Maybe I should send some money to IB and put a GTC order for 100@$400, just in case it dips further

Steven Mark Ryan sold everything else he had (ok it was only 3% of his portfolio) and now 100% of his stock is TSLA, some 5500 shares. Ron Baron owns 1 million shares and says he will be the last person to sell. Really exciting to see who of the smart people will be right, the bulls or the bears…

Dear @dbu, you are wrong. Please distinguish between his private stock and the stock of his fund. It’s not responsible for a fund to hold so much of a single stock, when it comes to risk management.

“It was painful selling every single share,” he said, adding that he personally has not sold any of his more than 1.1 million shares of the electric car maker. He said “risk mitigation” was appropriate for his clients regarding the sale of their shares of Tesla.

I don’t know about him, but about the fund they write:

Baron Capital held more than 6.1 million Tesla shares as of Feb. 28. They were purchased at an average cost of $42.34 per share. The firm reported selling 1.8 million shares of Tesla from August through February.

The intraday volatility for TSLA has been huge. Think they were down -13% intraday recently, only to close at -5 or so. Glad I held even through the days they went up 6% or 7%, even though it was hard looking at the intraday chart.

Regardless of what happens, even I don’t make any money it’s a good polishing to my diamond hands. In all seriousness, I’ve rarely been exposed to such volatility - so it kind of teaches me to keep calm and ignore the daily ups and downs, focusing on the longer trends.

I watched the Fundsmith (virtual) 2021 AGM yesterday. Discussing valuation and that they tend to invest in more-expensive-than-average companies, Terry briefly showed and explained a compilation of “acceptable P/E” ratios for their companies 20 or 30 years ago. I.e., at what P/E ratio could you have bought these stocks 20 or 30 years ago for an annualised average return of 7%. The take away and important reminder was (is) this: You could have bought them at an “expensive” P/E ratio back then and still fare well.

The list of companies didn’t include a P/E of 1000 though. Now, I wouldn’t bet my life that TSLA is never going to justify their valuation someday. I just am not convinced that it’s very likely, given the nature of their business and sector. Also, you’re not investing in TSLA just justifying their valuation some day - you want the stock to grow in price, don’t you?

The other consideration, of course, should be that investors can stay irrational longer than I can stay solvent (or in this case: That my short ETF is worth anything).

I would strongly advocate not over-exposing yourself to TSLA at these prices. Be very wary of “buying the dip” mentality. TSLA is still insanely highly priced for its current day & next few years’ financials.

Irrational exuberance & momentum allowed the price to get ahead of itself. Market is now deciding what fair value for TSLA today really is. And all these funds taking big profits from the recent growth run-up and re-allocating to less inflation/interest rate susceptible assets will not be helping you.

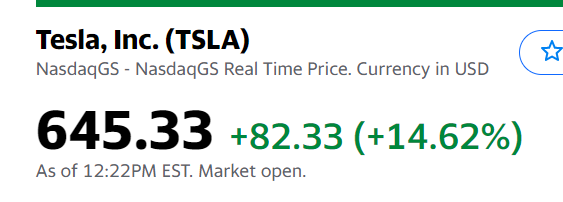

Don’t be caught buying and holding the bag of TSLA at $900, then $700, then $578 today, then $300 next month. And when it finally stabilises holding and waiting 10 years for it to realise its value and climb back to $900.

Why take the risk of 10 years investing opportunity cost? The bull case doesn’t offer the risk/reward at these prices. You need to realise you’re buying TSLA at $600 today, not the $42 of the past.

FYI I have closed out my short exposure now (also see less risk/reward on the bear side) and am content to sit on the sidelines of growth stocks at this time.

That’s a very interesting case.

If for whatever reason the price goes down to 100$, Baron (perhaps with some pressure from his clients) may be tempted to sell all shares (minus one) on the way and he still will have a nice success story to tell with a 136% profit.

At the same time Steven Mark Ryan will HODL (loss aversion plus faith) and hope not having to flip burgers when he is old…

At least everybody agrees that the current price does not reflect reality

Some think the company is worth a lot more, others think the stock is worth a lot less…

If I may chip in, to recall the context:

In December 2020, the company admitted to California DMV that FSD is nothing more that SAE Level 2 automation (see the correspondance here, page 30 of the document: As you know, Autopilot is an optional suite of driver-assistance featuresthat arerepresentative of SAE Level 2 automation(SAE L2). Features that comprise Autopilot are Traffic-Aware Cruise Controland Autosteer. Full Self-Driving (FSD) Capabilityis an additionaloptional suite of features that builds fromAutopilot and isalso representative of SAE L2.

In the meantime, Honda is releasing its first Level 3 car (see here for instance). I don’t know when the robotaxis will be there, but 1) it won’t be in 2021, and 2) Tesla won’t be the first nor the only one to release them.

On the solar energy side, the company accurately stated that the business grew a low since last year. Installed MW went from 54MW in Q4 2019 to 86MW in Q4 2020. A nice growth of 59% YoY! But when we look at the numbers, Installed MW five years ago used to be…253MW in Q4 2015… There is still a lot to do to convince me that the business is doing well.

On the battery cell technology, last time I checked Tsla was still depending on Panasoic to manufacture its batteries, so there is no advantage on this side, yet.

As long as the three points above are not solved, TSLA is only a car manufacturer, where:

most competitor have caught up with the EV trend and they started to release their own models (and will thus pay less regulatory credits to TSLA) → competition is knocking on the door

you need roughly 1 dollar of capital to generate 1 dollar of sales

on 1 dollar of sales, you make maybe 3-4 cents of profits.

With such a profile, I still don’t think that the company is worth a lot more than its equity, i.e roughly $23 billion as of last filings. Current market cap is $573 billion.

EDIT: it would be a sad irony if all this promotional bull run until the S&P admission would leave retail indexers holding the bags…

I’ve gotta say, he is so over-confident and condescending of index investing, that it will be a funny consolation to see him explain himself if TSLA stock doesn’t go “to the moon”.

Yeah. I guess I’ve invested enough of my fun money, I should stop thinking about buying more… That being said, I’m not going to sell for now, I should hold the stuff at least 6 months. I’ll just let it ride, it’s sad that at the top point my m2m performance was at $50’000, now it’s only $20’000. But I think this small bet won’t hurt me that much…

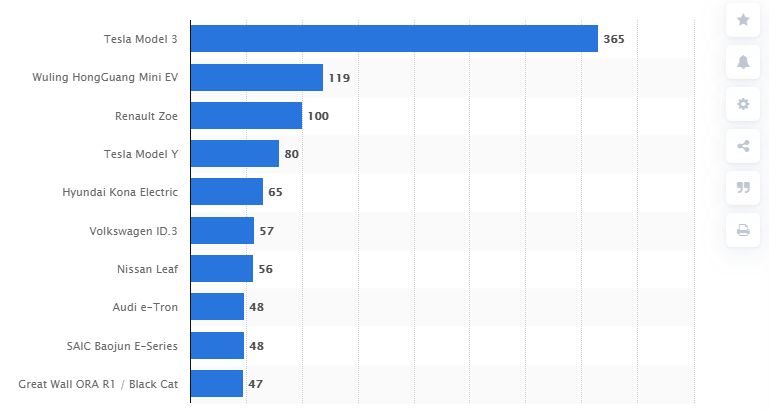

I would be cautious about these claims. At the moment there is no car maker that is mass producing EVs at the level of Tesla. The Hongguang and Zoe are small cars with small batteries. It’s not clear if the ID.3 or the e-tron is produced at a profit at all.

I’m curious to see what happens when all things fall into place. That is:

Tesla implements their latest production optimizations (front/rear casting)

it releases the Cybertruck, which should be very cheap to produce (no paint shop plus other simplifications of the manufacturing process)

it ramps up production of the new battery cell

it ramps up production in Giga Berlin & Texas

These milestones should be reached until the end of 2022. At that point, Tesla could be churning out millions of cars per year, at low cost, which they can then convert to either higher margins or lower prices, killing competition. You may think right now: oh nice Audi e-tron is a cool looking car and it has a similar price to Model S. But what if Audi is losing money on it?

Also, we are very close to EVs becoming undeniably cheaper than ICE cars, when it comes to total cost. Plus they are more fun to drive, more ecological. When people realize it, they will stop buying ICE cars. Are current automakers really ready for this? You think they can switch overnight? Close or refit old factories?

Indeed, I drive the Model 3 and it’s long, usually the front/rear sticks out on the parking lot, and wide, I have scratched the rims in the garage countless times (although that may be due to poor driving).

But what I mean is, is that the battery pack is smaller in these cars, so you need less batteries to produce many cars.

Also, I don’t think you should be driving a car like this on any road where you can go over 50, it’s a death wish

It doesn’t really matter.

What matters is if and that it’s produced - that there is competition.

Doesn’t Tesla’s share price, on the other hand, imply that hardly anyone will be able to compete with them? (Even the shills will are banging on about that).

Why wouldn’t they be unable to switch?

Sure, there may me political wrangling internally…

But the irony here is that TSLA themselves is building cars in a refit car factory - and a tent.

There is competition but only at low scale. Let’s see if they can ramp up production. And of course it matters if they’re profitable. They can’t be selling cars at a loss forever.

It took quite some time to refit that factory and still it is problematic. The factories built from scratch should prove to be much more efficient and provide higher build quality.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.