done. need more? ![]()

I‘m not a chart specialist but there are some interesting pictures with (death) cross where we see bigger indicators as the 200d EMA been crossed downwards. While I continue to accumulate my monthly VT, I think I will reduce the amount of these and try my luck with some short mini futures to gain some leverage. Does anybody try to do the same (knowing that it most likely does not work out  )?

)?

That is normally not part of my investment strategy but only buy and hold is sometimes just boring

Don’t use leverage. Leverage killed Long Tetm Capital Management, leverage was one of the major issues of the 2008 financial crisis. Always keep in mind that leverage works in both directions and it’s devastating if it works against you.

Compounding a lot of money in the long term is not boring for me ![]()

6 Likes

I know that making money is not boring but I did that also in the past besides accumulating VWRL and VT as main position playing some site games with mini future, meme stocks and shitcoins. So far the outcome was overall positive. However, it took me some time to investigate etc compared to 10min of monthly effort to buy ETF‘s. It will always be just a small part of the portfolio about 0.2% per trade and only one trade at the time. As a summary I know it’s probably not the smartest solution (guessing it would be smarter to put everything in VT) but I like it and it is fun to feel the emotions which you do not get if you buy and hold ETF (that‘s the point of ETF to not get yourself uncomfortable  )

)

Not sure where’d you see -20% happening?

1 Like

Not sure either but I checked some charts from growth companies with low earnings like Netflix, zoom, some biotech stocks and they all look quite bad from a chart perspective. I’m aware that if the FED changes the game again that would look quite different but with real inflation and interest raising I‘m confident that some of these stocks will have a hard time in the near future.

1 Like

Exactly, I fully invest in VTI. I was doing so. As I said previously in the other post I am thinking to switch from VTI to VT this year, I have all there. The main reason for me is to have even more diversification. At the moment I don’t like to have everything in the USA market (rationale for me is the risk to have it in one market, also I think in the long run USA will not be as strong as it is at the moment.).

Also, another member of the forum commented that maybe keeping them and buying another two ETFs for the emerging markets with a lower TER than VT is also a good option (like VWO).

1 Like

let me share this one here (especially about the “dips” that take forever to reconcile).

I like the guy’s analysis a lot, comments welcome where you think he might be wrong.

1 Like

And increase the risk of never reaching FIRE.

1 Like

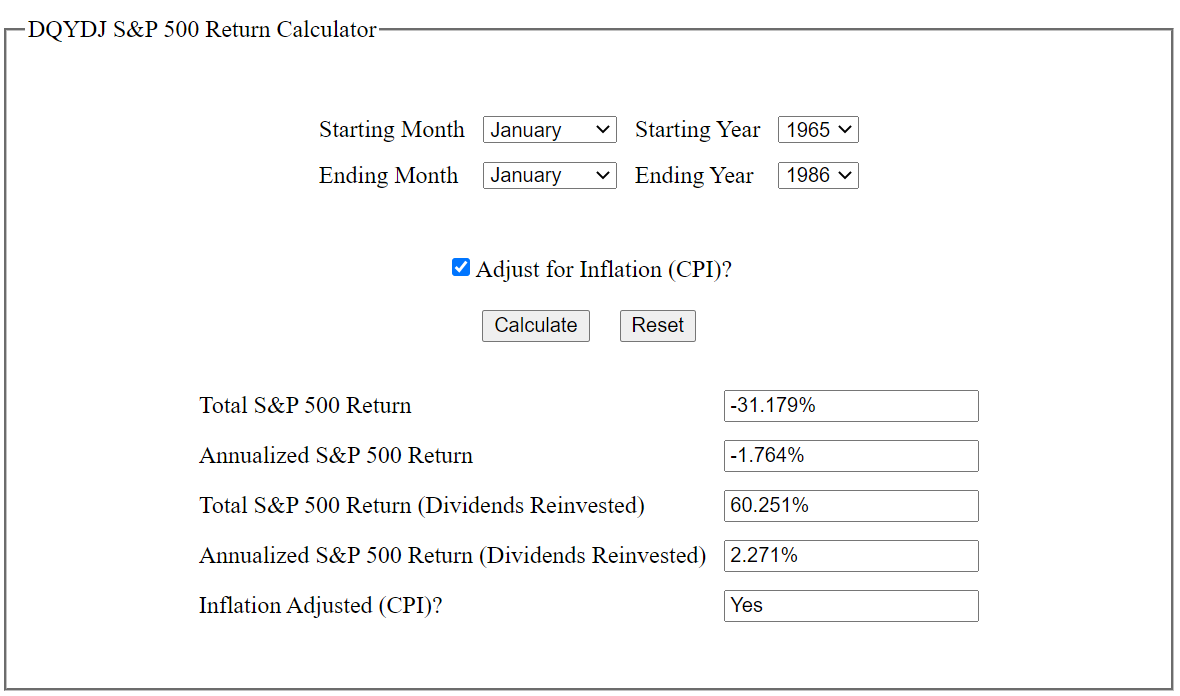

His claim around 6:20 that you had to wait for 30 years to start making money relative to inflation is just wrong. He’s making a typical mistake of looking at S&P price chart while ignoring dividends.

If I look at total S&P return from '66 to '95 I get something like 21x return, while cumulative inflation in that period was just below 5x. (using https://www.usinflationcalculator.com/ and S&P 500 Total Returns by Year Since 1926 for data sources).

4 Likes

And can actually increase the chances of Running out of money in retirement

3 Likes

The trick, of course, being to design a plan we are able to follow. Behavioral mistakes can kill an early retirement plan more easily than a small allocation to bonds.

Better an imperfect plan we can stick with than a perfect one we’re going to drop at the worst possible time.

2 Likes

True that. But even then, 20 years without any real risk premiums compared to bonds (at the time) are probably out of bounds for most of us

Indeed. As always « it depends » there is no black or white answer

1 Like

On the topic of 2022 strategy, this recent article from Jeremy Grantham (GMO) has been in the news lately. Personally I am torn between “history will repeat itself” vs “this time its different”. One can find counter arguments to his point as well such as all the money needs to go somewhere. In any case I have decided to reduce downside risk by opening positions in some of the less overvalued markets (European Prime Value, Japan, etc). I am not brave enough to short growth stocks - been burnt before. Eager to hear your thoughts …

My personal thoughts are that history rhymes, but the verses don’t all have the same number of syllables, such that it’s impossible to tell with enough accuracy when what will happen. It’s probably a good time to reassess our risk tolerance, but downturns can happen without warnings, so we should rather be ready at all times.

In the same vein, efficient shorting requires being right on the direction (down) and the timing of it. That last part is the trickier of the two. On top of that, the downside is unlimited but the upside is limited. It’s possible to go broke shorting the market, so I’d say It’s a loosing game for retail investors such as we are. I wouldn’t wander on that path.

4 Likes

That’s how every crash started, it’s always the same.

1 Like

I head someone on YouTube saying that value stocks are making a comeback and money could flow into them from growth stocks. I understand very little about growth/value etc, but I wonder if you guys think that YouTuber had a good point or not.

'Murica has a huge plan to “rebuild”, that includes a lot of construction, highways, manufacturing critical stuff (like the Semiconductor Foundry of Intel), energy networks (utilities), transportation.

These things have been in the “value” business so far (except chip makers), so they might overperform, especially if growth stocks with ridiculous valuations get further plummeted.

1 Like

Predictions are very difficult, especially about the future ![]()

True value stocks are never out of fashion, if you buy them with a high enough margin of safety. The problem is, that it’s extremly hard to find such stocks at the current valuations.

1 Like