Im tilting value and keeping US/ex-US at 50/50. that should fare well in any market environment

Also thumbs up for Ben Felix

If you want a simple two fund solution that tilts to factors and especially small value (it‘s about 25% small for the core 2 etfs) and is still reasonably priced:

50% DFAC - dimensional fund advisors (Avantis was founded by expats from there) US core 2 etf

50% DFAX - international ex-us core 2 etf

Or do it market cap weighted 60/40, however you see fit.

Sure, they are. But doing it now, because of fear of what might happen is not reasonable. Who knows, maybe the bull run will continue for another 20 years, maybe there’s the biggest crash in history tomorrow…

First, my US allocation is maybe 30% overall.

Second, I don’t give a flying f*** about any predictions, no matter from whom. No one can predict what the market will do.

Third, if there’s a crash, perfect for me, I can buy cheap during my accumulation phase

It‘s not a prediction. You should really watch it (it‘s just 7 minutes cmon) or else any discussion is moot.

Again watch the video.

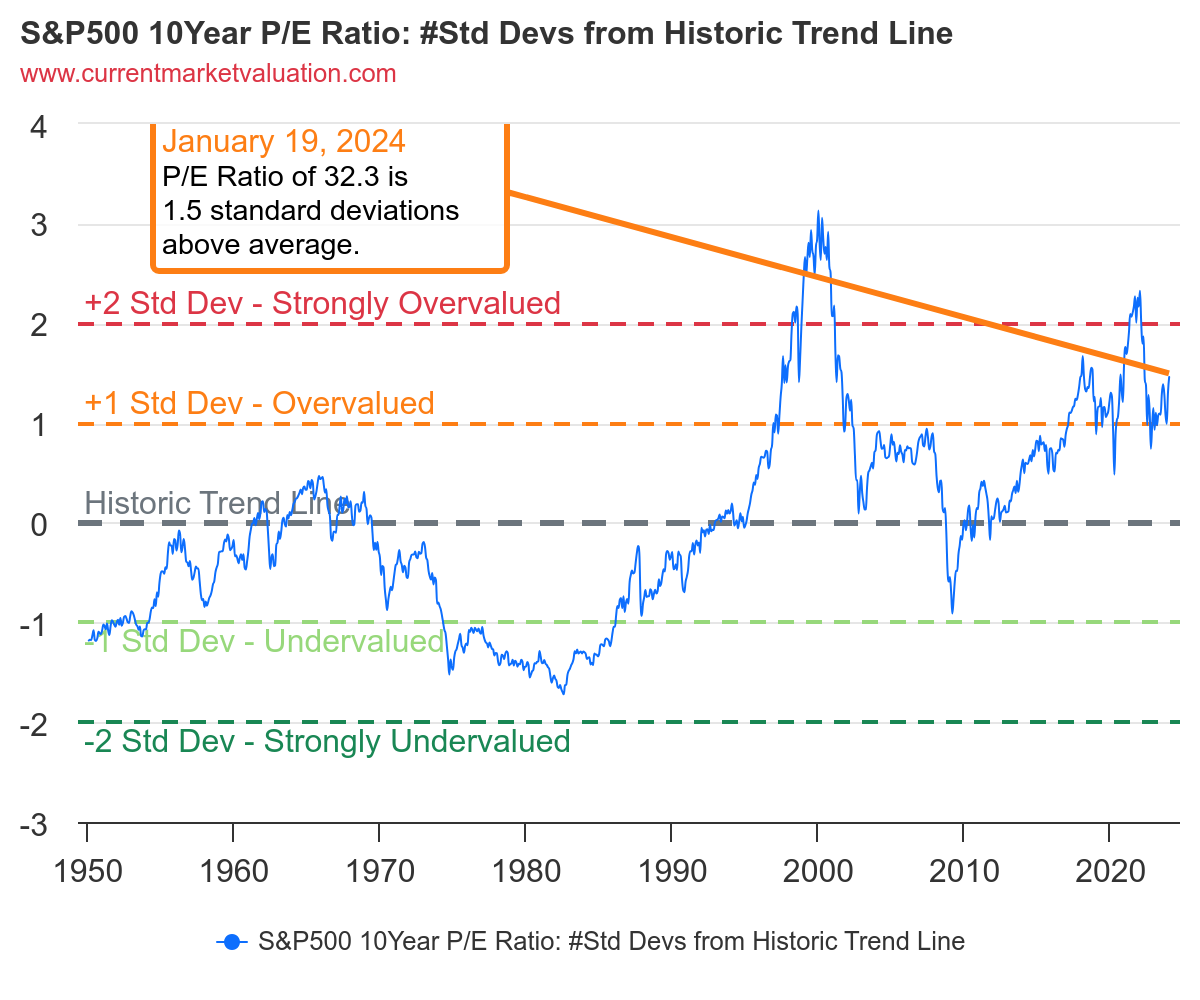

A bull run for 20 years at these US valuations is literally impossible.

Also changing your allocation because of new information and you thinking this through (this is what OP is doing here) is totally reasonable. There is strong arguments for tilting a bit away from the US. Which you also apoarently do.

Having a general value tilt is also a good idea in my opinion and being internationally diversified anyway (VT already is of course).

Sure, but a decade of underperformance like starting in 2000 is also not that great for accumulation.

Although this is not that applicable here and more geared towards those having overweight in US

Well high valuations → Low expected returns (with some noise)

I guess we all care about our returns. No?

That’s actually a very good argument and a well established strategy.

Not if you invest lamp-sum before the crash and you do not have 30 years horizon

Well, factor tilt is not an arbitrary, out of the blue, strategy. There are good arguments in favor. But ok, I am not either 100% convinced it will work for me…

Same with home bias…

Ok, I watched the video and he even states himself that the US is not overvalued, but some large cap US stocks are overvalued.

In markets and in life, impossible things happen all the time.

I’m more for buying good companies, value stocks (true value stocks as defined by Benjamin Graham) are very hard to almost impossible to find nowadays, Berkshire also changed its direction from value stocks to buying good companies based on Charlie’s advice.

There’s always new information availablie and if you change your allocation all the time, it will have negative impact on your performance as your always changing the latest trend and information. Make a reasonable strategy and stick to it.

i guess the problem is that you could say various stocks have been over-valued for the last 10 years or so and you could have missed out on 10 years of fantastic gains.

or you could take a value approach and buy value stocks and forgo those big gains to avoid the potential later falls.

or some mix in between where you have some allocation to each bucket and re-balance periodically.

Interesting.

Does 10% make much difference though?

Even after rebalancing you would still have a very high % of your assets in high valuation stocks (~55% vs 60% in case of 100% VT)

But ok, someone could have lower % allocated to stocks.

The question would be then: diversify with what?

If we are talking about bonds, I am not sure if it makes sense for a Swiss investor (taxed on marginal rate). + 2nd pillar is kind of a forced bond.

Gold, Crypto etc do not make sense to me. Maybe REITs? Not sure about that either…

The thing is that Cap weighted US stocks in a regular ETF (e.g. VTI) as a whole were not overvalued 10 years ago. At least not so much.

It wouldn’t make sense to differentiate from the market back then. At least not due to the valuations.

That’s one idea (option 3 in the initial post) to lower your exposure to super high valuation stocks.

I will add “equal weighted” ETFs on US stocks market as an option.

I was actually thinking about switching to equal weighted allocation, at least for such extreme cases as US and CH markets, if I ever going to live off my stocks portfolio. In the accumulation phase that I am in now, I prefer to stick with market capitalization weighted portfolio. The drawdowns might be stronger, but there seems to be more growth chances AND I can wait.

The problem if you use a rough measure like P/E to define over-valued and “tilt” accordingly (or even worse Price to Book like the guy in the video, Ben, uses) you not only filter out “Non-profitable & speculative tech” but you also filter out profitable and growing companies like Microsoft

If one doesn’t think that’s a bad idea refer to the famous Charlie Munger quote about Return on Capital

Exactly, perhaps it’s naive mental accounting on my part, but I tend to think like “Starting from 10, climbing up to 50, a 20% or even 50% drop will leave me with 40, or even 25, which is better than starting from 10, climbing to 20, where a 10% drop will leave me with 18”. If this childish mental accounting makes any sense

Value has taken a huge hit vs growth the last ~15 years though, eventually will turn, the question is whether at that point a huge amount of gains will be irretrievably lost. I personally find some more comfort emotionally of spreading eggs in many baskets, with the biggest one (50% of portfolio) being world market cap weight, then quality, some value, some tech, some indexy stocks like BRK, some no brainers like nVidia, Lilly, Novo etc. In the end time in the market is key, and not investing is far worse than investing, so we’ll all be fine!

DIY US Investors are the strongest Private investors in shares Globally: There are not many economies that both generated signifficant investable income and a need to privately invest like in the states

DIY US Investors exhibit a strong Home Country Bias: Same applies to most Private Investors globaly, Home Country Bias tends to reduce as Wealth is Managed (HNWI) and Institutional Investors tend to no longer exhibit it

DYI US Investors drove US Share Prices up: its only a few Billion probably but still VTSAX only investors leave a small mark in Valuations

Non-US DYI Investors couldnt offset this: see point 1, there is simply less DIY Investment Savings available elsewhere

Inst/HNWI/Managed Investors didn’t offset this: as they follow somewhat static, globally diversified Asset Allocations. In the bigger scheme, there are not many large, international investors with game changing home bias / US exclusions

Trens Followers increased the Trend: it takes a few percentage point overperformance only and even more money poured into the US, turning this into a self-fulfilling prophecy until this day when more and more even non-US DIYers go US only

Asuming that this is what happened (I don‘t have data yet a clear instinct) we currently face the following situation:

US is in a valuation Bubble

Short Sellers don‘t (yet) cover it as its too risky to go short against a Index trend; Short Sellers accelerate a trend reversal and process it. Short against a trend only works if you as a short seller had clear data that makes you assume your targe wen buts in a limited time; so won‘t happen against indexes.

Conclusion: Efficient Market Theory doesnt apply here. We sit on a time bomb that goes belly up if anything changes in the US, like DYI investors turning to cash withdrawers. The first tiny signal of this happen will wake up Short Sellers and THEN will EMT put the Us Stock exchanges back to where they belong.

Interesting thought process, I have had similar thoughts many times, however how do you account for literally all big US asset managers recommending 30-40% ex-US? Wouldn’t this have an impact?

We’re a minority here (and in the US) who take a very keen interest in “the whole investing thing”, enough to read and write about it in public fora.

In the US in 2022 the headlines were that nearly 50% of households have no retirement account whatsoever. Sure, with wealth inequality of the US this may mean they represent people who have no retirement accounts because they live breadcrumb to breadcrumb so they wouldn’t move the needle anyway. I don’t know. I have also had the opposite thought and wondered if European valuations would be even lower if it wasn’t for European pension funds taking small, but not insignificant positions in home equity.

It makes more sense to me logically that Joe Schmoe from 'bama walks into their local Vanguard/Fidelity/Schwab/Edward Jones office and asks to plan for his pension, gets put in a Target Date Fund with automatic contributions and rides happily into the sunset.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.