’s exchange rate for that currency pair. This is true for any currency and security, no matter if you’re buying “the world” or one country market or one single stock.

b) If, however, you look at it from a perspective of risk to (or maintaining) your cost of living and purchasing power and cost of living, it’s a fallacy to believe you’re buying “the whole world” with VT. Adnd that’s true for the currency risk as well).

1 Like

“Your time horizon matters. Your vulnerability to exchange rate volatility increases if you need to sell your investments in the short run. Longer-term investors have much less to worry about and may even benefit from currency risk. Studies show that exchange rate fluctuations make little impact on equity returns as time horizons lengthen. Economists who advocate Purchasing Power Parity between countries believe that currencies reach equilibrium over time, and therefore exchange rate fluctuations tend to net out. Many commentators believe that there’s no expected return from taking currency risk, but that it can reduce the volatility of your holdings by reducing the correlation of returns between overseas assets held in different currencies. In other words, global equities will naturally tend to hedge each other as rising currencies are offset by falling ones.”

(Source: https://www.justetf.com/en/news/etf/the-effect-of-currencies-on-etfs.html)

So, since most of us seem to be long-term buy&hold guys, I guess we can sleep tight ![]() You could buy currency(CHF)-hedged ETFs, but that’s basically a bet on your own currency, and a very expensive one at that, especially in the long run (currency-hedging isn’t for free).

You could buy currency(CHF)-hedged ETFs, but that’s basically a bet on your own currency, and a very expensive one at that, especially in the long run (currency-hedging isn’t for free).

For bonds on the other side, it’s a different story.

Here’s another deep dive on currency hedging, unfortunately in german (https://gerd-kommer.de/wann-ist-waehrungsabsicherung-sinnvoll/)

1 Like

Guys, for the umpteenth time, the quoting currency of an equity fund (ETF or not) does not matter.

If you buy an equity ETF, you buy a collection of businesses. The only forex exposure you will have is:

- In which currency these businesses collect revenue

- In which currency these businesses have to pay their expenses

That is, compared to the currency of the country where you live. That means that yes, you should evaluate the performance of your holdings expressed in the currency where you live.

Even if you bought a swiss fund, quoting in CHF, buying only a swiss index made of only Swiss companies whose headquarter is in Switzerland, you would still have a very minor exposure to CHF, and most likely a huge exposure to USD.

Don’t believe me? Let’s have a look at Swiss blue chips:

-

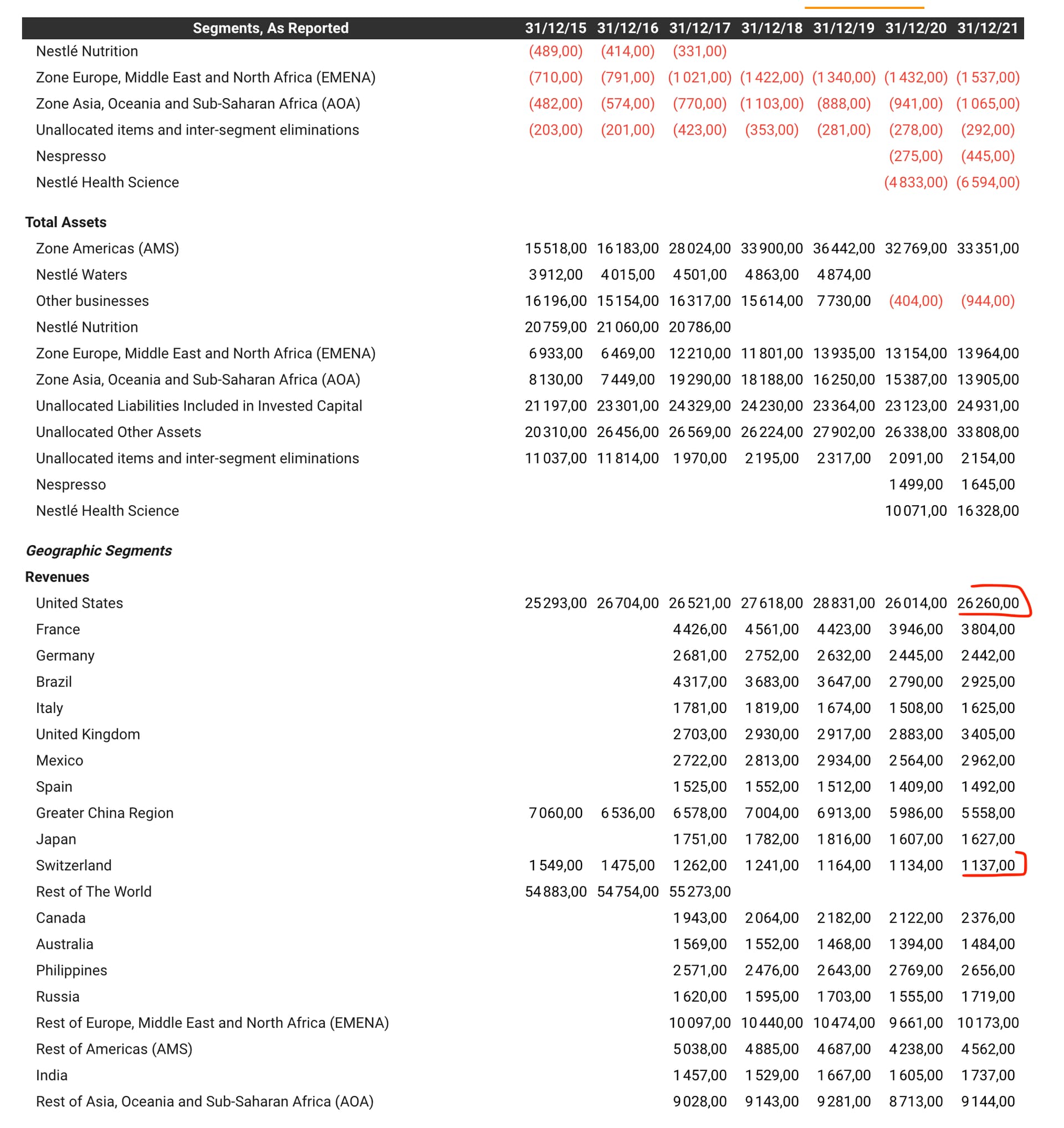

Last year, Nestle made 26 times more revenues in the United States than in Switzerland. Even the Indian business is bigger than Swiss revenues:

-

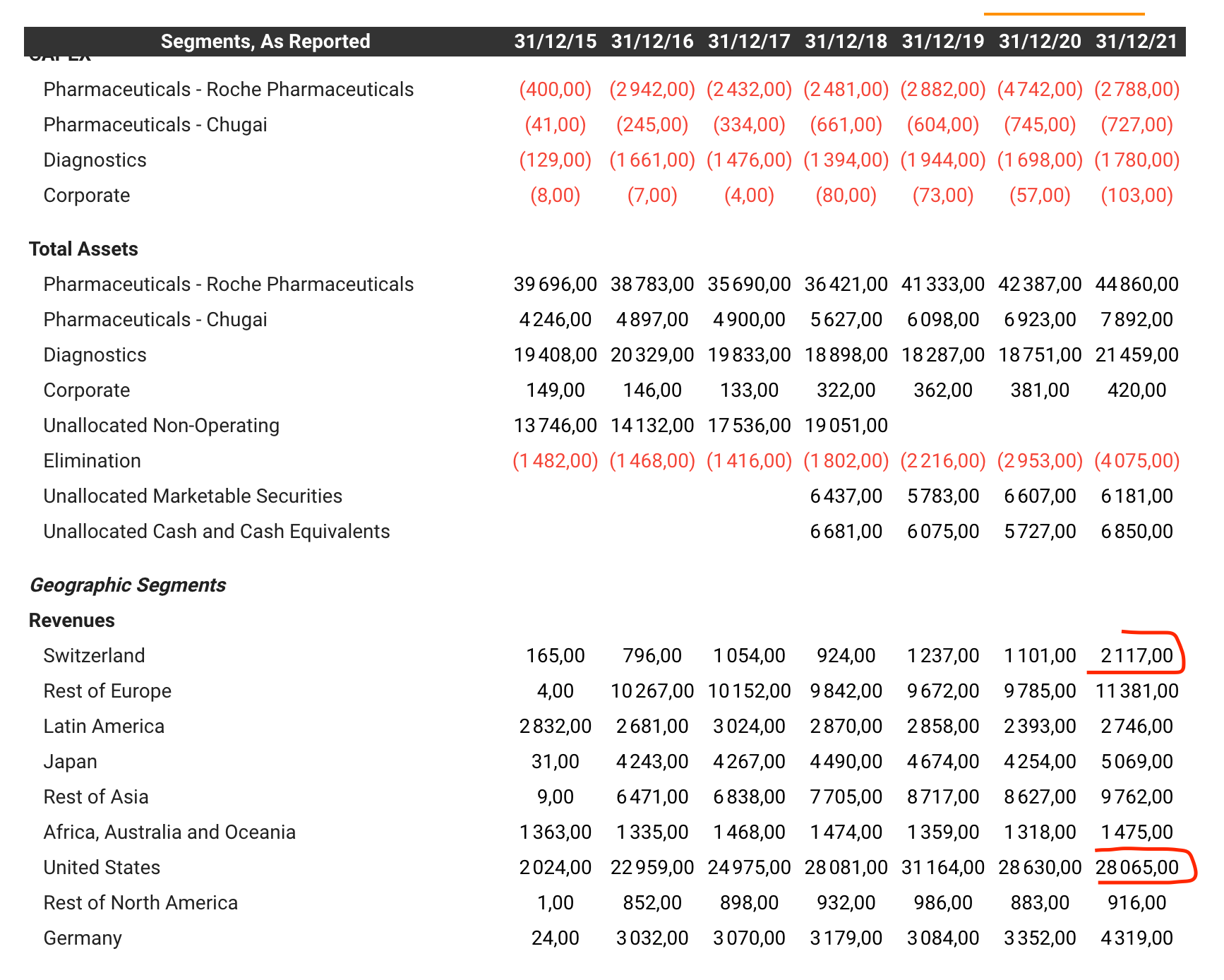

Roche made CHF 2.1 billion revenues in 2021 in Switzerland, and… the equivalent of CHF 28 billion (that is, roughly USD 28.8 billion) in the United States.

-

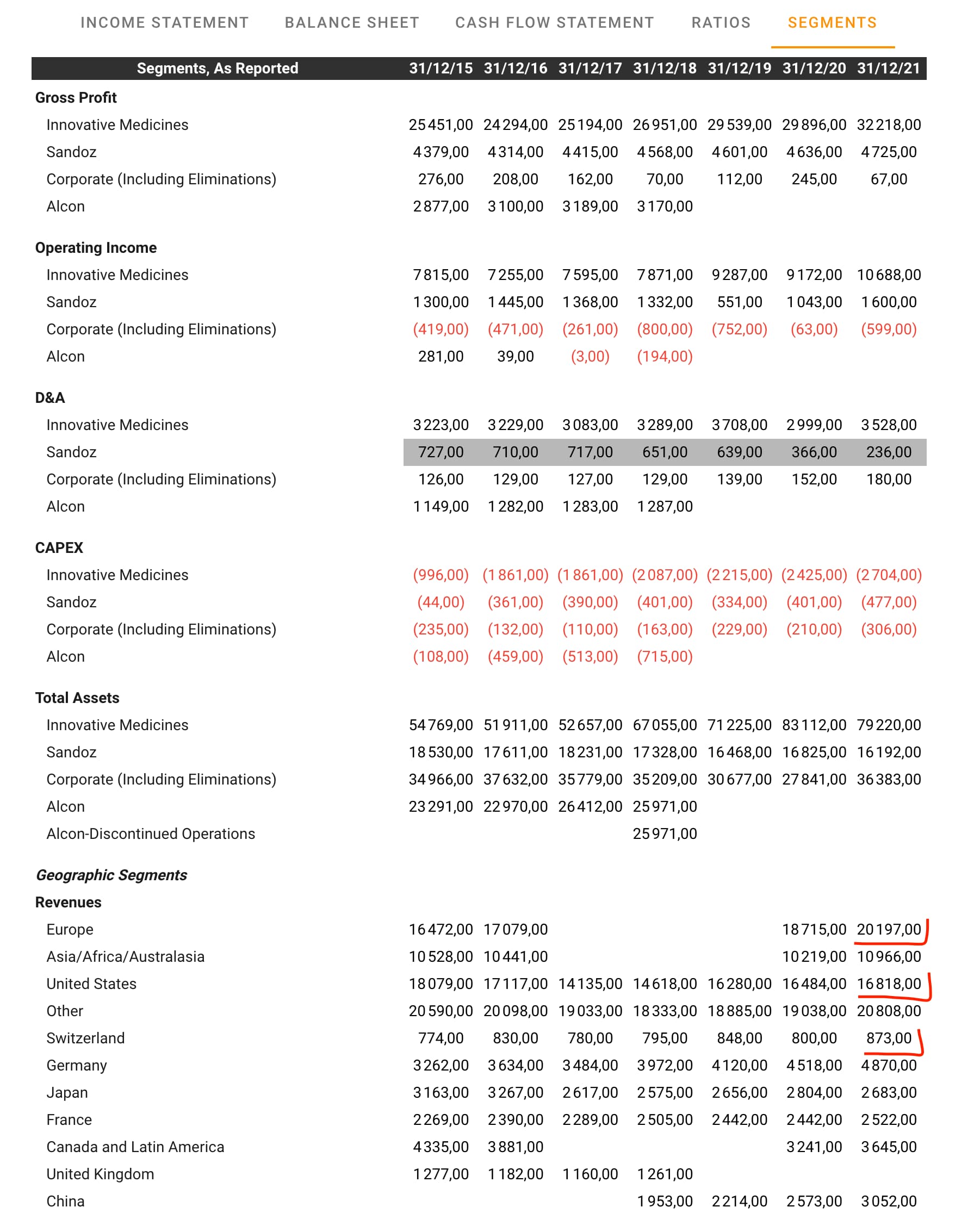

Novartis made CHF 873 million revenues in Switzerland, but made the equivalent of CHF 20.1 billion in Europe and CHF 16.8 billion in the United States.

You get the idea. Your exposure to foreign currencies (USD, EUR, etc) would likely be more than ten times bigger than your exposure to CHF.

And frankly, I would not sweat too much about it. First, it would be next to impossible to hedge it correctly (with companies weight in the index changing regularly, and business performance in each region of the world changing every day). And second, I’ve never seen a successful investor who said “you know, what saved me was to hedge currencies.”

20 Likes

Plus those companies are maybe hedging their FX risk to some extent anyway.

4 Likes

bottom indicator will be when Wallstreetbets has a lot less activity…

1 Like

Looking at the news headlines, I feel we’re approaching the bottom: It’s pure fear and pessimism.

Still, I find we’re nowhere near a dramatic correction, it’s more like crybaby-time for spoilt investors from the last decade.

Trying to think of a juicy headline to finally bring VT below 90, there’s still some panic missing in mix ![]() C’mon guys, what more do you need? Santa Clause is officially fake news? Mustachian movement killing global consumption?

C’mon guys, what more do you need? Santa Clause is officially fake news? Mustachian movement killing global consumption?

1 Like

brings foreign investors buying US Treasury bonds with finally a positive real interest rate and pumping USD/everything up. Which is beneficial for us, ex-US investors.

1 Like

The past 2 crashes took 1.5-2 years from peak to trough and ~5 years to get back to all time highs.

MSCI World, USD, Gross dividends reinvested:

We can’t time the bottom but my hunch is that for anyone with a long investment horizon now onwards will prove to be quite a good time to have been accumulating via Dollar Cost Averaging

4 Likes

Starting to DCA here is not wrong, but you have to be prepared to see more red to come.

4 Likes

IB shows me 90.04 for VT…

2 Likes

I assume a similar scenario. Also, the returns over the last decade were quite high, so I expect a longer consolidation phase over the next couple of years.

1 Like

VT is below 90 now. Who’s sweating?

2 Likes

I am ready to make a friendly bet that in May VT won’t go below 86 CHF, which was the minimum in March. After sliding down for 5 weeks and dropping by 6% in three trading days, any good news can cause fireworks.

1 Like

Damn, my bank hasn’t transferred my dry powder to the broker yet, can’t believe how prehistoric our banking system is ![]()

Where’s the whole disruption promised by the crypto/defi-bros?

1 Like

Q3 2024 the new instant payment system by SIX (SIC5) will be launched.

9 Likes

Well, if VT continues tanking until the wire comes through, I’m personally gonna congratulate my house bank on its prehistoric system ![]()

Actually, prehistoric wire speeds prevent market timing, which might be a good thing for me ![]()

2 Likes