I see what you mean now. I was just hypothesizing for my situation, where in my mind income tax is already paid and doesn’t influence the amount invested.

I agree that the comparison is not 100% meaningful. But considering income taxes like you said, still makes 3a alot better no?

Precisely because of this, it makes the 3a better. In the open market, you can find a product that will be at least as good as the one in the pillar. The tax free advantage is what gives pillar 3a the edge. But @nugget mentioned there are some additional costs of the 3a pillar, which I would be happy to read about. Then we would have a full picture.

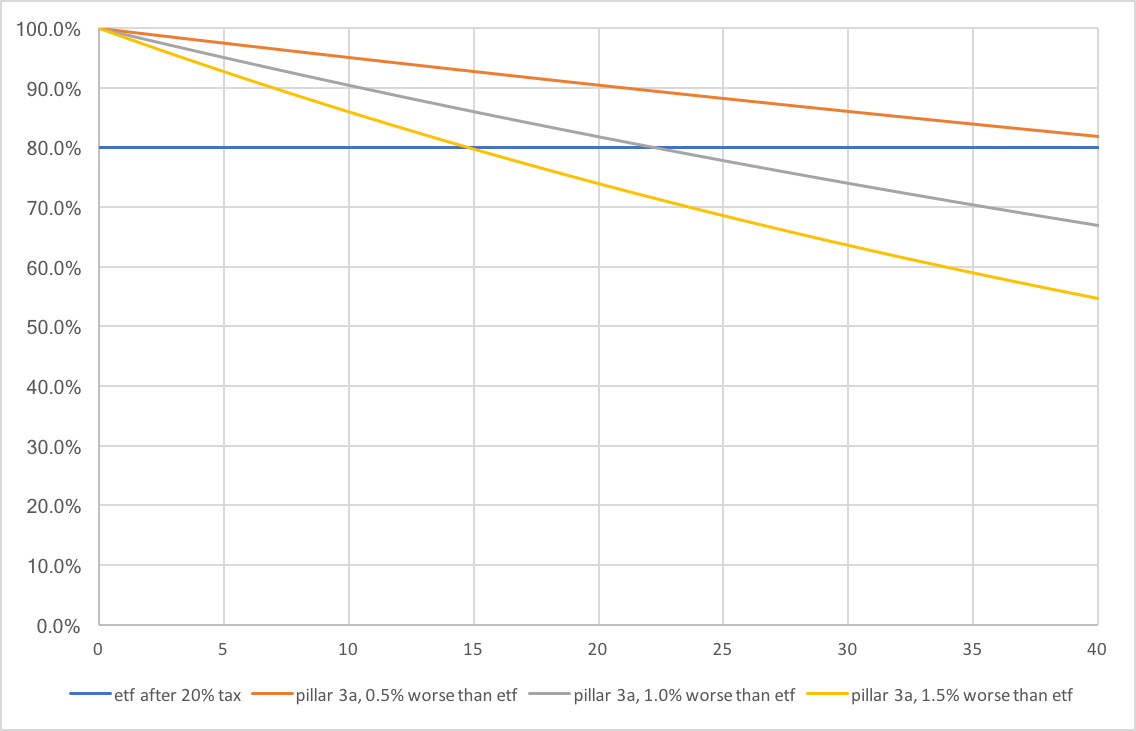

I made a simple chart which should illustrate it. The way to read it:

X axis: years

Y axis: the percentage of the initial investment, had it all been put in the ETF

“worse than ETF”: could be custody fee or just underperforming the ETF (per year)

you have to check which curve is higher on the expected year of withdrawal

it depends a lot on the cantons too. In my canton I am already paying 0.15% of wealth tax, which does not consider money in pillar 3a. Additionaly you save your income tax on the dividend (let’s say 25% of 3% of your global fund). That’s an additionaly 0.75% per year, so a total of 0.90% tax savings per year compared to the DIY solution.

And I agree it is important to include income tax in the contribution amout, ie 5000 diy vs 6768 3a solution.

how is this possible if the money in 3a costs you up to 0.8-1.0 % less per years in taxes?

With VIAC plan(97% stocks) I don’t think you can find DIY ETFs which can make up for the tax-sheltered benefits.

I’m also starting to think like this 3a is must have, regardless of the timeframe. The high fee of 0.5% is made up by the fact, that there is no income tax on dividends. Then let’s say that the less than optimal regional allocation of the fund (way too much Switzerland) costs 0.5% (but depending on situation, you may even match or outperform an open market ETF). So we have to look at the orange curve on my chart. with an income tax of 10%, the break even point is after 20 years, with 20% more than 40 years!

Anybody sees any holes in this logic? How big is the tax you pay when you pay out your pillar when leaving Switzerland? Can you leave the money in the pillar when you leave?

thanks Grog for being persistent, you might have contributed to me changing my attitude.

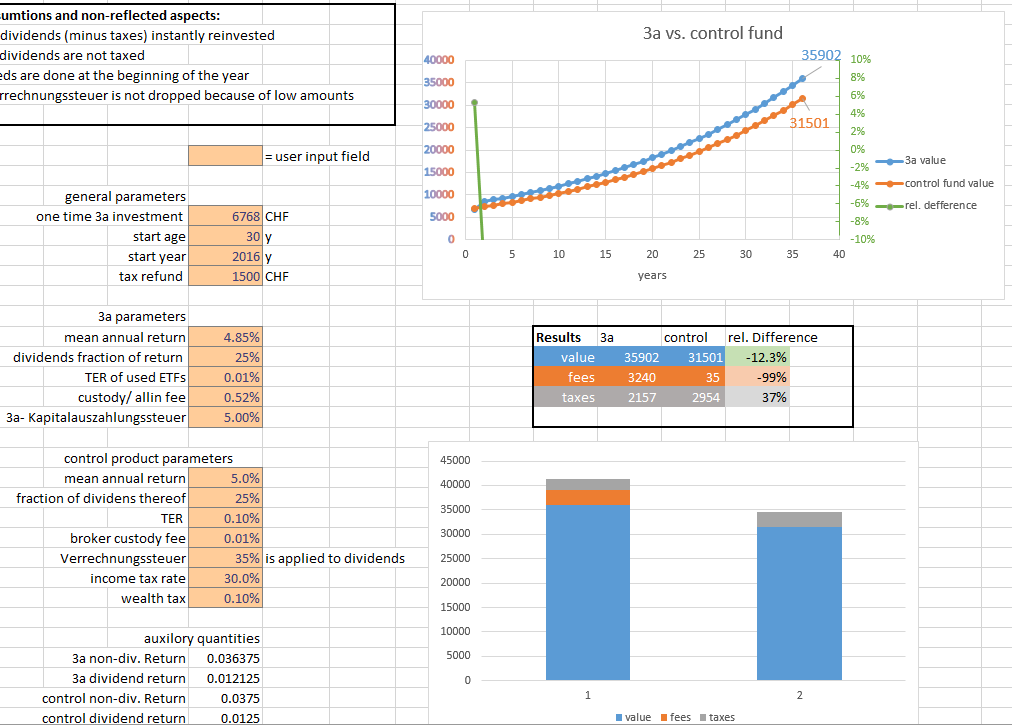

going back to my not that outdated calculator from the opening post (the one for a single year’s investment)

i find a more than 10% advantage for 3a. this includes taxed dividends, Kapitalauszugssteuer. the wealth tax might not kick in in this simulation.

parameters & assumptions in the image:

And i don’t think that 35 fees for the control fund are realiGuns, because 3a contains transaction fee. If you buy once per year even on IB it costs you 1-2 dollar of currency conversion and 3-4 dollar of transaction. At least i think.

I will ask for the third time: what is the tax you pay when you pay out 3a before you reach retirement age? In the calculator, I see “Kapitalauszahlungssteuer” 5%. I guess it depends on the total amount and canton?

And second question: How do you invest in this VIAC? You open a separate account there and once a year make a bank transfer? How reliable is this company? If they go bust, is there any risk? Is thi VIAC the best there is for 3a?

according to my valuation, their offer is closest to the low cost index fund investment popular among mustachians. VZ had a similar offer before, but with max. 80% stocks, lots of currency hedging, and a bit more expensive in fees. after that come the swisscanto passive funds. MP made a blogpost about it.

everything after that (UBS/CS funds, life insurances, cash depots) are somewhere between worthless, ripoff and scam. see this as bad example

haha yes, pillar 2 is regulated to the ground. no flexibility/ no reasonable investing with a 30y+ horizon. need to become self employed to avoid this over-subsidizing of the swiss over-paid retirees. just like in germany^^

(i have no grudge vs the retirees but the system was made in a way they recieve 25-30% more than is sustainable)

as self employed it is not mandatory to “be connectrd to a Pensionskasse” https://www.ahv-iv.ch/p/2.09.d

however, as i read, it becomes mandatory again once you employ people. complicated… maybe less straight forward than i thought. but this is stuff for a Pillar2 thread, not this one^^

Depends on where you’re leaving be careful not to get slapped with full income taxes by your new country of residence when you finally withdraw! I know IRS does this. Applies to pillar 2 as well

Get your facts checked, subsidizing old geezers is what state pensions do (pillar 1), not defined contributions sort of plans like pillar 2/3, these function much more like bank accounts, you get what you paid in

He said short term and i fully agree. If you have any sort of respectable salary worth talking about, ZH takes 40% of it in taxes (marginal rate). Shove this money into 3a for a few years, pay 5% instead of 40% on withdrawal and even if all the fund did was invest it into -0.75% yielding bonds you’d still walk away with a nice profit.

In the long term however it’d be much more important how the money is actually invested of course, stuck for 40 years in low return funds your opportunity costs will be enormous and not even close to being compensated by tax difference

i don’t think I am that far off. Umwandlungssatz is in free fall - and already/still people live on average a few years longer than their individual stash would allow in terms of the BVG annuity. Their life expectancy still rises faster than the pension systems adjust.

when i am retired according to BVG god knows what the umwandlungssatz is going to be. 3%,4%? already today it’s 20% less than 10 years ago. somebody pays the difference. “Bestandsgarantie” is the word => they cant change current expenses, only future expenses (my pension) and payments

yes exactly. but once we assume a stock portfolio like the VIAC 97%, it’s ot that clear anymore, no? still, it’d be stuck for the same 40 years. also there is the risk of change in legislation - imaginge they ban stocks from pillar 3a, then you have your stash rotting there. or decrease the tax benefit… whatever

And why should you care? Pensions are for poor people. There’s no need at all to wait for your pension fund to cough up your money bit by bit, you can take it all cash when you retire or leave the country and determine yourself how it’s invested

I do care since i am forced to put money in. Money that is being compounded at 1% in 2017 when the fund made 6+%. where do the 5% difference go? for sure not to my stache, but to pay oversized pensions. MSCI world made 22%. i believe you wouldn’t just shrug your shoulders on a 21% opportunity cost investment.

That’s why I don’t account 1st pillar in my net worth and FI calculations. I treat this money as “stolen” - maybe I’ll get back some in the future, maybe not. I don’t count on it though - especially with expending government expenditures and growing demographic problems to sustain them.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.