Perhaps people from developed countries invest locally. As a Greek I wouldn’t drop a cent on a Greek company, even though the Athens index has done spectacularly well the last few years. I have an Indian friend who’s on the same wavelength, “not a cent for Indians” he says. Anecdotes, sure, but they may have some weight to them.

Bogle cautioned against stock options too, saying something along the lines of “if you lose your job or the company goes bust you lose both your income and retirement”. Bogle indeed didn’t invest internationally, but the logic behind was quite poor (“Britain has weird politics, French are lazy, Japanese are old, US companies do business abroad so it’s all fine”), backtesting shows he would have gained from investing internationally but nevermind, we owe him making investing accessible and cheap.

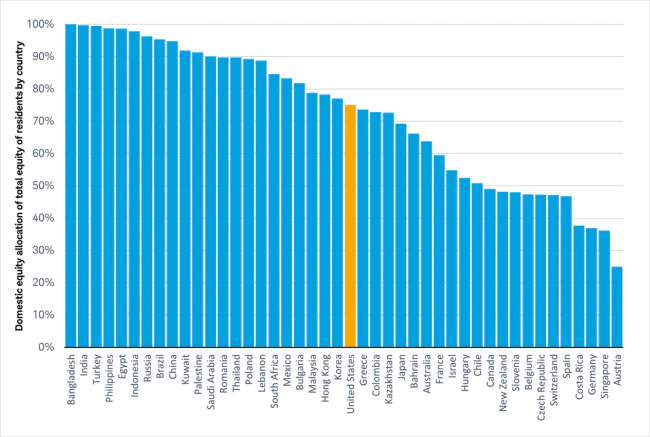

Just to be clear. Home bias is normally referred to Country of residence. Not necessarily Native country.Your Indian friend is out of India, so his view is not representative of resident Indians do. See chart below. By the way, my greek friends say the same (what you say)

I am not arguing if Bogle was right or wrong. In the end it does not matter because investing is not only about returns, it is also about peace of mind.

Agree, that’s what I meant indeed. Interesting graph, by the way, I’d anticipate it has to do with availability/ease of access/restrictions to investing/taxes that lead to places having so high domestic equity investing. I think I’d read that Turkey, for example, has very preferential treatment of local equity investing.

Edit: re Greece, many people got burnt in the stock market bubble of late 90s-early 2000s, in fact probably anyone investing from 1998-2006 are unlikely to ever get their money back in their lifetime. Predatory “advisors”, legal insider trading, every trick in the book was utilized that few made a killing and many lost A LOT.

I was always under the impression that I own an equal fraction of all companies through my ownership of VT, i.e. each share of VT represents ownership of 0.00000001% (or whatever) of each company in the index it tracks.

But thinking more about it, this couldn’t work in the extreme case if there is some company in the index which has a small free float, i.e. if VT as a whole has enough assets to own 10% of each company, but some company only has a free float of 9%, that’s not possible.

Now the next questions:

How is free float actually defined and determined? I guess it must be public information for the index funds to know how many shares they should own.

what mechanism exists to stop the Hermes family declaring their ownership to be part of the free float, yet still maintaining ownership of that stake (which would boost the amount the index funds should own and therefore would increase demand for the shares)?

Insiders always need to declare their buy and sell of stake. There are even rules around how much free float is required to be even part of publicly listed indexes. But I don’t know the details. You might need to look into individual indexes to check for information.

For Hermes family this is even more complex because they are under constant attack by LVMH to buy them out. Thus Hermes formed a company called H51 which holds family shares and they cannot sell without internal agreement.

I found this article from Morningstar with summary of expected returns for stocks from US vs International stocks and also bonds. This is in USD terms. CHF terms would be less.

Hopefully it helps in defining some expectations. Of course it is only forecast. This was at beginning of year so the recent performance would actually reduce further the expectations.

Was scrolling this thread and came across this statement.

It is a common misconception that Fama and French got a Nobel for factor work (value is one of the factors). French did not get a Nobel, Fama got a Nobel for his work on the efficient market hypothesis, which is not related to their seminal work on the cross section of stock returns.

French is heavily involved with Dimensional Fund Advisors, the firm that commercialized factor funds.

It is hotly debated if the factors may provide better returns.

It’s a little orthogonal to the topic, but I find it interesting nonetheless.

I know, others disagree and offer as a counter-argument – with almost (at least seemingly) stifling intention from the tone that I pick up – hand-waving Fama’s Nobel prize* through the air, @Compounding’s statement still resonates with me.** If I had to super charge it, I’d phrase it as “Value is a marketing term, just like saying Growth instead of Magnificient Seven. And the goalposts keep changing all the time.”

It also reminds me of

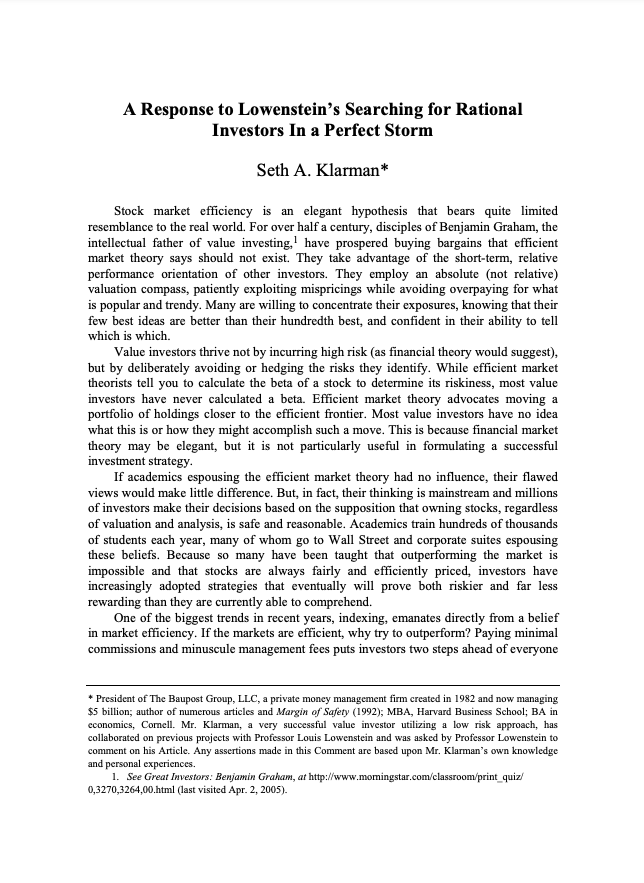

an article by Seth Klarman that I came across recently.***

Favorite quote is the first sentence: “Stock market efficiency is an elegant hypothesis that bears quite limited resemblance to the real world.”

Chuck Carnevale, aka Mr. Valuation, and one of my favorite quotes by him: “Growth and Value are twins joined by the hip”. He’s expressing that you can’t throw stocks and sectors into category “growth” or “value” by their name, but that valuation is what matters, regardless of what the artificial category that “the market” and the press slaps onto those things.

At any rate, feel free to disagree, please remain civil to each other.

If my twist to this topic was already discussed extensively elsewhere, please forgive, point me to it, and I’ll take appropriate action here to this post.

* Note that in the same year – 2013 – Fama was awarded the prize for what is now being summarized as the Efficiend Market Hypothesis (EMH), Robert Shiller was awarded for what is summarized as “behavioral economics”.

I remember, at the time I was very new to investing, plotting out how to set up a 60/40 portfolio and being interested in economics, and being puzzled seeing the Nobel prize being awarded to what I at the time perceived as two opposing theories about investing.

For completeness: a 3rd guy got awarded, too, but I’m not familiar with his thinking.

The 2013 Nobel prize press release for those interested.

** I would also gently remind all my friends with strong beliefs in the theory of an efficient market that economics or finance is a social science. Not to belittle it, but it’s not a hard science.

Which is kind of why you ideally title your efficient market thoughts as a hypothesis (because you can’t really prove it and things will change in the future) versus calling it a law, as you would maybe in Physics, once theories are accepted as proven, like Newton’s law of gravitation.

Isn’t that what makes it interesting? Anybody and her mother can solve some formulas and has science to do, but once behavior comes into play, it gets complex.

That‘s like saying someone outperformed me trying to climb the corporate ladder, because they played the lottery once and won the jackpot.

In the end everything is a game of chance, and one does try to tilt the numbers in one‘s favour. Doesn‘t mean others can‘t get lucky with way less favourbale nunbers for them and I can get unlucky even with 99% success chance.

And it surely is not wise to try the way with less chance.

E:Although active day trading is of course also not advised and statistics also show that they underperform the market. So both are kind of bad examples. Akthough if the first case is a quantinvestor, then it‘s different again.

I don’t get this analogy, but admittedly I’m also on the dudes sides of the spectrum nowadays.

Are you saying that the dudes who bought DPZ, HD and GOOG played the lottery?

Genuinely confused, and apologies if you were referring to something completely different.

Here I would fully agree with your statement as is.

I think where we differ is that I believe “chance” cannot be as sharply calculated as I think you think. I believe there usually is no such thing as “99% success chance” in the world of finance.* This certainty of a probability exists only theoretically and only in hindsight practically.

* To flesh things out a bit more: Economic theories may suggest such exact, or mostly exact, probabilities exist based on applying some stochastical models onto sparse historic price data. IMNSHO this is just social scientists forcing their hammer – statistics 101 – onto a limited data set (historical price points with a rather limited amount of historical data), throwing in a bunch of assumtions so things can actually be calculated – like using volatiliy as a measure of risk – , and then drawing conclusions.

At least the conclusions are usually presented as theories.

Picking any single stock and putting most of your imvestments in that is akin to playing the lottery. Yes the chances are way better than actual lottery, but you are still placing a bet on that single firm outperforming or not going bust. It‘s huge idiosyncratix risk.

ANY company can go bust or be broken up or have a huge scandal that tanks them.

If I came across as propagating picking any single company and putting most of your investments in that company then I would like to clarify: that is not at all what I am suggesting.

All I am saying that I don’t believe in general in the principles … ahem, theorized about by the Modern Portolio Theory (MPT), which includes the hypothesis of efficient markets, using volatility as the measure of risk, etc etc.

There’s still thoughts within MPT which seem true and even intuitive to me, regardless of behavioral economics, like diversification of assets — reduces the risk, reduces the return.

Still doesn’t mean I have to believe in the entire theory …

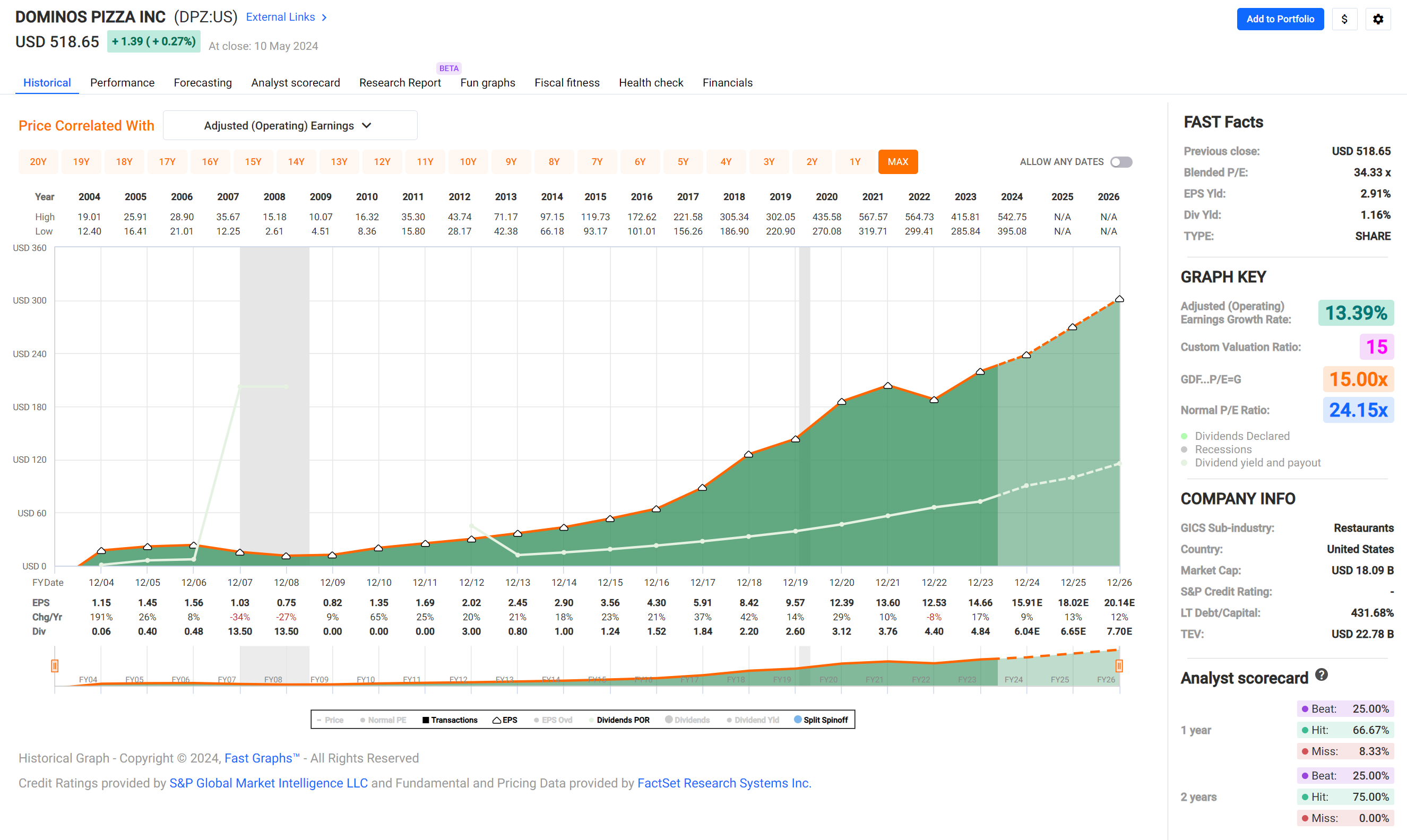

DPZ, HD, GOOGL: I am not invested in any of these companies – mainly for valuation reasons (which you might call market timing reasons) – but I would claim that the dudes mentioned above having bought and buying Domino’s Pizza, Home Depot, Google will likely do well.

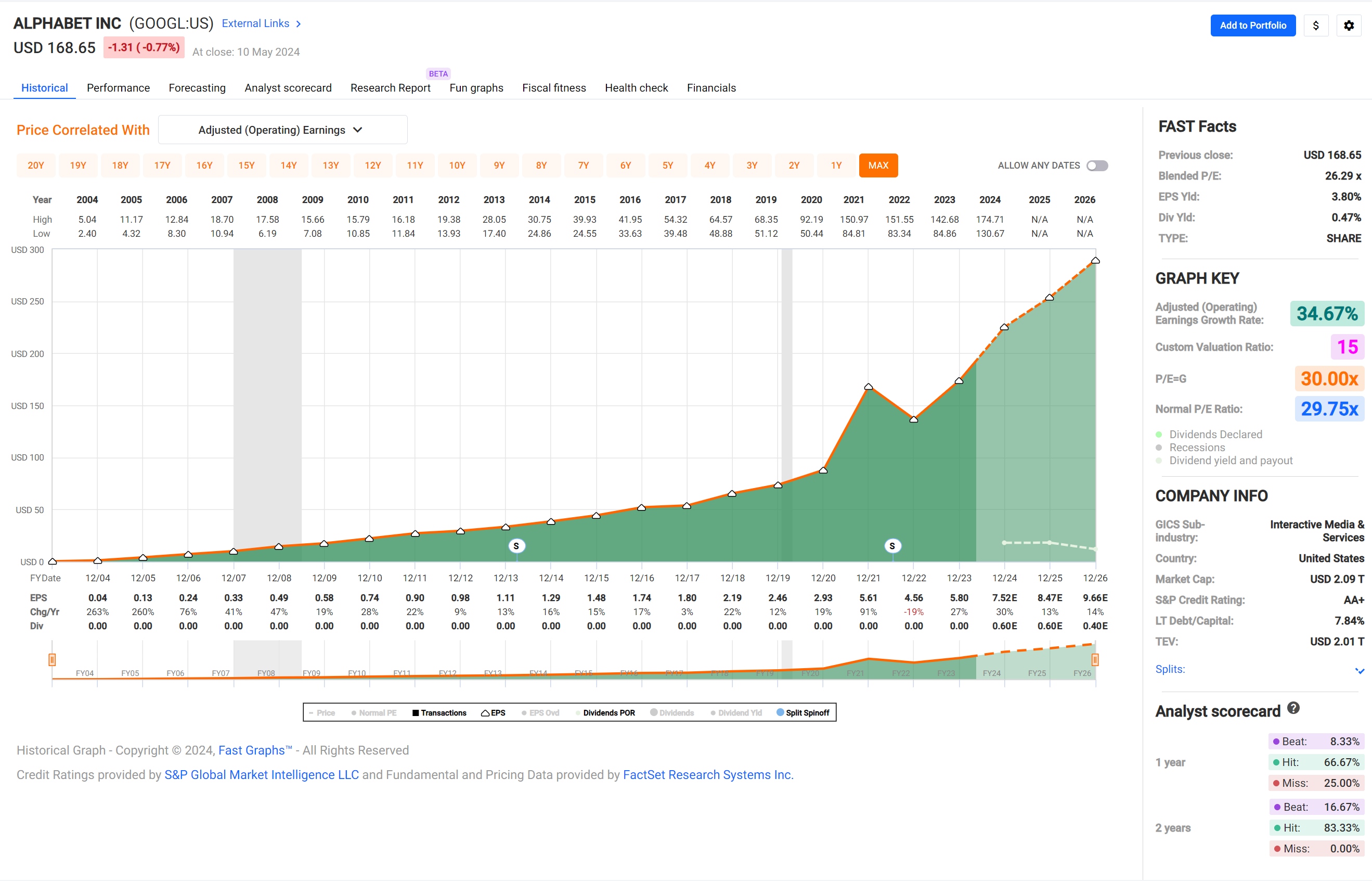

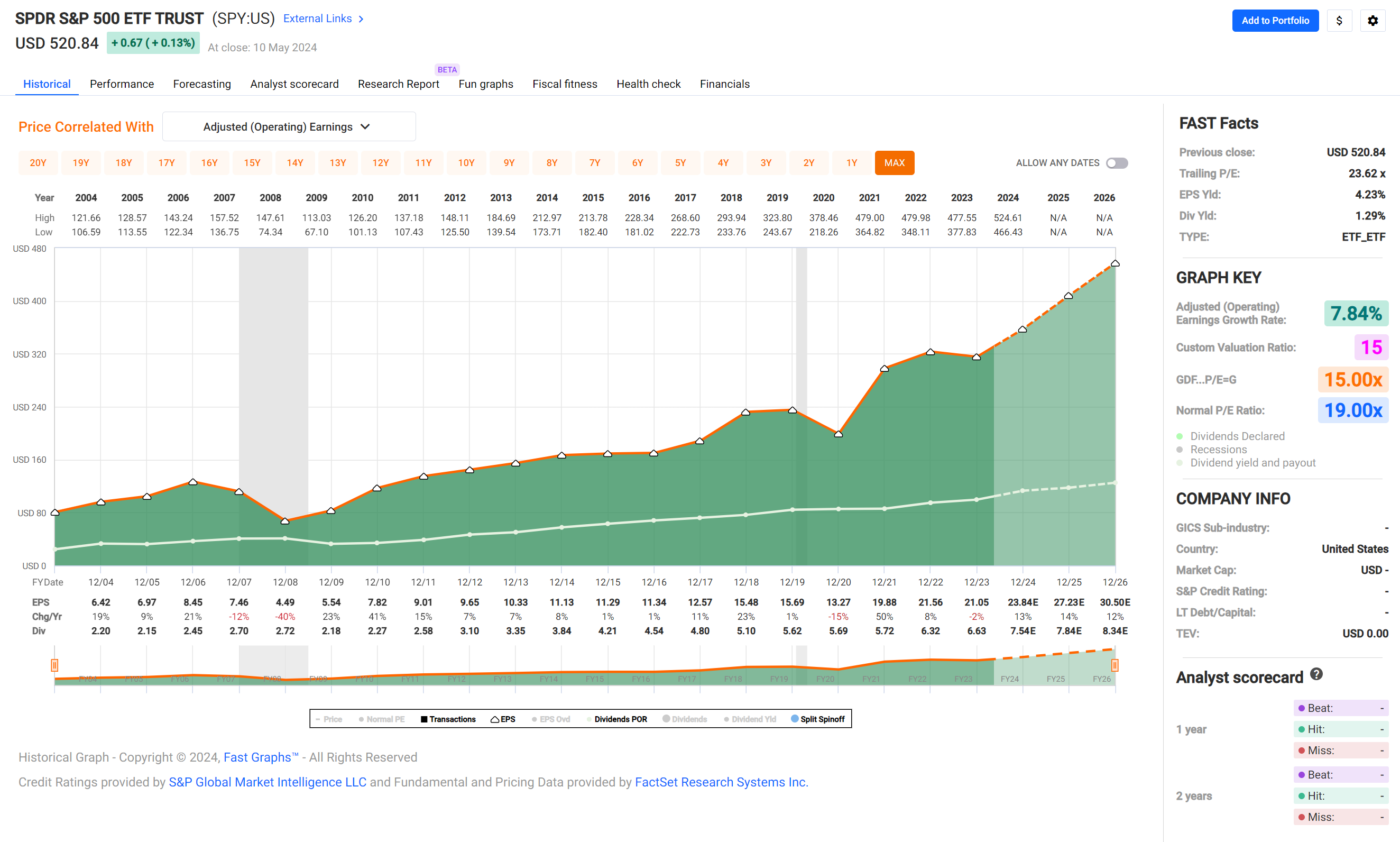

Here’s graphs on operating earnings for the three companies. I’m deliberately leaving out price. The point is: these are companies with several decades of growing their business while growing earnings very consistently.

In my opinion, there is nothing wrong in picking individual stocks and building a portfolio. It should not be considered gambling unless someone just bought stocks based on some random YouTube suggestion. If one has time, acumen and interest, then it can be a good investment plan to study various companies and investing in them. This is what used to happen for many many years before the index investing became fashionable.

It’s just that active portfolio selection has a low chance of beating the market over a long term. If this is not an issue for the person, then it should be fine.

While I’m a proponent of investing in individual stocks, I like to remind myself that single companies can go bankrupt and that heavy concentration risk may not necessarily be worth it (that is, I need to diversify at least a bit and be willing to loose any single of my investments, and potentially a bunch of them altogether, at any time).

We are not Warren Buffets with direct access to the company executives, accurately assessing the health of the business is pretty hard at our level and with the information at our disposal. We can have a pretty good idea of it if we are willing to dedicate the time and energy for it but I wouldn’t throw my full confidence behind any of my stock picks.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.