I would go further and say: You also have to be cautious what you publicly state.

If you are an ethically responsible entrepreneur or business, that is.

Especially when

a sizable part of your customer and shareholder consists of fanboys that often take your word at face value AND

when your public claims concern safety-relevant features of your products

That’s the issue at hand for me: We “know” that it’s not ready yet - but they are blurring the line if not outright suggesting it is. (I’m gonna stop here not to repeat myself any further).

And while I’m not sure your twittering TechnoTsar always knows what he’s tweeting (from a perspective of corporate governance - and the SEC’s), I’m not buying he doesn’t know what technological claim he’s making.

“I will not be surprised if European and Japanese authorities put a ban on its use. Even if it’s just to (secretly) protect their domestic automakers and allow them to catch up.”

But why ban outright, if you can influence public opinion?

Well, the ransomware business has been on the rise for a few years now, also not stopping from cutting of the IT infrastructure of hospitals (some people do not care about lives when it comes to money).

Tesla or other FSD car owners seem like a good target to me, especially with such cars being sold more and more.

And it does not need to be life threatening, maybe involuntary speed limiter to 15 within city limits or parking sensor signal jamming, causing lots of scratches and parking damage.

I definitely would not rule out, that this becomes popular.

I don’t know, I’m not informed well enough. But it’s kind of obvious that AI is capable enough in some areas, and in some not yet. AI can beat any human in chess, go and other games. Being able to drive in real life is a huge step and it will make a huge impact if it can be achieved. Progress is being made. If Tesla achieves it in 2025, I will still be impressed. The rate of improvement is so far satisfactory to me. I take the promises and claims quite lightly. Everybody can do with them what he wants.

I have read the earnings call from yesterday. Highlights:

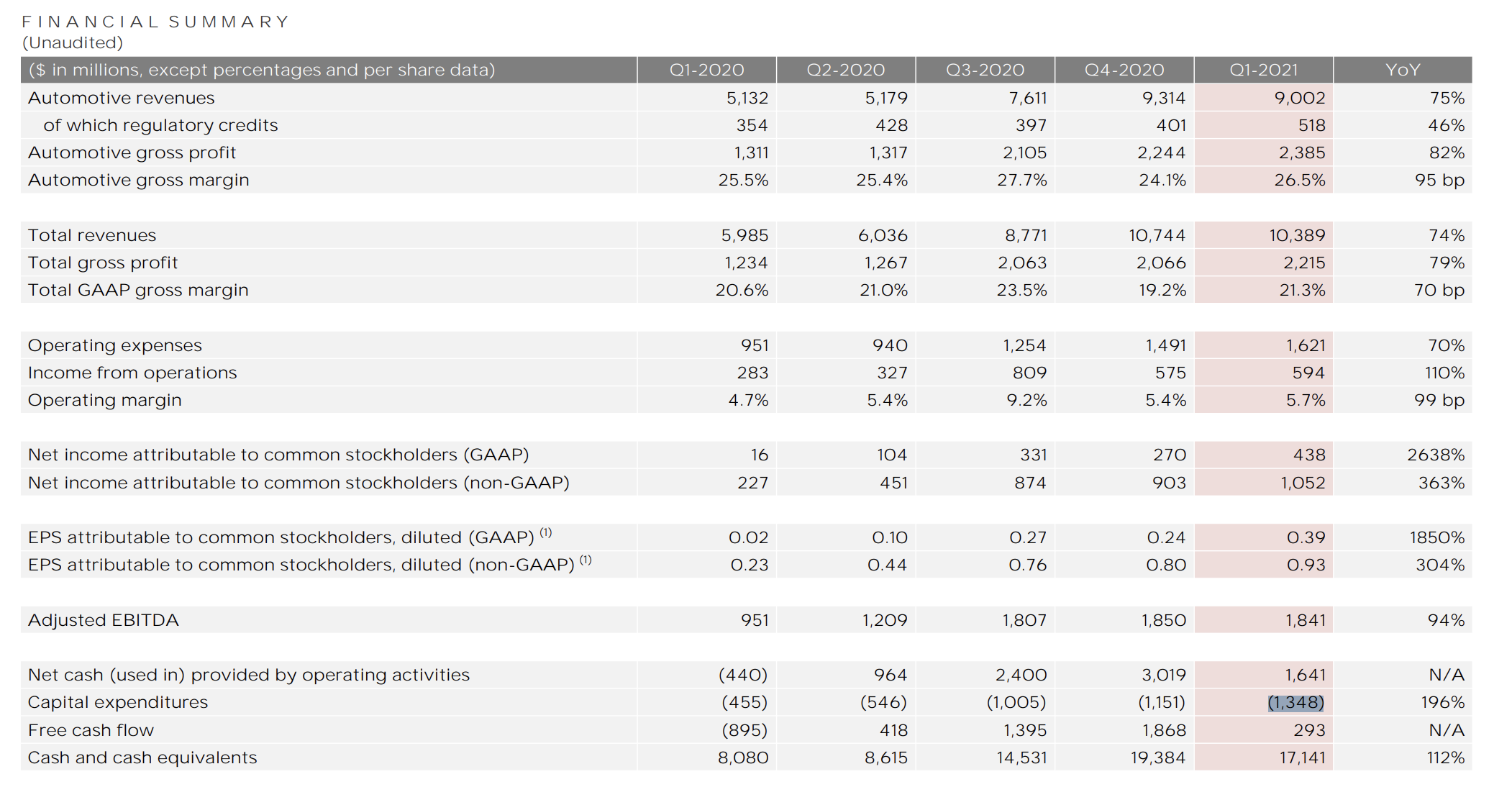

To their credit, TSLA’s regulatory credit are still material and as high as before, contrary to what the CFO had said last year, so this boost might continue for maybe 12 to 24 months. I don’t expect much longer, given that these credits are paid from European manufacturers and now every european brand is launching its own EV vehicles.

As others have noted, profits are still heavily dependent on regulatory credits. Net income = 4$38 million, of which $518 million is Regulatory credits and $100 million is profts from Bitcoin Trading.

On this same topic, it is curious that they chose to include BTC profits inside operating profits and not on a separate line. Unless it plans to have a long term BTC trading desk.

Revenue grew well, but only on a nominal basis. When we take into account the share dilution between Q1 2019 and Q1 2021, Growth in TTM Revenue per share is only 12% per year. If your focus on the core business and remore regulatory credits, we are on a 6.8% growth per year. Equity raises and Elon’s bonus packages are hurting results. Not really the hypergrowth company that is sold everywhere in the media.

According to Elon, 4680 cells will be in production in 18 months. That would be for 2023. That means no Cybertruck, no Semi before 2023. That also means that the Brandeburg Model Y will likely not be powered by the 4680 cell, contrary to what was previously assumed. Let’s hope that for once he can deliver on time, because competition also plans to mass produce these batteries by next year and Big players will take advantage of it.

Does it imply that we should not expect any new model before 2023? That would be weird, given how many new models competition is releasing. I get that TSLA plans to refurbish the Model S, but will it be so good compared to, let’s say, the EQS?

For reference, Subaru sells 1 million vehicle per year profitably, and is worth $15 billion. That gives and idea of the value of the car manufacturing part of TSLA. I guess everything else is related to automated driving and solar.

Let’s talk about solar for a minute. In Q1 solar revenues were $494 million, while Cost of good sold for solar was $595 million. That is a gross margin of minus 25%, for a total of negative $100 million. That might explain why they suddenly increased the price of the solar roof by 80% on existing contracts. Their solar business is a dud, and if it is worth anything, it is really not much.

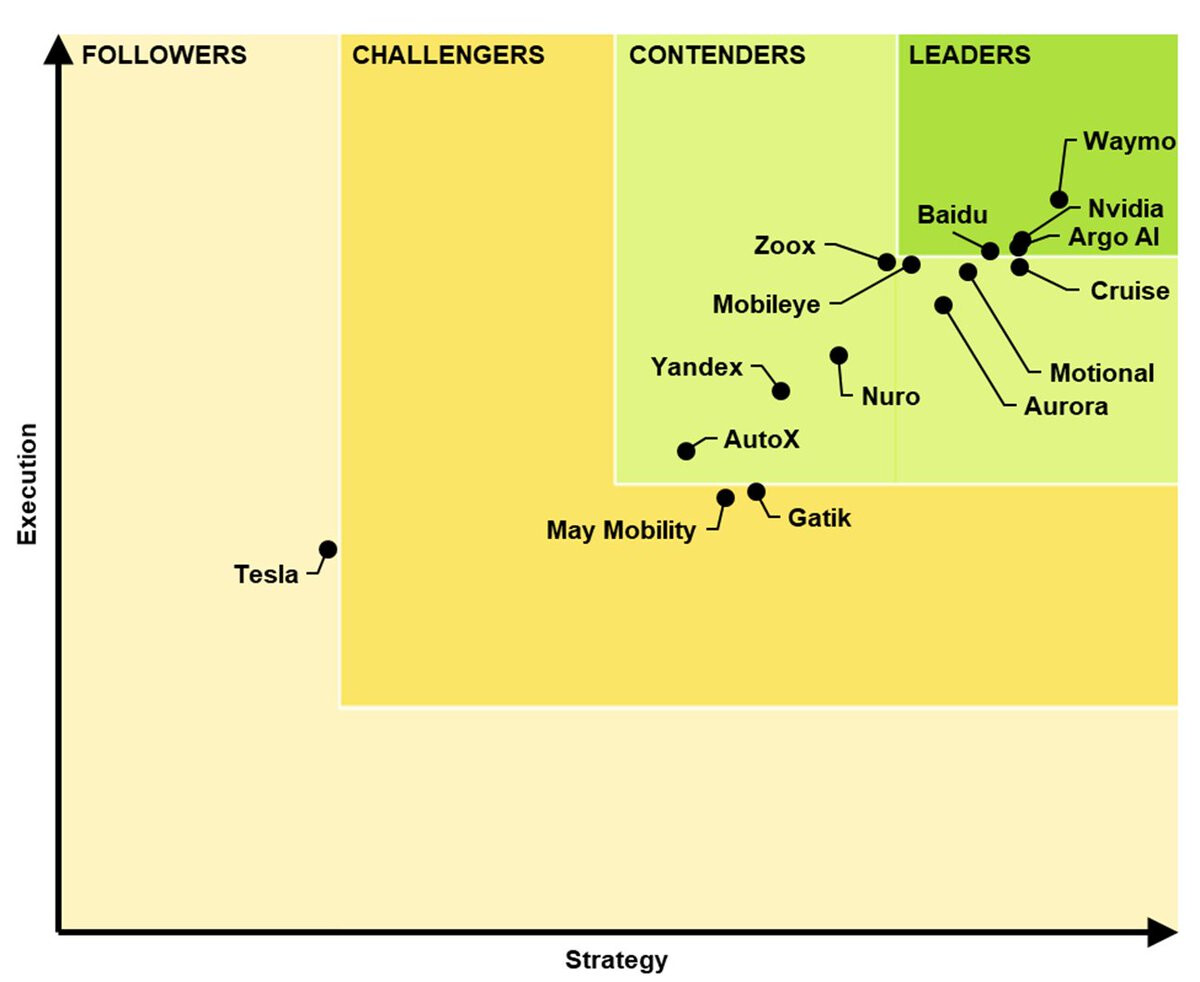

That leaves us with FSD, which makes the bulk of most hopes embedded in the share price. I will sidestep for a moment the recent controversy about FSD naming (*). I will rather focus on the competitive landscape. First of all, contrary to all its competitors, TSLA sticks to refusing LIDAR, claiming that if a human can drive a car with only two eyes, then a car should do the same only with cameras. That would be true if AI was as complex as a human brain. Although AI can do a lot of things like chess or go better than humans, it is still lacking in most domains, otherwise the tech singularity would already have happened. TSLA is lacking the distance information that Lidar provides, which means that AI either has to guess the distance of objects, or someone has to tag them (provided that those objects are visible at all in the videos). What they have done so far is impressive, but still lacking compared to the disengagement data provided by competitors. For instance, there are already company commercializing live autonomous trucks (see here) . And for regular autonomous driving, competitors are plenty and often operating at a higher SDA level than TSLA. But with Musk, I think TSLA getting autonomous driving is still possible: they could for instance raise a new round of equity and go buy GM for instance…

By the way, if someone manages to get the content of this study I would be very interested.

So would I pay a P/E of 1’000 for a company that grows its core revenue per share by 10% a year, relies on external credits to be profitable, has a dying solar operation and is far behind its numerous competitors in autonomous driving? I’ll let you answer that.

A really interesting read. I think the ship has sailed on really seeing a lot of portfolio growth on Tesla shares… It seems though there are still compelling reasons to invest in the company but also compelling reasons not to. It’s great to have such a company & entrepreneur existing in our time… it’s what it must have been like when General Electric was taking shape…

An idea I was exploring (if it’s possible) is to purchase pre IPO shares of SpaceX. There seems to be potential for interesting portfolio growth in the space industry. I have seen the platform Equity Zen offers this, but only through a professional trader. Perhaps someone on the forum has experience with this:

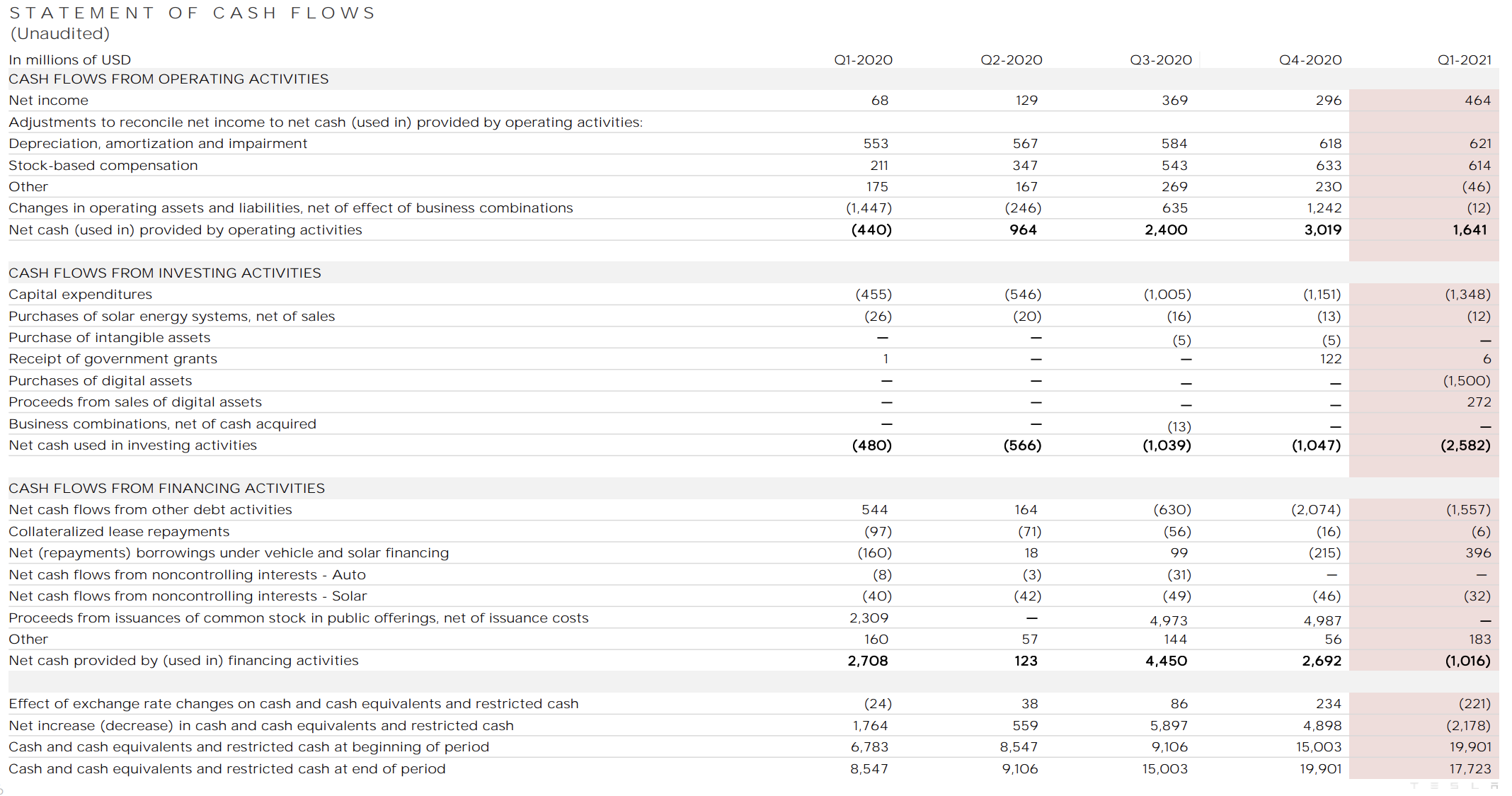

Something is missing. Capital Expenditures have been $1’348 million. This cost will go towards building future cars. So if you want to subtract regulatory credits, you should also subtract capex, right?

If you want to get the feeling of what to expect in the future, you can look at gross margin, which is going up. For the Model Y produced in China, it currently sits at 29.4%.

According to the Shenzhen, China-based financial firm, Tesla’s China Model Y only costs ¥237,930 (USD 36,852) to produce. However, its selling point gives Tesla a 29.4% gross margin with a price of ¥339,900 (USD 52,646.25).

So with the factories that have been built or are being built, Tesla should be able to produce some 3 million cars per year. With an ASP of $50’000 and a gross margin of 30%, we’d get a revenue of $150 billion and and a gross profit of $45 billion.

Not in one year. Capex is an asset that gets deducted from profit over the life of the asset. Example: if the $1348m relates to production lines that will last 10 years, $134.8m will be deducted from profits for each of the next 10 years.

As you can see below, capex in Q1-2021 was $1,348 m. I see that it is deducted after income from operation, so if I understand you correctly, capex is not included in income calculation? By the way, I think it’s fair to assume that operating expenses will not grow as fast as revenue, so more of the gross margin will remain, right?

Correct. In accounting Capex is not included directly in the income statement. It is recorded in the Balance Sheet as an asset. It is then depreciated to the income statement as an expense over the life span of the asset.

If you are interested in analysing companies’ accounts you can google to learn about the concept… this seems like a good link.

OK, so we convert some of our cash to pp&e on the balance sheet. Then, as the factory gets used up, we count depreciation as expense. Now, I wonder how Tesla depreciates its factories. I’d like to see some basic calculation. Like: the Shanghai factory cost X to build, it has produced Y of the Z cars it ever will produce. I guess there is some leeway for the accountants how they want to portray the company’s situation? Like, they could over- or understate the depreciation and in the end this has a huge impact on the cost.

You got it. Depreciation assumptions should be verified by external auditors so I would hope they should be ok.

This triggered me to check who Tesla’s auditor is and the below popped up. Quite a big deal as it implies PWC weren’t able to get the necessary reassurances from Tesla management. I would want to kick the tyres on this (pun intdended).

WSJ article 13 feb 2020 “Tesla’s longtime auditor, PricewaterhouseCoopers LLP, has raised “critical audit matters” following its review of the company’s financial statements, Tesla disclosed in its regulatory filing. PwC, which has examined Tesla’s books since 2005, highlighted that auditing the car maker had particular complexities, including in how the company was reserving money for potential future warranty expenses and the promises it made to guarantee a resale value or buyback option for some of the vehicles it sold”

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.