Really? 69? not 70 or 68?

This year (and last) is really the year of the 69. I see it everywhere (dammit)

I checked it, its CHF 69’420.67 to be excact ![]()

5 Likes

add 2 cents and the internet would explode.

edit: yes i know 67. I’m old school

1 Like

Because of the other Whales in this thread I first thought 1 = 1’000 so I was like:

Damn, what did this guy spend 10 million on in 2024?!

7 Likes

Not just square one but somehow you arrived in the future ![]() How come you already know your networth 2026?

How come you already know your networth 2026?

At your age, traveling and having fun may rightfully take precedence over heavy FIRE activities. Once you earn a decent salary and don’t inflate your lifestyle too much, the networth will rise much faster with your invested savings.

2 Likes

It’s not exactly square one. I’m considering the post I made two years ago as square one. Net worth actually regressed 222.- in two years.

Finally, I am joining the Party here ![]()

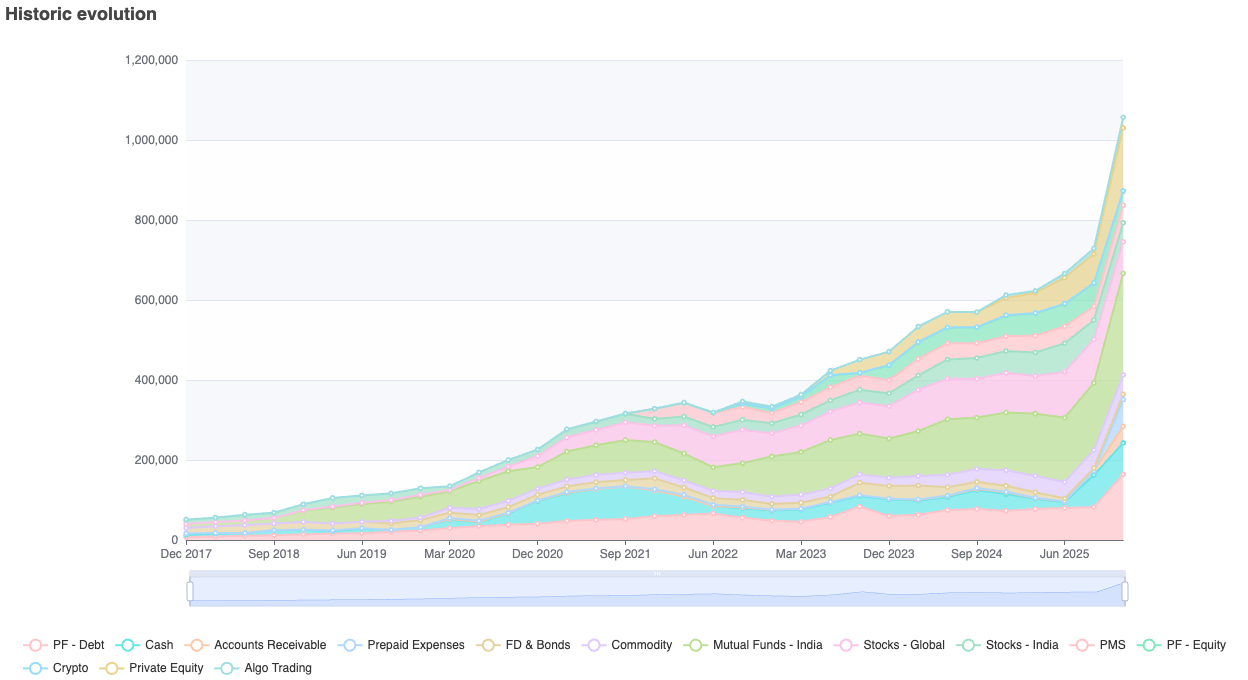

Here is my growth from Dec 2017 to Dec 2025.

Dec 2025 is special because I decided to combine my wife’s portfolio.

Here is the interpretation of the separate components:

PF-Debt - 2nd and 3rd pillar (not invested in the market)

PF- Equity - Market-based 2nd and 3rd pillar

Accounts receivable - Amount blocked somewhere. In this case, mainly from UBS, we just bought a house, and UBS will refund the reservation payment

Prepaid Expenses - Minor component just to keep track of recurring spending like SBB Halbtax Plus

FD & Bonds - Debt-based instruments yielding interests

Commodity - Mainly gold

Mutual Funds - Kind of ETFs (focusing on Indian stocks)

Stocks India - Personal managed Indian stocks

Stocks Global - Personal managed NON-Indian stocks & ETFs

PMS - Professionally managed Indian Stocks

Crypto - Negligible

Private Equity - Non-listed companies

Algo Trading - Money involved in algo-strategies

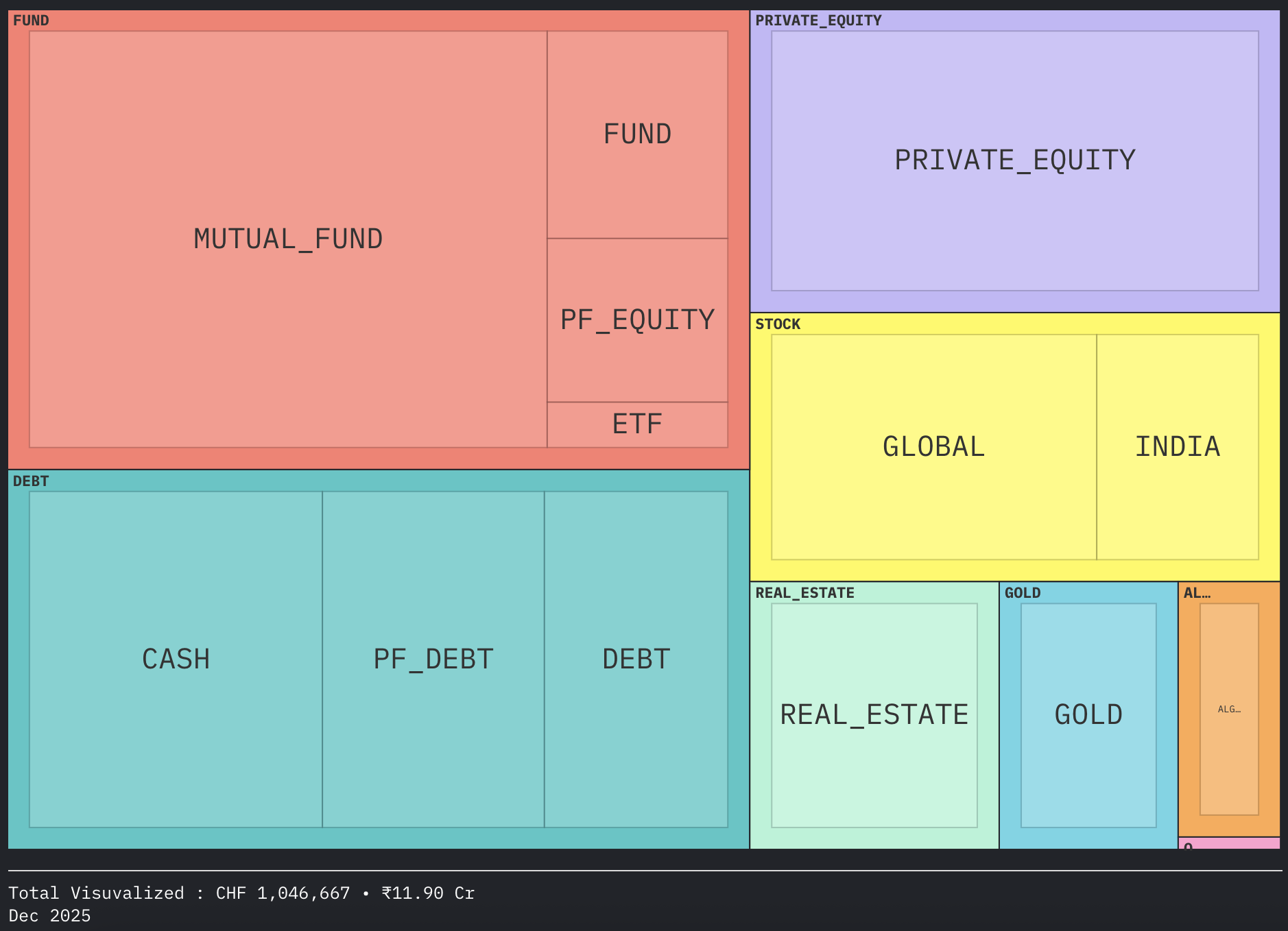

Current asset allocation:

There is still a bit of a naming mismatch, as I did not intend to share when I created them.

Looking forward to your feedback. Happy to share my investment philosophy and other aspects as we go forward! Please also DM me if you have any suggestions/offers/ideas.

4 Likes

It is brand new and Nebenkosten include maintenance costs. Both actual ones (e.g., repair) as well as a Teuerungsfond.

It isn’t perfect, no. But perfect is the enemy of good enough.

I have a 10 year mortgage. I am very happy to sell (if not done so at that point) if I am unhappy with the new mortgage. I will certainly move away when/if I retire early. Somewhere where taxes are lower and I am closer to the mountains. So that point also doesn’t apply.

It is unlikely that anyone buying in the last few years would have a sound investment on a standalone financial basis

Can’t agree with this. Was it optimal? No, what is, but it was very good. My 8% is not even including the increase in value.

Nor does it include opportunity cost of locked capital.

Anyway, I agree it’s tricky how to consider a primary home in FIRE not only on a mathematical side. There’s a huge difference between people “happy to sell, happy to move, happy to “downgrade”, happy to rent if a better deal comes up” and someone tight to a place / location (family, roots, taste, comfort, loving your house) when calculating net worth and FI target.

In that case, your real estate may as well do a x10, either you stay in and it does not make you richer in terms of FI despite your beautiful graphs.

Let’s say my FIRE number is 3M, my debt-free real estate grows from 1M to 3M, here I am with my F-U number, what do I live from?

One could argue that as a renter the x10 (or x3) may as well translate in rent increase and as an owner you’re supposedly protected from this inflation. Thing is, it’s still a 0 cash-flow return you can’t realize living in it, and you have to have some other assets to cover non-housing costs as an owner.

It can be misleading in terms of financial planning. I see a lot of RE/primary home above 60% of total assets among this forum’s millionaires, with huge increase steps “when the bank did the valuation at mortgage renewal, woo-hoo I’m closer to FI”. I’m curious about the early retirement plan, if any.

As owner you may leverage some (more) debt, but that’s another story (how many are ready to take on mortgage debt and interest risk to put that in a portfolio you’re supposed to live from when FIRE’d, also it’s not guaranteed the very concentrated asset value grows forever).

As a renter a well invested portfolio could cover housing cost (and every other cost) even after inflation.

3 Likes

Impressive curve! Makes sense to combine all assets between spouses and plot it. As a whole, the asset allocation looks a bit complicated to me. Every asset class and every single stock needs a bit of mental bandwidth to keep on top of things. Maybe have a discussion, find common ground and simplify things in the future? There are other things both of you may want to consider:

- Cost of instruments: Funds, Mutual Funds and managed portfolio probably have costs of >0.2% (which for me is the current acceptable threshold)

- Potential home bias: a lot of India in the mix.

- Private equity could be a concentration risk, if only consisting of a few companies

- Large cash and cash-like part. Perfect if you are intentionally building a “war chest” to buy into a dip. Otherwise a bit large.

Hope this gives you some ideas!

2 Likes

Thanks for the detailed look and thoughtful suggestions. Really, really appreciate it.

Mental bandwidth: Totally true; in addition, having a concentrated portfolio could yield better returns too. So that’s indeed my plan. Let’s see where I would stand in the next quarter.

Cost of instruments: The main reason I keep in Funds insterd of ETFs is because of the Taxes. It’s a bit in a gray area in Double taxation taxes, I might be able to pay capital gain tax in Switzerland (at 0%) instead of India. For ETFs i have to pay long-term capital gain tax of 12.5%

Potential home bias: That’s very true and also a conscious decision. India is now the fourth-largest economy and will soon surpass it to reach third place. Also, the GDP growth in USD terms is the highest in the world. I believe it would also appear in the top line of the companies and also on the valuation.

Private equity: Very true, too. I didn’t intend for this portion to be bigger; however, the gains in this section are insane. For instance, $7k invested in Anthropic became $50k in about 1.5 years. I don’t want to cut the gains (in the name of re-allocation) as these valuations are going crazy (probably due to AI bubble ![]() )

)

Large cash and cash-like part: That’s mainly due to some locked capital and shift of the 3rd pillar for the mortgage that will start from march 2026. I thought to go in again in equity if there is a dip, but it seems like the equity market is rallying as if there is no tomorrow.

Open questions for me:

-

How do you all account for the mortgage? Would you just add the downpayment in the portfolio and call it the value of the house? Or is it preferable to show the actual buy value of the house and subtract the debt? I feel the first option to be conservative, and also easier to account for.

-

Over the recent years, I started build options portfolio. While the section (pink bottom) is not even visible, its exposure is quite big. For now, I just show the market value of options in the portfolio, but I am wondering if I should show it as an asset for the LEAPS positions at least.

-

What is the overall view of the reallocations? By doing it, are we cutting down the winners or making the portfolio more resilient?

-

How do you all keep track of your learning? Do you store the quarterly networth somewhere with hypotheses and goals, and backtrack it to see what works well and didn’t?

1 Like