I like the REIT portion of your real estate, but I’d feel inadequately equipped with enough conviction about the Home and Rental part of your portfolio mainly because of (my) liquidity concerns. It seems like about half of your assets are in essentially mostly (at the most times) illiquid assets?

I sort of understand the Home portion of it, because of … attachment to the place / emotions (at least I would feel that way if my landlord decided to sell). Completely rational? No. But emotions have their way of sometimes trumping rational thinking.

Overall: if liquidity is indeed only a qualified very distant concern of yours, then it’s a strategy I could perhaps live with. Still somewhat uncomfortable from a liquidity perspective. And probably would still like to see the cash flows attached to those allocations, though, to feel comfortable with this kind of capital allocation.

The REIT portion of my portfolio is in the deep red since interests rate started going up and TBH I don’t think I’ll buy more of it, especially given the massive overall RE exposure.

I am not at all happy with the current amount of RE and the plan is to stop buying anything else while keeping adding to the stocks/pension parts. I am not really concerned about the illiquidity at the moment as I don’t plan to sell any of the properties any time soon.

Cash flow is yet to be seen because I am still renovating but if things go according to plans/forecasts I should be getting some ~70K/year of net income, or ~14% ROI (quite high because one property is an inheritance and I am only considering the money I invested to renovate it).

I get your point and quote the compliment. Thanks. There are no connections to the construction business, but everyone needs a place to live, right?

At this point I don’t worry about market values. I don’t plan to sell any time soon. Still, it’s an asset and the money put there would otherwise be part of the other slices.

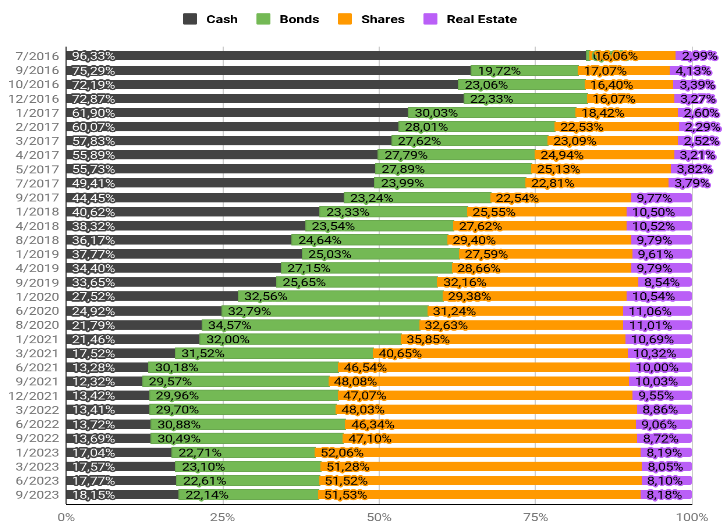

I like to keep the history since I started to define a targeted allocation.

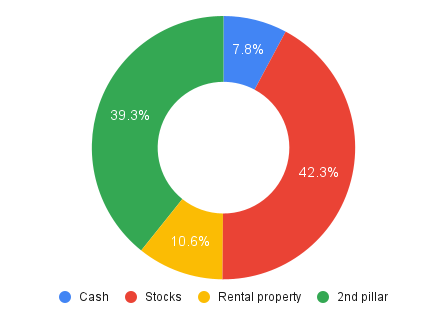

My objective is 70% share (including 3rd pillar)…

The second pillar is including in the bond allocation

I debated whether to deduct withdrawal taxes. But I wonder why we do this and few of us consider doing the same to calculate property net of capital gain and property gain taxes?

I guess more people see it likely to cash out 2/3a pillars while much less likely to sell properties. I am one of them. Also, property capital gain tax is more complex to estimate.

I started recently with investing in stocks so my allocation is still not relevant

Overall is there any rule or, let’s say, desirable asset allocation by %?

Furthermore, my current cash position is high - we have some savings related to a down payment of our future real estate that we projected to buy in next 3 years. Is there any clever advise what we can do with this money - i.e to invest in some bonds or similar? Obviously a time horizon is too short for investing in stocks.

There is no general rule as the asset allocation is individual to your risk profile, meaning how much risk you are able to take and how much risk you are willing to take. Search online for investment risk assessement or similar and you’ll get some questionnaires, which will help you in assessing your risk profile.

I already did it before - my profile of investor is something like moderately aggressive.

I thought that maybe some “Mustachian” approach is already developed

If you have some specific thread on top of your head, do you mind share it?

How do you guys calculate your saving rates? Do you take into account your 2nd pillar or not?

I was calculating without, but after reading some posts/topics, now I am confused.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.