Dear all,

is there anybody considering to make use of the VZ products für 3a savings?

they recently allowed to go 80% Stocks and you can define the ETF allocation yourself to a certain degree.

However I still dont get all the info I’d like to have - anyone in the same situation?

I am in the same situation. I recently put alot of thought into my retirement plans. I also stumbled over the new possibility at VZ now that you can invest up to 80% in stocks rather than 45% earlier. (that nowadays Bonds especially swiss Gov Bonds are no option no more… need to stay in cash)

I opend e 3a depot at VZ after mailing to a senior officer from zurich HQ. Unfortunately the new release that you can chose your own ETF-Portfolio will be launched sometime in February (For now you can only invest 80% in stocks with the standard investment profile nr. 7… no option for me so i have to wait until releasedate.

But i hope it is worth while because with the new release you should be able to pick more than one ETF in every asset class. eg. for international stocks there should be the db x-tracker msci world ETF and also a hedge CHF Version of some Credits Suisse institutional index fund covering msci world ex CH. If this is true my plan is to invest my 80% in a combo of these two in order to comply with currency max regulation (I dont want to invest in the narrow and home bias SMI… if i wanted i would just buy Nestle, Roche and Novartis stocks ;).

Another Question for me is if i should put the remaining 20% into the SXI Real Estate Funds or leave it cash. The SXI is quite expensive (there are alot of costs hidden behind the fund of funds construct 0.25% ter is just the cost of the ETF itself so it will sum up to 0.8-1%) Gold or Commodities is no option as well as the bonds as i mentioned above.

I should get an email from the customer service as soon as they launch the new release. will come back to tell you more after that.

Hey @basilisk,

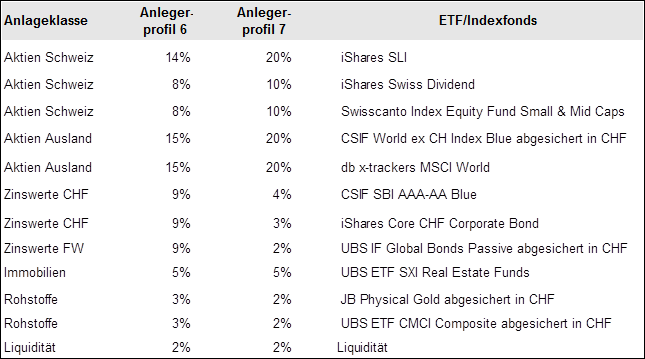

then we are quite on the same page. I am glad to finally find someone wh o can discuss this in detail with! For everybody, here is a fund list. these Funds should be available for the VZ depot soon:

to me very interesting is the Swisscanto Small & Mid cap. But they did not specify which one - there is more than one with that name.

Also special interes cought an email i recieved, stating the Vanguard FTSE All-World High Dividend Yield should become available. since 3a is tax-free, there might be some incenitive to pick this one.

@real estate:

I agree taht these funds are really expensive beyond what is written down.

@hedged: it is rather common sense among swis mustachians that hedging is of no use in the long term. however, in case the TER is still low…

what would I do with the 20% non-stocks? is cash better than real estate on the long term? i guess not, but who knows.

@Nestele, Roche & Novartis

they are contained in any all-world stock ETF or Europe ETF. Together with other SLI titles, this makes me look at the SPI mid (not in the list) and the swisscanto ETFs since my non-3a portfolio is 20% Vanguard FTSE All World.

Now, i still have questions^^ considering the current list of ETFs (the above list is not yet official afaik)

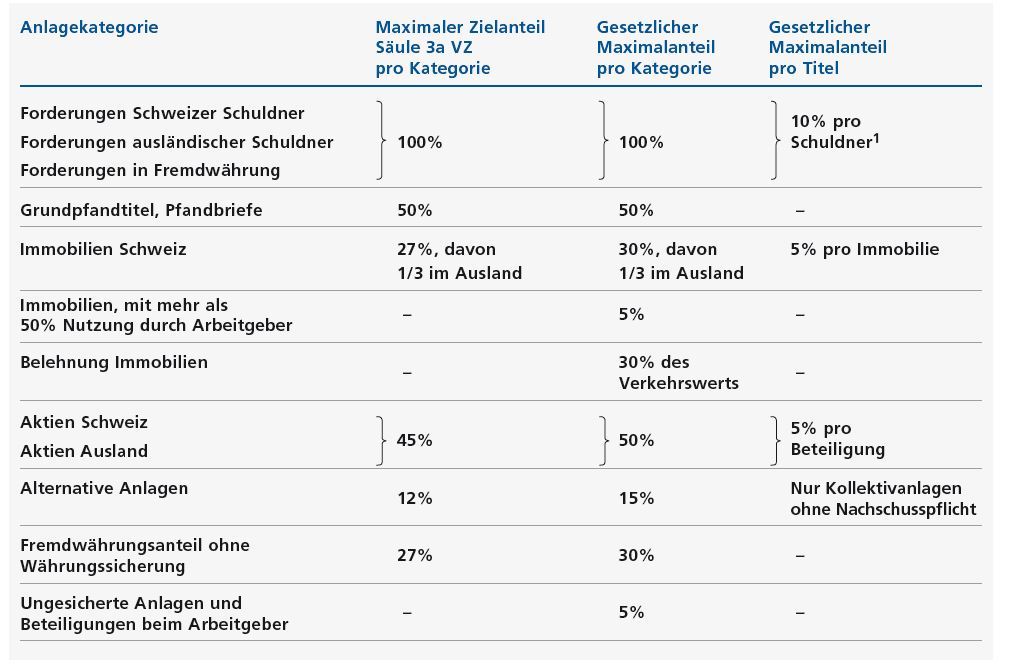

the stock limit is 50%. Now they raise it to 80% - why is 100% not possible? Is it really, based on hard laws not possible or just their “protectiveness” that prevents me from going 100% stock for the next 35 years?

Hmm yes the swisscanto seems to be worth a look. its funny i plan on switching my non-3a Depot from a MSCI World, Europe and EM to a simple Vanguard All-world lazy style Portfolio.

If the High Dividend ETF would be available this would be awsome. no dividend taxes is very mustachian indeed… althought since you can’t take out the dividends from your 3a and you have to pay taxes at the end of your saving period on the total, a dividend strategy seems only to be better if you can outperform a blend strategy? so in 3a the overall performance matters not the relation between capital gain and dividends, right?

About the hedge. Yeah i would never buy a hegde in my non-3a Depot but since the restriction of 27% for foreign currency will stay its a matter of second best solution.

real estate vs. cash. hmm as i will keep my low risk portfolio part in cash the only thing that bothers me is that you pay 0.68% also for the liquidity. which means there is no zero interest rate but a negative one on my cash at VZ-Depot. the price to pay for the tax cut. To your question why we cant invest 100% in stocks. well it’s not in the law itself (BVG) but in a regulation (BVV2) and yes it should protect you from taking to much risk but in my opinion this only leads to unattractive products. the majority of 3a-money in switzerland lies on accounts also because products are so expensive and somewhat constrained. most people use it to tax-efficiently save money to buy real estate. for investing it is still not very attractive. hopefully robo-advisory will change that soon. i mean 0.68% to give me some narrow and mostly mediocre ETF selection (like to know if there are some kind of kick-backs or retributions to VZ from iShares et al.) and teach the system some investment constraints? really? well we don’t live in the best of worlds but VZ seems closest for now.

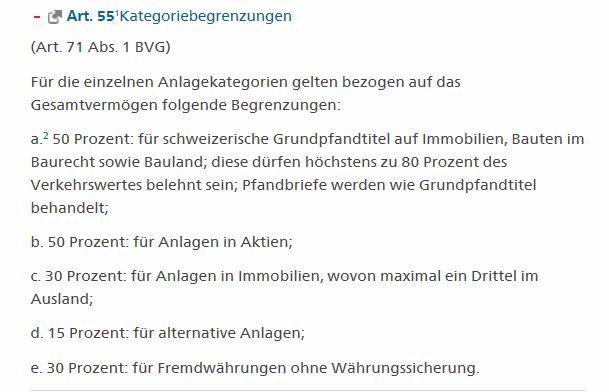

Addition to BVV2. in the regulation there is a 50% stock constrain but also an exception rule. if the pension institution takes on some safety measures it is allowed to go above 50% stocks. don’t ask me that kind of measures this is but since raiffeisen and postfinance have 3a index funds with 66-70% stocks (alot of smi) and UBS has its active 75% stock (world or swiss Focus with ter 1.75, haha) it seems to be really depending on the pension Institution itself on how much stock the can go. VZ could go up to 85% in stocks when you look at the Investment guidline document. but it seems they choose a 5% security-margin.

My decision was already made and I changed my 3rd pillar to the Swisscanto LLP 3 Index 45 R at LUKB a few month ago. I’m not really happy because of the timing and situation at the bond market after a 35 year bull market. But I think it’s better than a non compounding 3rd pillar. Until now I also had no bonds in my portfolio.

But for us as clever mustachians there should be more than one 3rd pillar account. So I consider to start the next 3rd pillar account at VZ to play more offense. I hope until than (2018) there is a decline in costs at VZ. They are really high at the moment.

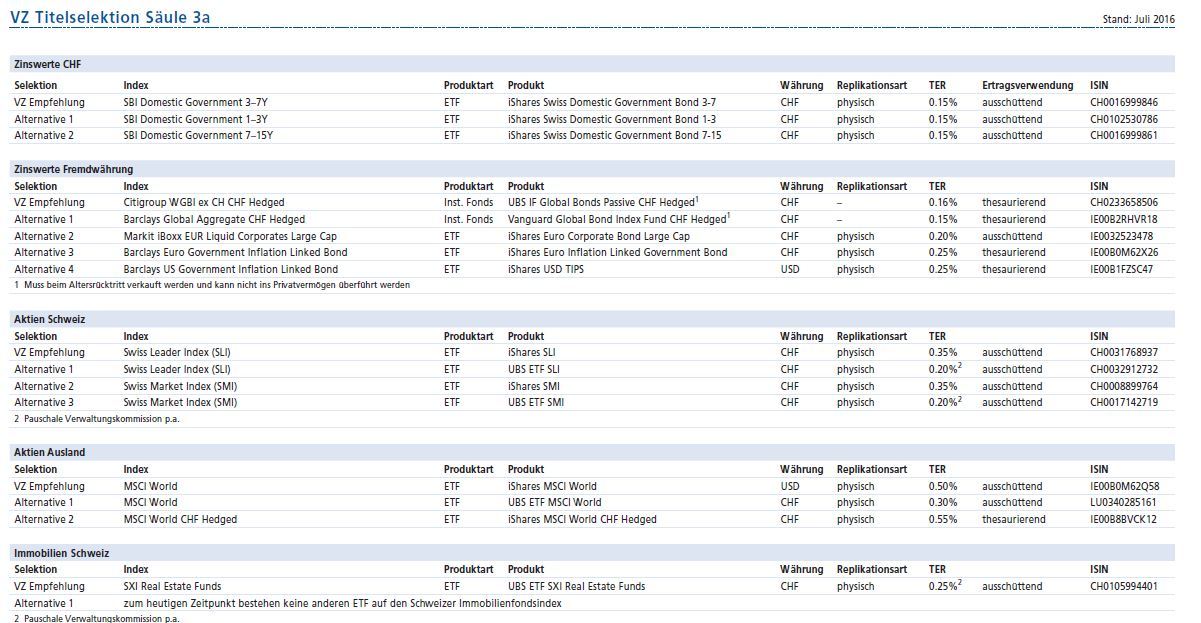

SPI Extra Indexfund

MSCI World ex Switzerland Small Cap Indexfund

FTSE All-World High Dividend Yield

where the two first are not available to me as private investor outside of 3a. yummy! and high yield could make sense since the 3a-dividends are not taxed, but i have to run numbers here. I have to design my new portfolio now!

yes definitely and that High yield and EM bonds are available gives me some fixed income alternatives to cash… (not in the AAA section of course

they even have factor etf von the SPI although if you look at the index they pic 30 out of the 60 biggest SPI components (so the better 50%) for 7 risk factors. well as i think this is way to weak to really get the factor right it is funny that they also try to the get small cap premium with this i mean take the better 50% out of blue chips to proxy small cap come on this is funny

but all in all thanks to vz a real improvement i think

Yeah, and reading through the prospects and seeing that there are still other unclear fees that add on to the 0.68% make me very wary of investing in a product like this.

So I am with them for over a year now. up to now i did not find any fees apart from the 0.68. however, if the fees are “hidden” i might have a hard time to find them. any suggestions where to look for?

Les frais de gestion de fortune (investissement

a lieu chaque mois), de tenue de dépôt et de

gestion de la fondation s’élèvent à 0,68 % (Allin-Fee).

Les droits de timbres fédéraux et les taxes

boursières ainsi que d’éventuelles commissions

de souscription ou de rachat pour les placements

collectifs ne sont pas inclus dans les frais susmentionnés.

and

La banque de dépôt imputera directement au preneur

de prévoyance les frais de gestion de fortune

et de tenue du dépôt. Une partie des ces frais est

soumise à la TVA.

also

Frais débités par des instances externes en lien

avec un mandat conclu par le preneur de pré-

voyance lui sont répercutés.

and

Une taxe d’au minimum 10 CHF est prélevée

chaque trimestre.

I’ve heard some rumours that the Fremdwaehrungsanteil restriction of 27% applies to all foreign stocks, i.e. you cannot go balls deep into S&P, but forced to buy swiss stocks or silly hedging. Can anyone confirm?

Also is 0.68% fee charged just on the stocks, or the cash balance too?

@pombeirp: I red the prospect too, federal stamp fees is not included but i can understand why. these are fixed fees that cannot be changed by vz via contractdeal so yes “all-in” is like allmost everywhere not all-in indeed. also the creation and redeption fees of the institutional funds are not included but are in the range of <0.1% (as far as i know these CS, Swisscanto funds) the minium of 10.- per trimester is just e barrier to really little accounts. your second insert to me is just means that the depotbank collect your fees (not the vz 3a pensiontrust). i didnt find any other document which would say you would have to pay additional depotfees. your third insert is for the case you want to use your 3a depot as a security to buy real estate. for that paperwork they charge you extra - which is i would say the standard in the industry.

@hedgehog: yes it applies also to stocks thats why they offer these index chf hedged funds like the one for msci world ex ch. but because in 3a they use the institutional share of these funds costs are quite ok for the hedges. the world ex ch has a TER of 0.18% which is even lower than the ordinary world etf by db x-tracker (0.19%) what kind of leaves me dissappointed is that vz doesnt use these institutional shares of index funds in its normal robo advisor (the one with 0.55% fee) there they us the retail investor shares with much worse costs which everyday joe can buy. why they give away this advantage is a miracle to me.

yes cash balances pay also all-in fees… thats why i use a normal 3a account at my housebank to park the cash-part. this is very unpleasant coz cash at vz would cost me about 1.2% (0.68%+~0.5% median 3a interestrate)

I just got online access to my VZ depot - which is up to now running on the passive 45 mode.

Here is the CSV export of all transactions since 2017. It seems like the individual fees are nothing but the stamp tax which is 0.075% or 0.15%. I don’t know why the numerical values deviate.

on 31.1. the remainder of my cancelled lifee insurence came in - hence the following purchases. It says “last rebalancing 31.1.2017”

I also don’t know about the following purchases & sells, I will try to find out about their rebalaning policies.

I will post any other insights i might gain

[edit] i tracked all transactions back to 2015 when i opened the account. There are actually no “sells” apart from those in the list above - no back and forth with my funds, yey! makes me wonder why CHF 5000 were shifted from stocks to bonds… and ahhh, i have to sort it out in a quiet hour

but overall, i think it’s not bad at all for a passive investment!

@hedgehog to be precise: 0.075% are for Swiss based securites and 0.15% for foreign based.

For exemple, VFEM from Vanguard is traded on SIX, but based in Ireland. On this ETF 0.15% stamp tax is applied

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

so i have to wait until releasedate.

so i have to wait until releasedate.

i mean take the better 50% out of blue chips to proxy small cap come on this is funny

i mean take the better 50% out of blue chips to proxy small cap come on this is funny