Hello guys,

in the past days I have seen that a new proposal of low-cost third pillar has been made from UBS.

In detail, finally, also UBS decided to provided Passive investment strategies. Here the link of the most extreme product, with 100% stocks. on the contrary I have seen they offer a series of funds, very similar to the various Fintech companies (VIAC, Finpension,…).

If what I see there is confirmed, it seems now to be very competitive against the above mentioned Fintech companies. 0.25%+0.18%=0.43%.

Just as a reference, VIAC is now the Global 100 at 0.45%.

If confirmed, this may be very positive news for us (the customer), yet quite challenging for the various fintech. any comment?

Do you expect also Credit Suisse to follow? Now CS is providing some passive fund (up to 75%), but costs are still on the order of 1%.

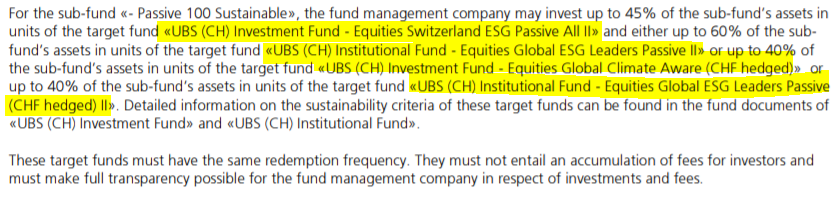

thanks Wolverine. very clear. can you please attach here the fachsheet you mention?

Then, you guys all conclude that for the moment the old fashion banks are still faraway from the fintech? Do you forecast any change in the near future?

Yes, or Vitainvest 100 Passive (0.90% total TER, btw newly available since this summer) for that matter. Lets say you are able to save 20k/year and need to amortisize 6.8k/year. Now you have to options:

A) Direct amortization. Save 0.60-0.90%/year on interest (or less after taxes) and invest 6.8k/year in Viac/Finpension and 6.4k/year IBKR.

B) Indirect amortitation. Invest 6.8k/year in the banks 3a investment solution and 13.2k/year in IBKR.

While the banks 3a will have a higher TER (0.90% compared to 0.45%), you’ll end up with more money when chosing B.

That PDF is the marking brochure for their retail 3rd pillar offering. As part of the pension scheme, the pension foundation can give you access to these restricted classes, same as VIAC does.

I mean, these finds came into question as a way to invest 3a money used as an indirect mortgage amortization at UBS. I don’t think one can buy funds for qualified investors in this setup. So you are stuck with World 100 U.

These investments are not limited to qualified investors. They limited their offer to a class Q for internal reasons. They are without retrocessions. There is a 2% load fees which is waved when invested through 2nd or 3rd pillar.

I haven’t looked into the 4 UBS sub-funds. Overall, the product seems cost efficient and simple in its design.

I’m happy to see that the big banks start offering cheap 3A passive solutions. Competition will increase between providers leading to better cost efficient products for investors (at least I hope so).

Is it your understanding that we can buy these in UBS’ custody account - 3 pillar? If the 0.25% fee is accurate it would be cheaper than VIAC or Finpension

Why do you think of the contrary ? because of the “Q” in the name ? it’s a share class. They could have opted for “X” or “Z”.

As shown by Ed_waadt in the all public marketing brochure, there is only one share class.

It wouldn’t make any sense to limit a 3A passive solution to Qualified investors only (> 2 mio CHF). With 2 millions of wealth (direct investments in real estate and claims from social insurances (including claims from the 2. and 3. Pillar are not considered), the 3A would be the least of my concern.

Based on UBS website and documentation, I do. However, these products were issued one month ago in the middle of the summer and are not highly advertised by UBS. They make more money with their active funds

I’m not surprised if they are not yet well known by UBS advisors.

You can’t buy them in normal custody accounts, they are for 2nd/3rd pillar only. Total TER will be 0.90%/year as there will be a custody fee of 0.65%/year when using this fund for 2nd/3rd pillar.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.