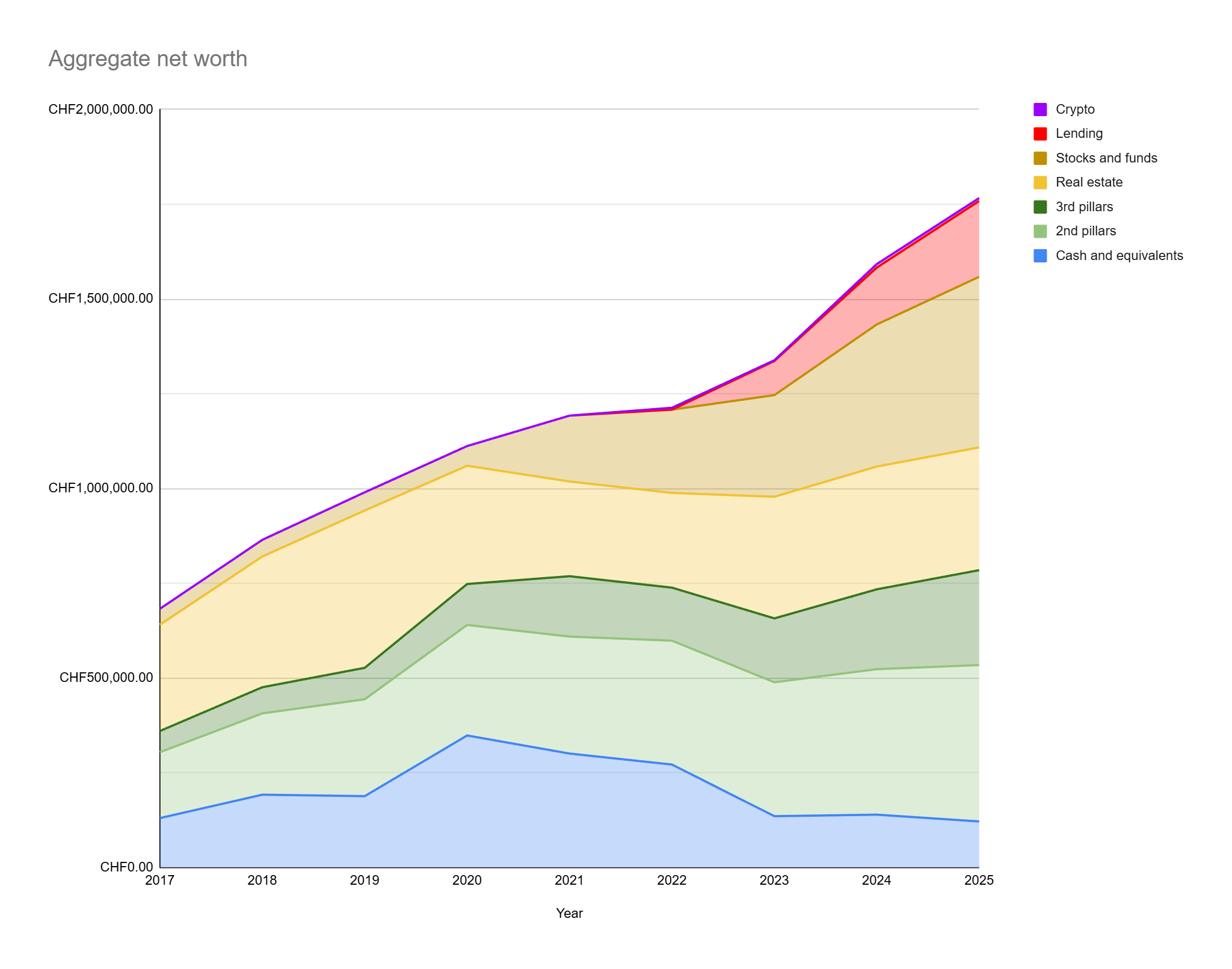

I hold assets that are valued in USD, CHF and EUR. The balance sheet I did provide is in CHF and I have it calculated in USD and EUR too.

But my stock trading happens all in USD, all dividends are in USD, all realized capital gains are in USD, why should I measure it in an exotic currency like CHF, a currency which I spend less than EUR.

I am in the process of changing my USD debt to CHF; the interest difference is a nice insurance long term. And it looks like I got a temporary low with slightly under CHF 0.79 to the Dollar.

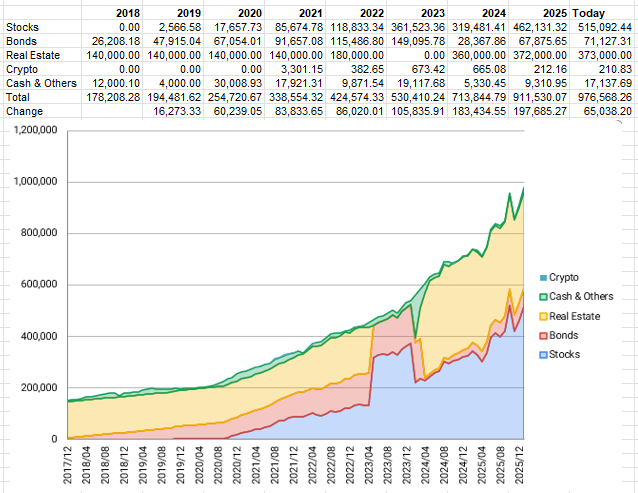

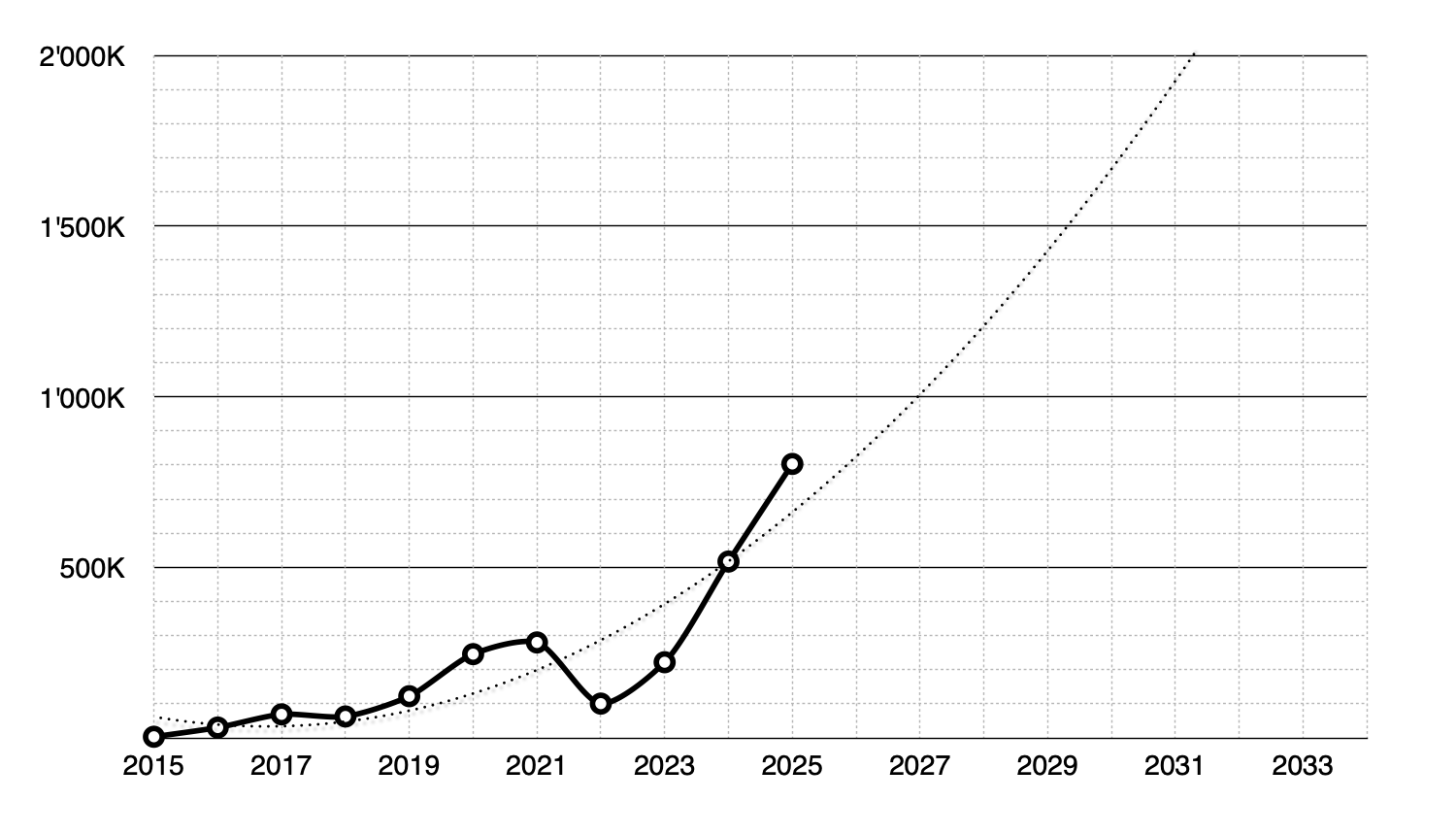

Yeah in 2025 growth was mostly driven by a good savings rate (+42.7k) and pension fund increase (+11.5k), not so much by market returns (+3.4k). Bad year for crypto and got unlucky again with my timing. Almost half of those savings/investments were from my bonus (as usual) which is paid out on February 20th every year. Which was exactly the top before the March/April crash in 2025.

Btw, I bought another plot last month in Bosnia for 10k. I’ll see how this will play out long-term, but I think it will be a great investment. 5 years ago I wasn’t planning on any RE and today it’s 35% of my total NW lol. Next goals are to hit 400k in autumn this year and 500k before the end of 2027.

My NW increase of 134k since last year (+9,7%).

I’ve saved 95k (including LPP) with an average of 50% saving rate.

Unfortunately this rate will drop as my wife is still looking for a job with no more unemployment benefit.

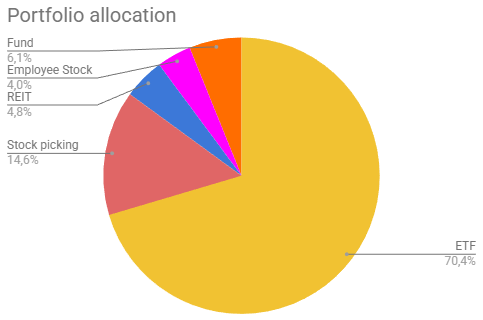

Still with too much cash on the side and too much stock picking (underperforming the ETF section.)

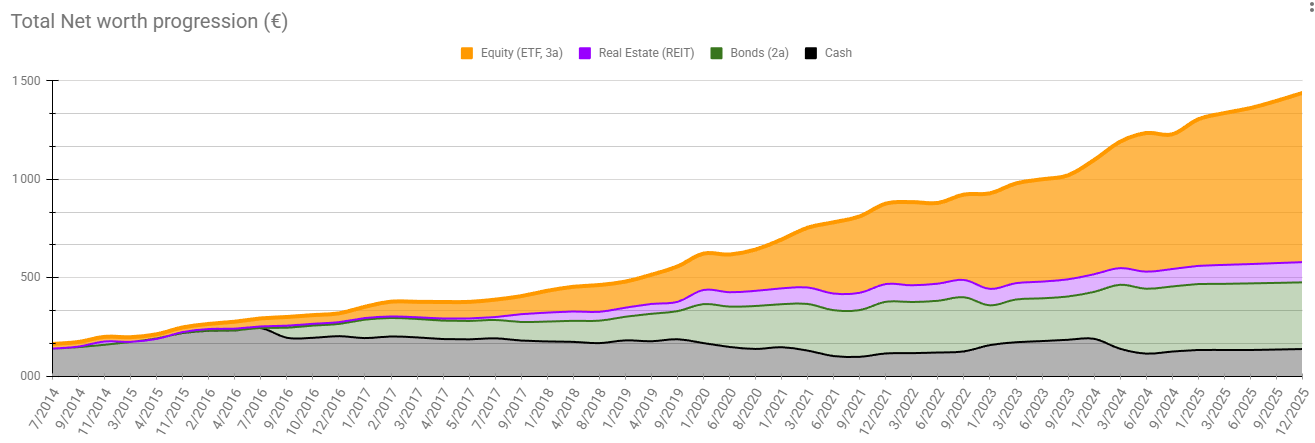

11.5% NW increase, stock portfolio (again) underperformed VOO with about 11% gains in CHF, with some questionable stock picks and my employee stocks going the wrong way

the one good thing I can be happy about is that my SO now has an almost-equal mix of BVG / 3a / corporate bonds / stocks / real estate

I can’t really decipher IBKR reporting to be honest

The performance tracker says I underperformed SPY, but the NAV and everything is (should be) shown in CHF and SPY definitely didn’t go 18% in CHF this year….

Problem is that IBKR is only showing performance benchmarks in the main currency. So your NAV is shown in CHF and the benchmark most probably in dollars, hence the difference.

Yes. In my opinion, that’s just a completely broken chart. Comparing relative performance across different currencies practically never makes sense. You can even hold 100% VOO but if your base currency is not USD, you see a huge difference to the benchmark. I would attribute it to US-centric developers but Swissquote has the same bug (At least Swissquote allows changing the currency of your own portfolio in the chart, so as long as you know the benchmark currency, you can make the chart make sense with an extra step).

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.