[update]

by now i think the numerical deviation simply comes from rounding errors, based on very small absolute values.

the sales & purchases in March are due to the switch of VZ towards indexfunds and should be a unique thing. That’s what the guy said

Rebalancing check is monthly. The exact conditions for rebalancing are proprietary. Mainly if you add funds, change the strategy or some deviation thresholds are met. for my passive45 mode these conditions were not triggered since 2015 (apart from adding funds by me).

I will soon switch to a 80% (maximum) stock strategy. let’s see what happens

I’m trying to compare apples to apples when looking at VZ versus Swisscanto at LUKB, and the TER seems to be respectively 0.68% (all-in) vs 0.60% (0.25% management + 0.35% underlying funds’ TER). I see a Kosten p.a. column in the VZ Titelliste, is that already included in the all-in fee, independently of the fund you choose?

No, the individual fund’s TERs must be added on top of the 0.68 allin fee. so you should correct the 0.68 to 0.78-0.98%, depending on your choice of funds. the 0.68% are billed quarterly, the fund’s TER are not explicitly billed but payed as the funds take out their fees from the fund assets.

Your guy seems to be making an abstract argument against stock picking and day trading in general if you look Into his reasons.

My guy’s main argument is more about a concrete point about current state of the market: diminished risk premium compared to investment grade bonds. You’re sponsoring junkiest junk on earth (euphemistically called “high yield”) and after the big rally in prices you’re now paid just barely above what creditworthy companies pay plus default rate, and the outlook is not so good that there’ll be buyers for these bonds if a mass exodus out of these ETFs starts

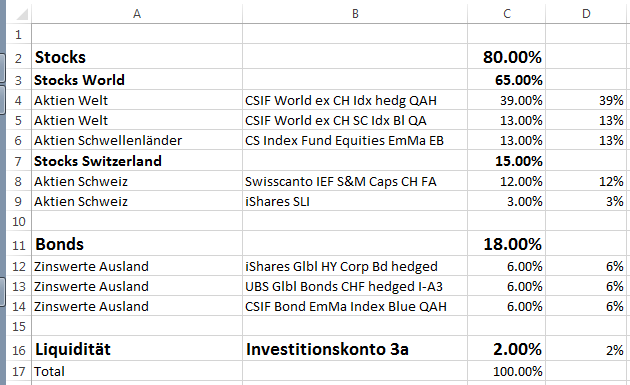

After some optimization I now have the following Strategy: 80% Stocks:

39% World ex Swiss CHF Hedged: CSIF World ex CH Index Blue CHF Hedged

13% World ex Swiss SC: CSIF World ex CH Small Cap Index Blue

13% EM: CSIF Equities Emerging Markets

12% SPI Extra: Swisscanto Index Equity Fund Small & Mid Caps CH

3% SLI: iShares SLI

18% Bonds:

6% World Gov: UBS IF Global Aggregate Bonds Passive CHF Hedged

6% Dev. World HY corporate: iShares Global High Yield Corporate Bond CHF Hedged

6% EM Bonds: CSIF Bond Emerging Markets Index Blue CHF Hedged

2% Cash CHF

I take full advantage of the 80% stocks allocation, which is the currently known maximum for 3a Investments. The 13% of world SC & EM add up to the 26% of non-CHF-non-hedged assets (the 27th percentile was not allowed in their selection mask). 2% cash are also required. the remaining 18% are evenly spread over different bond markets. with a total average TER of 0.2435% and 0.68% allin, I own this portfolio with at total TER of 0.9235 %, plus swiss stamp taxes on transactions.

The high TER and restriction in Product choice make me reconsider if i put money there in the future. but the money i put there already is now put to good use.

Do you have a limit to world stocks hedged allocation ?

i think not, maybe 80% of this would be possible.

Switzerland don’t have to be too overweighted.

This is a matter of discussion and personal preferences. I see both a reason to set it to 2.7% (=share of swiss stocks in Vanguard total world stock fund) or 100% for elemination of currency risk. everything else is quite the same arbitrary.

may I add that no transaction cost of rebalancing apply, which for a hypothetical portfolio of CHF 20’000 and 8 assets easily goes to CHF 80-200 per year (assuming CHF 10-25 per transaction), in this example 0.4-1%. Then this 0.92% s not so bad anymore. Including transactions after adding funds, this is not bad at all. for larger 3a pillar sums, it becomes less favourable ofc.

So today they rebalanced (=implemented my new individual strategy) at VZ. It did cost only the stamp tax, and it was 0.03% of my portfolio (selling and re-buying the whole amount). now it looks like

80% Stocks is the max, also 2% liquidity is required. the non-swiss-non-hedged part is limited to 27%.

I think this is about the most passive-indexing-longterm-investment thing you can currently do within the 3a framework. it comes at the cost of an 0.68% p.a. allin fee.

the small cap is a personal preference of mine.

i have emerging markets (3rd position) in there, 13%. it is not hedged to CHF, that 27% cap applies. i filled those 27% with small cap & EM stocks

@Nugget:

Same question as Zugzoo, did you change the allocation?

Also you were saying that high TER + restricted products will make you reconsider putting money there in the future.

What else do you have planned?

I just moved to Switzerland for my first job ever, and I would see myself staying here for a long time.

I’m interested in the 3a+3b as a way to invest passively (Set up an easy portfolio that re-balances automatically) and as a bonus get the tax deduction.

That’s the ONLY thing you’re getting out of it, don’t get fooled

It’s expensive. Unless you have a short enough time horizon before withdrawal, high tax burden, mortgage to pay back, or just want to keep a lot of spare cash in portfolio, I’d avoid 3a.

Forget about it, it’s not tax deductible. Just a con made by banks to fool you into giving them more money

Thanks for your message.

What do you mean exactly by spare cash in portfolio?

What would you advise for someone in his early 20s that wants to start investing 1,250-2,000 CHF a month?

My plan so far was to add 500 to my safety net (currently has equivalent of 4 months of living cost) & 750 in 3a+3b at VZ with a portfolio similar to what nugget has on this page.

I have another 750 that I can invest without an issue and I’m wondering what’s the best way.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.