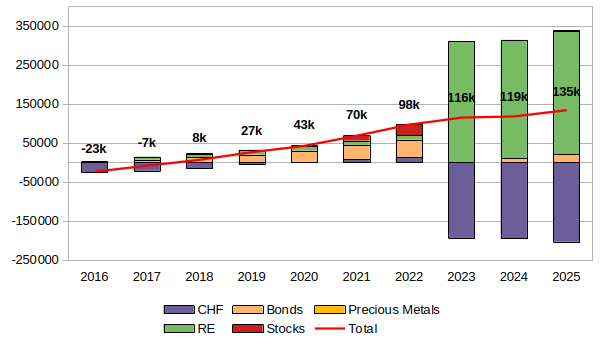

YoY in CHF

- +26% in stocks (38% of it contributions)

- +1% in 3A (didn’t contribute this year)

YoY in CHF

Still mostly in cash in preparation for my home renovation project (which has completely stalled this year but should take off in 2026).

Extra expenses went in training, car repairs and pre-paying health insurance.

Happy New Year, hope you all enjoyed some time off ![]()

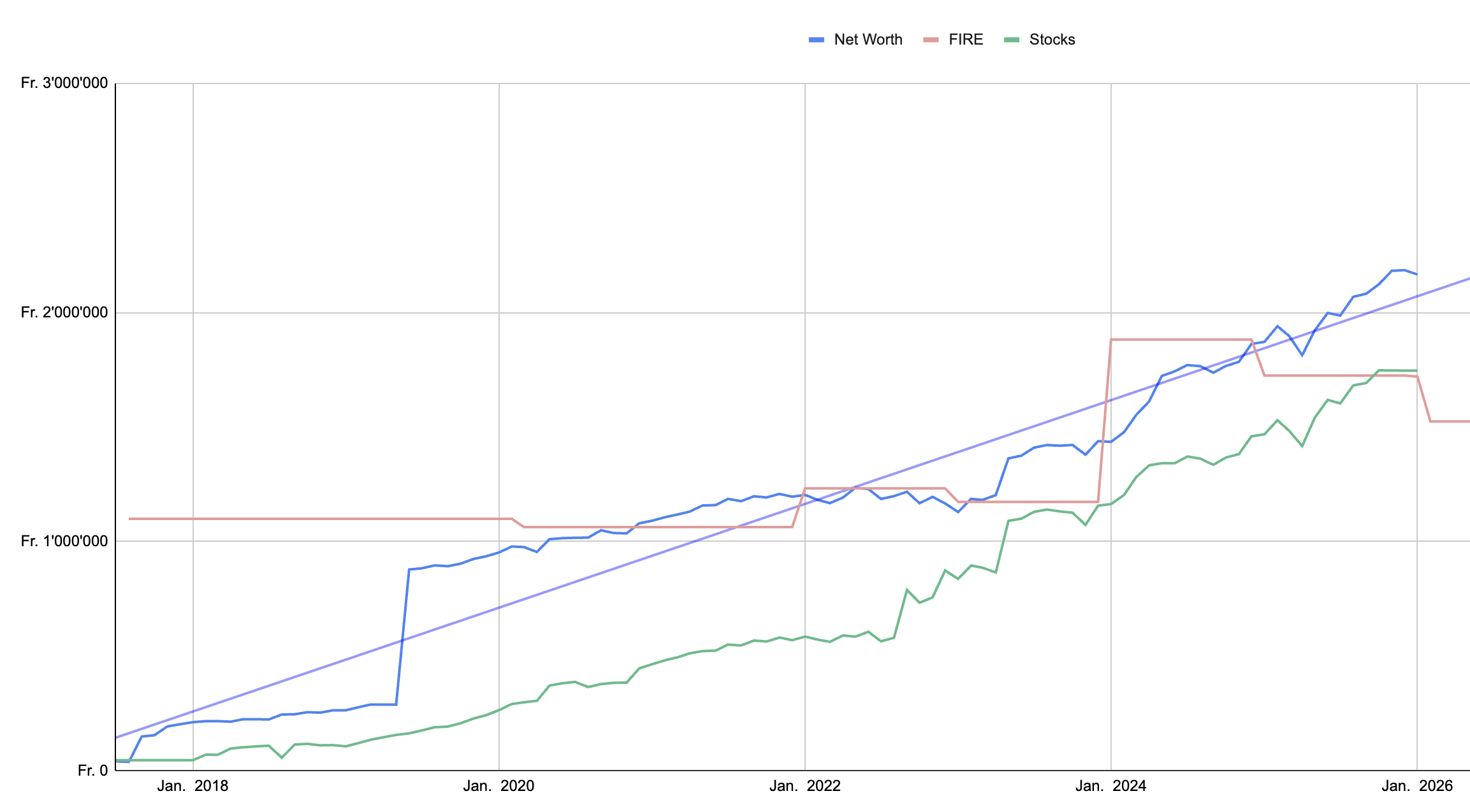

This was a very eventful year for my net worth:

Both together resulted in an NW increase of almost a million, going from just under three million to just under four million. Of course this is a very early estimate, I am especially unclear about my 2025 cash bonus expectations and how that will turn out.

Edit: Reading this again myself, I should clarify that I consider cash bonuses in my NW as they are fully earned by year-end (just uncertain in final amount for now). I include unvested equity gradually through the vesting period, and was expecting only a much, much lower NW increase this year, losing unvested shares against new savings and returns.

That looks like an exponential coronavirus graph from 2020. Congratulations! ![]()

Yes, Excel tells me I am a billionaire before reaching retirement age ![]() In reality, I have zero expectations that those last two fantastic years will continue, but I am still highly overpaid, so no worries

In reality, I have zero expectations that those last two fantastic years will continue, but I am still highly overpaid, so no worries ![]()

Time to sum up 2025. It’s been another good year.

Net Worth went from CHF 2.6M to 2.84M (+ CHF 247k, +9.5%), which is a new All Time High.

The equity share went down from 45.6% to 44.5%, despite my ETF portfolio hitting an All Time High as well (CHF 1.26M, IRR 10.3%). Thanks to abandoning my options trading I have some dry powder to invest going forward.

My investment strategy for 2026 remains largely unchanged:

* “Eternal” IBKR portfolio will look like this:

4,000 VWRD

2,000 VDEM

1,000 VHVE

1,000 CHSPI (848 today)

250 SMMCHA

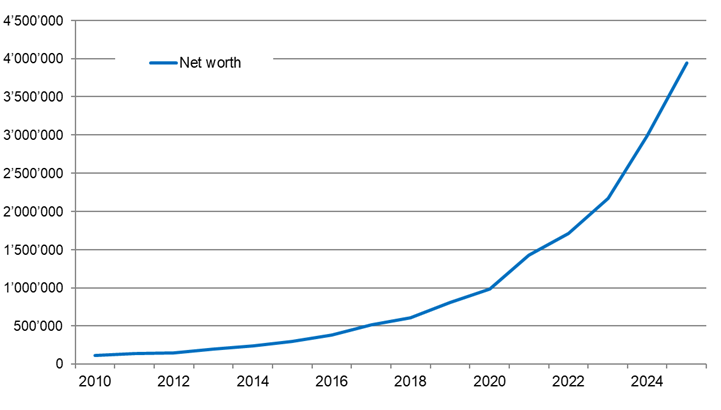

What happened here. It took over 10 years to get to 1MM and then you get to 4MM in a few years. OK, you get a 1MM bonus this year, but still. What happened since 2020? Did you own patents on MRNA ![]()

is there a board rule how to handle real estate in the calculations?

I think market value (if known) minus debt (best is split it out) is the most logical.

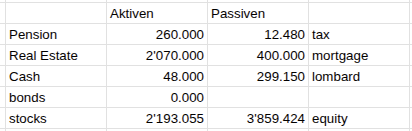

E.g. if you look above, @Wolverine post has the negative debt component (below the line).

My NW this year grew 32%. On average since tracking it grew 27% per year. So, in that sense nothing happened really, it’s just the payoff of consistent savings and investments over many years. And that it took 10 15 years (first five not tracked) to get the first million is also kind of the point and hopefully the element taken positive and as motivation here: It does start slowly and takes a long time, but the investment gains will snowball eventually.

And to give a real answer to the puzzle too: In 2020 I became a top 1% earner in this country, and have doubled that income since. So yes, the exceptional part in my story is that my income grew in fact exponentially. What also helped, is that I had employers that offer 1e pension solutions, allowing me to heavily optimize taxes without losing out on investment returns.

can I ask, what industry do you work in? i am in big tech and it does not seem that 1e is generally available (it isn’t at the two companies I’ve been at, at least). It’s being discussed whether 1e may be introduced at my current employer, and I’m not sure whether this would actually be beneficial if it makes things complicated when moving jobs in future to non-1e companies

Not in tech, and to my knowledge, none of the big listed tech companies offer a 1e plan in Switzerland. I guess the problem is twofold: Switzerland is just another location (even for Google), why would anyone bother to assess such a niche solution. And, those highly profitable companies aren’t bothered by the balance sheet impact of the standard Swiss pension solution, so they don’t value the benefit as much (because that is the argument to convince your CFO: A 1e solution effectively transforms a defined benefit obligation into a defined contribution obligation, meaning you don’t need a balance sheet provision reflecting the risk of an underfunded plan as you transfer the risk to the employee).

Well, you get to keep 100% of the return, but you also need to manage 100% of the risk. But that is the beauty of it: You don’t have to deviate from a standard BVV2 investment strategy with a 1e, but you can. Also, legislation is in the making that will allow you to retain a 1e solution for up to two years, even when changing employer to avoid forcing an untimely sellout.

And when the employer assessed it, employees (at least enough of them) were against it.

I don’t think there is an official consensus as to how to account for real estate. Most people seem to use equity (market value - mortgage) as the value of their real estate.

I consider that leverage is leverage no matter the collateral and apply the debt to the whole portfolio, so I use the market value for the value of real estate and consider the mortgage as a negative cash position (as it’s a SARON one - I would probably use a negative bond position for a fixed rate mortgage).

I find that last version more honest when it comes to evaluating returns. I’m comparing unlevered real estate to unlevered stocks and applying a global leverage on the portfolio, whereas people who consider the mortgage as part of the real estate asset may (or may not) consider levered real estate returns as their core real estate returns.

Plus, the amortization decision comes down to buying more financial assets vs amortizing the mortgage in my case, so keeping the mortgage will litterally allow myself to buy more stocks.

Even that can be tricky, unless it’s a very recent buy or there are a lot of comparable places. According to my bank’s recent valuation, my place is up over 40% since I bought. That’d more than double the equity. Questions are, how reliable or biased is that estimate, and would anyone pay that price? Well, possibly, it’s still peanuts to all those income millionaires in here ![]()

Yet even if market prices went up that much in a few years, I’d also have to pay those higher prices for something else if I had any intention to move.

To be conservative, I consider my purchase price, only.

Either way, it’s just a number for personal entertainment for the moment ![]()

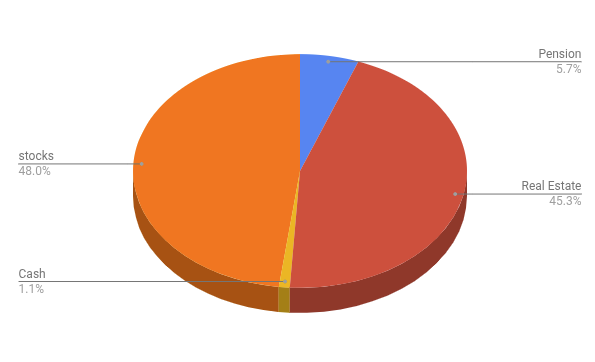

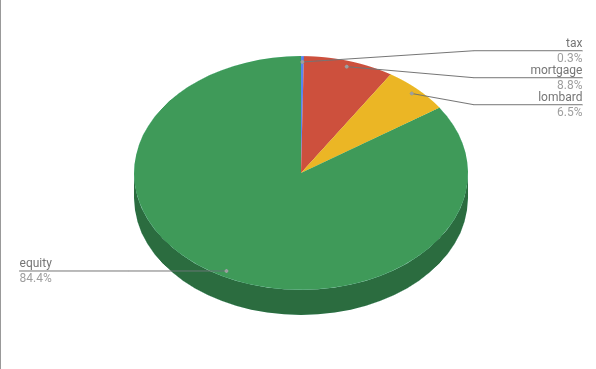

I do a traditional balance sheet in CHF, then translate the equity to USD and EUR. All currencies had new highs in December.

My house has a value of zero, actually minus 100k, but my land is worth a lot since the change of construction zones. So I calculate the land price minus 100k for the house on it. For my vacation home in Spain I calculate half of the current value. Real estate in Spain is very volatile. That means a lot of gain for the real estate, but stocks did gain even more. In all currencies…

I used the low dollar to switch most of my debt to CHF. I pay 0.87% for the margin credit and 0.75% for the mortgage. Soon one will not be able to deduct debt interest from tax any longer, so I decided to take that little risk. The risk is little because as I already displayed in several charts Forex volatility is peanuts compared with stocks. And there has not been a 5 years period where the interest difference was lower than the value change. Since the first world war the CHF is the only currency that had a significant rise compared with the USD. But this year the U.S. will repossess the oil business in Venezuela and that may change the picture.

I am criticized quiet a lot because I calculate stocks in USD. I trade exclusively in US markets and want to measure the performance and compare it to indices. I spend mostly EUR (which is a failed currency, I don’t hold any more than needed), then CHF, then USD.

Pension is for my wife who still works, the tax is what she will have to pay if this doesn’t change until then.

This is my balance sheet in CHF:

It doesn’t really matter what currency you base your calculations in. It will vary between people as some will have mostly income and expenses in CHF, others in USD others in EUR.

Here’s my update:

YoY: +294k (+16%) → around 140k came from savings

126% FIREd based on 4% rule

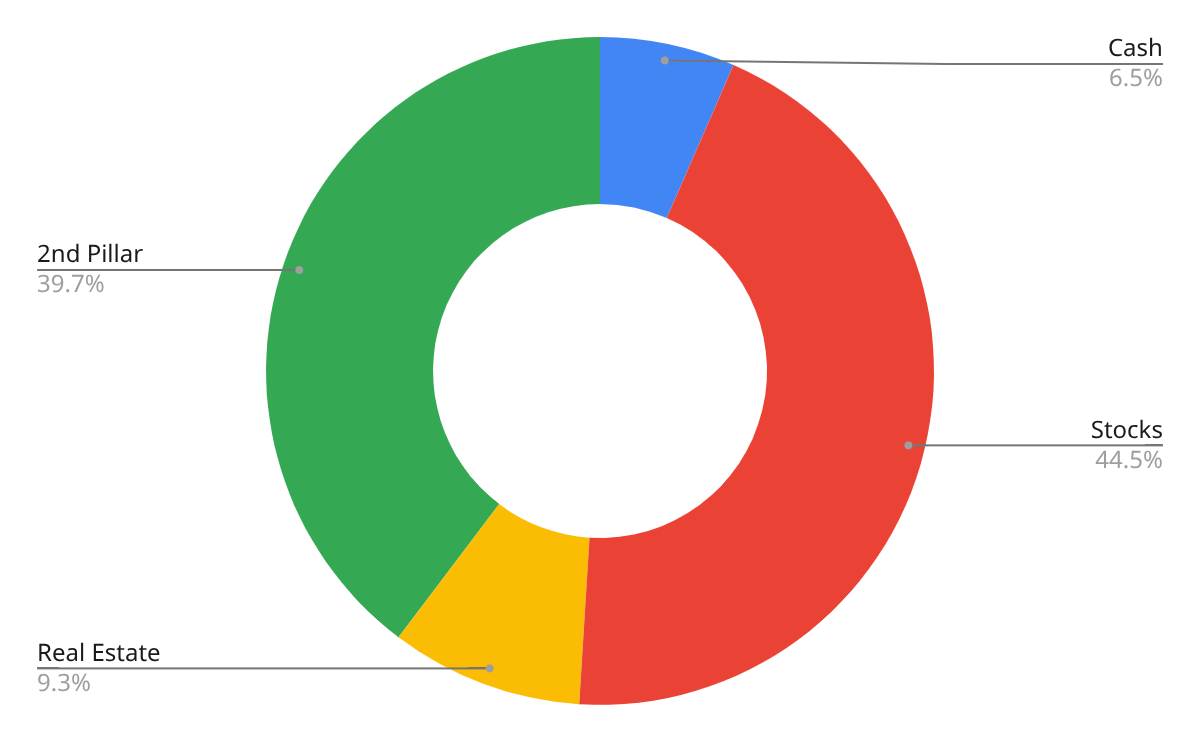

79% Stocks (VT, SSAC and similar like 3a)

8% Pensionfund

1% Gold & BTC

12% Cash

Waiting for the stocks to be at 75% to rebalance to 80%.

Costs around 70k (36yo with 1 kid, household costs are split 50/50)

Now a interesting (or boring?) period starts for me, since I reduced my job due to health reasons to 50% and now the income will cover exactly the expenses - will keep it like this as long as I enjoy it or pull the trigger if not.

Furthermore I had the last vesting came to an end and therefore I won’t experience “big“ payments for the foreseeable future… what leaves a bit the feeling of having finished your favorite game… My savingsrate will go to almost 0% for the first time since 2017.

However my health should get better slowly and thats the graph I should pay more attention to than this one here ![]()

I wish you all a prosperous 2026 ![]()

Ok, I’m having my little OCD tantrum here:

otherwise highly appreciative of your contributions to this forum ![]()

Let’s befriend and keep things quiet. There’s also some actual mistakes about some current stuff.

We’re not an English native speakers forum and everyone’s their mistakes and style, their signature, it gives some personality.

Concerning the USD scandal, @cubanpete_the_swiss is a (really) active stock trader on US stocks market, it’s understandable that he compares his bets and moves to US stock market with the corresponding unit. Adding CHF forex in the mix would just jam the mechanics.

Though bearing his lombard now in CHF, he’s added that into the mix anyway.

Whether that’s a good bet for a Swiss-investor-living-mostly(minus some few days)-in-Spain only him can tell, everyone’s situation is different. But from a portfolio management, there’s some logic.

And I don’t think his goal is to pump up the numbers. His balance sheet at the end of the year is in CHF, as for his tax report, he knows very well where he stands.