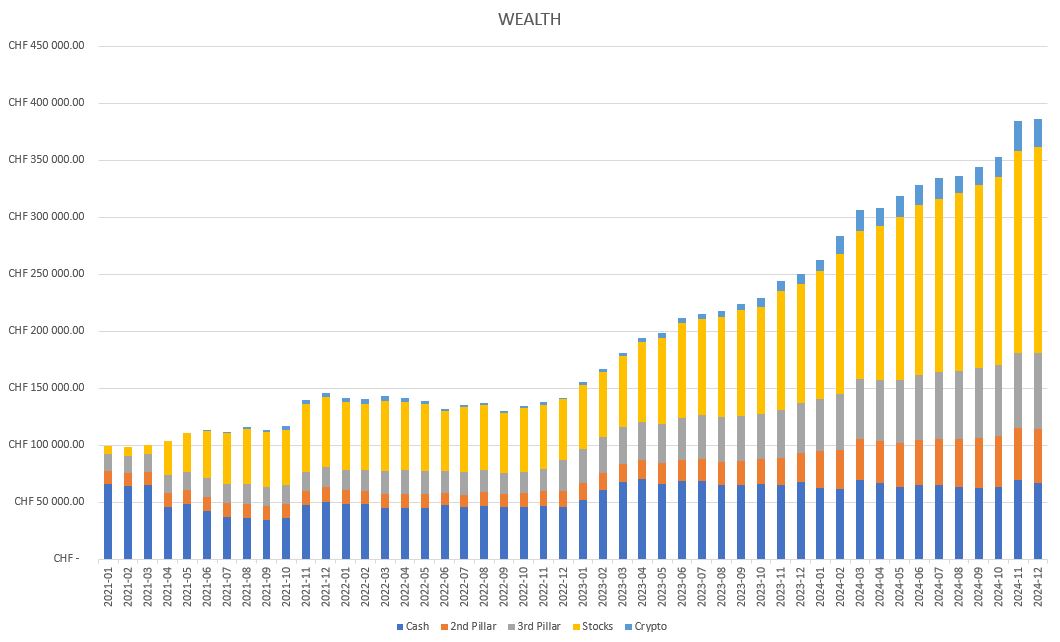

A little background: 2021 and 2022 were transitional years for my girlfriend and me. We were either studying, interning, trying to get a permanent job, or struggling to keep ourselves healthy. We gritted our teeth to achieve our goals.

The year 2023 was our first year with our first real jobs and steady salaries. We used this year to save as much as we could, to indulge ourselves, to make necessary and useful purchases, and other useless ones that gave us pleasure.

The year 2024 was a year of financial stabilization, we were still employed, and I passed my bar exam. I took the opportunity to look for a new job, which I’ll start in March 2025. My little bag of crypto also worked wonders!

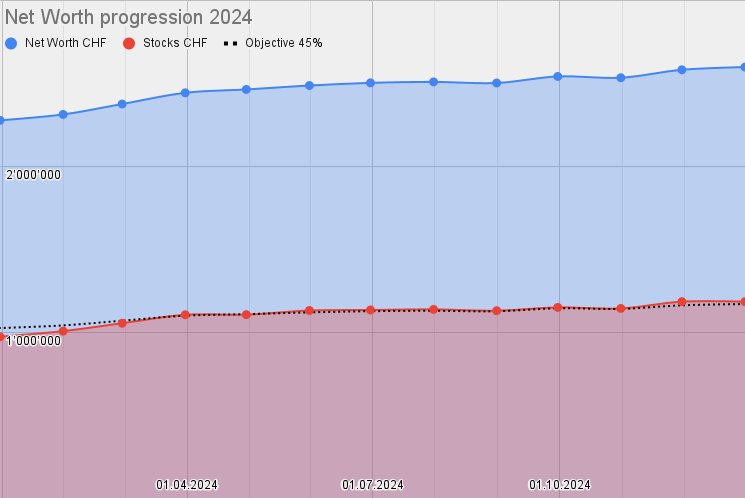

We can definitely see a “drastic” change in our fortunes starting in 2023! However, it’s possible that this evolution will slow down this year, as my girlfriend has signed a permanent contract, but will be paid less (she was on a temporary contract before, with terrible social conditions, but well paid). As for me, I’ll be at 80% this year (hoping to reach 100% soon). Our expenses will increase because of me, as I’ll have to rent a room at my future place of work. It’s going to be a bit of a shakeup, but we should be okay.

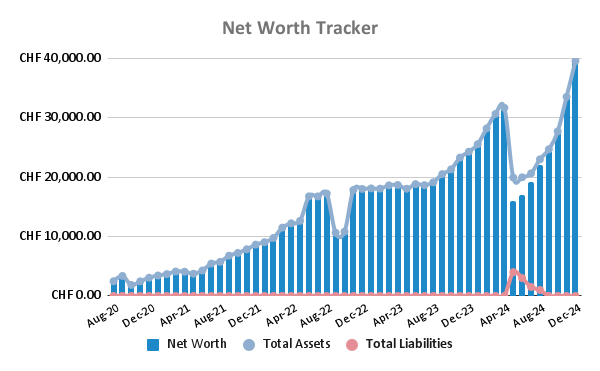

YoY: Change in net worth = +CHF 126’331.91 / +48.6% (stat from YNAB).

Almost hit 40k after owning a nice motorbike bought in september 2022 and after buying a car in may 2024 (way too expensive one but that was ok for me). If I count my vehicles with a correct depriciation in my net worth (my car will be amortised in 3 years), it goes up to 60k which is really nice at 20yo.

That net worth will grow way faster now due to the end of my apprenticeship in july.

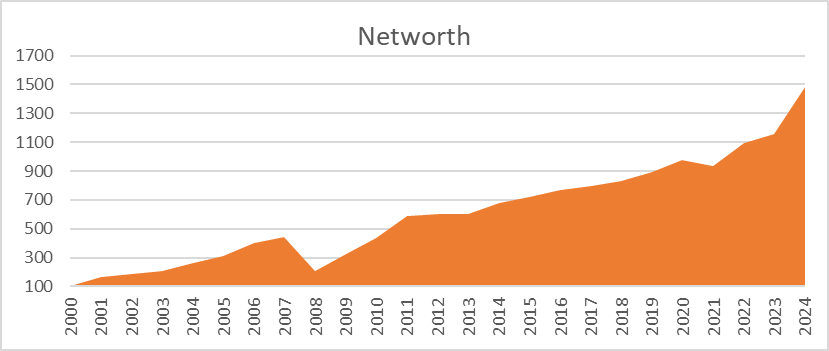

Congrats! Just wondering about the near-zero stock allocation in 2016 but still suffering the drop of the 2008 crisis? I assume you were heavy on stocks back then?

2008 was a personal crisis, with separation and preparation for a potentially ugly divorce. I gave back a generous gift from my parents to avoid it being treated as marital asset by the court. Luckily, it never got ugly and focussed on the wellbeing of our son.

Thanks! I didn’t expect it to happen so quickly… I initially dreamed of FIRE at the age of 45 and achieved it with 34…

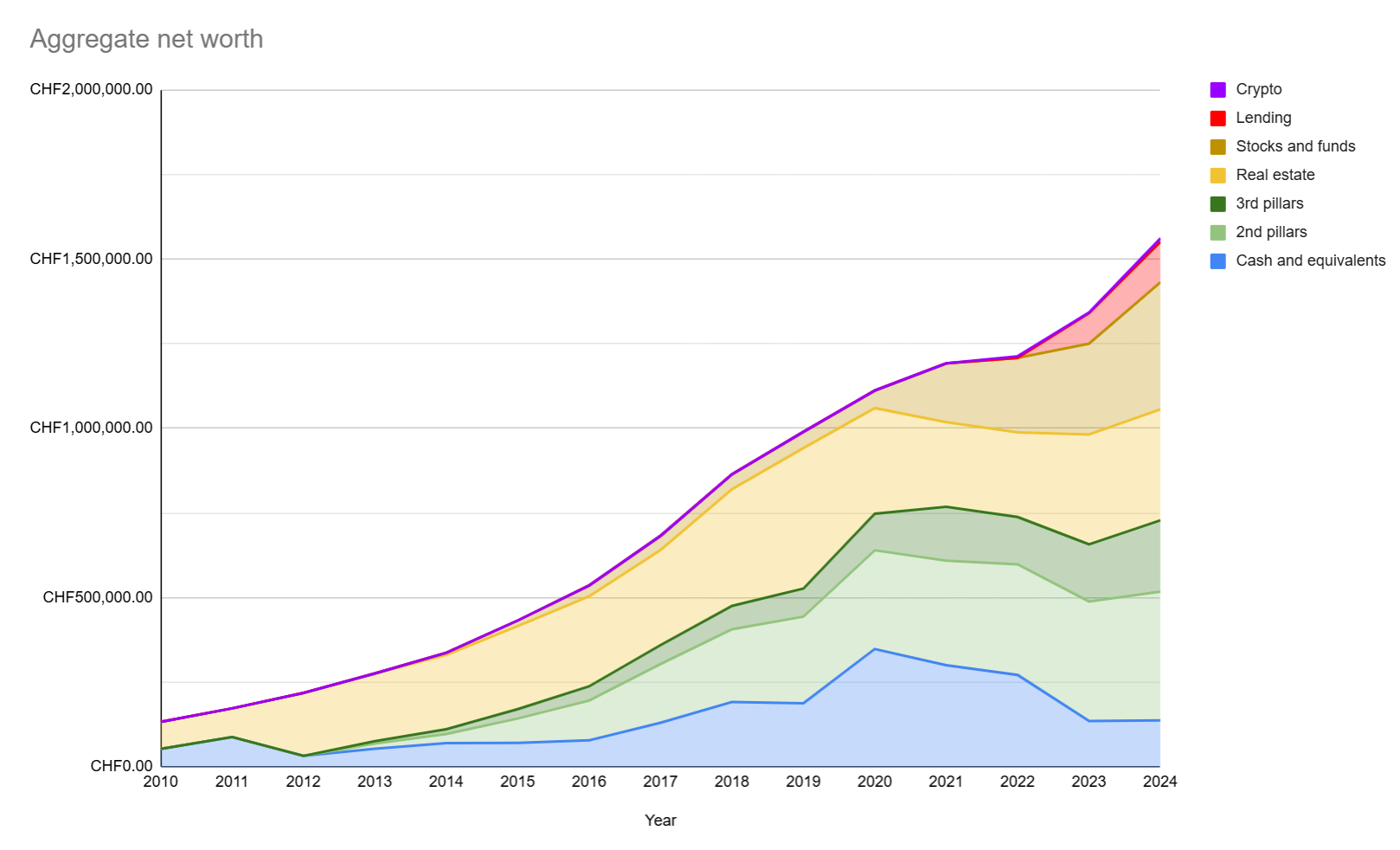

About 40% of my net worth came from a startup exit, while the rest was built through a solid job, a frugal lifestyle, and an aggressive savings rate of 60-70% after taxes. So without the startup (or that startup failing) that would have been a different story.

I calculate the FIRE-Nr like this: Yearly expenses (without income taxes) x 25

This is based on the 4% rule, one could as well multiply with 28.57 to have a 3.5 withdrawal rate. I just used it for motivation purposes, not sure which withdrawal rate I will use once I pull the trigger.

Interesting point re. Taxes. I tend to agree that, given there was no Capital Gains Tax and taxable dividend yield was minor (vs. capital gains), taxes was less a challenge. But at the same time, there is AHV and Wealth Tax. So the picture becomes a bit fuzzy. Are you sure that this holds? Or should we not rather say that if we assumed 4% SWR, the effective, consumable SWR was only something like 1% lower (0.5% Wealth Tax, 0.3% Dividend Tax, 0.2% AHV)? So… the prudent (for a 4% SWRer) view was that you need 33 times expenses (net of tax)?

You are absolutely right, counting no taxes or ahv at all would not hold.

In my case, I have other expenses linked to my work, like childcare, commuting, etc. which will cover easily for the post fire taxes - therefore I just took the lazy shortcut

A data point from that other group that we rarely talk about.

My lucrative exit story was up to a pretty good start with an IPO making a bunch of paper money into ~$5M unvested and pre-tax, 1/4 of which were going to vest in a month. When that month passed, it was already down 40%. That was still good, but as I was mentally anchored at the highest figure I saw in my E*TRADE account, I basically watched it slide down into nothingness (i.e. 1/15 of that highest figure) without liquidating anything.

It used to haunt me even as I kept telling myself “Selling at that low of a price wouldn’t have been life-changing anyway” for some time. Now I am at peace with it - sold half of it at a relatively low price and have kept the other half as a sort of lottery ticket, adding it with a discount to my net worth. FIRE target moved from ~38 to ~50, but as long as me and the family are healthy I’m one happy and content SOB.

Thanks for sharing, I can only imagine how mentally burdensome this must be, and if I were in that situation myself I would experience significant anguish whatever decision I would take… one reason that I am a fan of “single global index fund + chill” in my normal investing, so that there is no decision to be taken

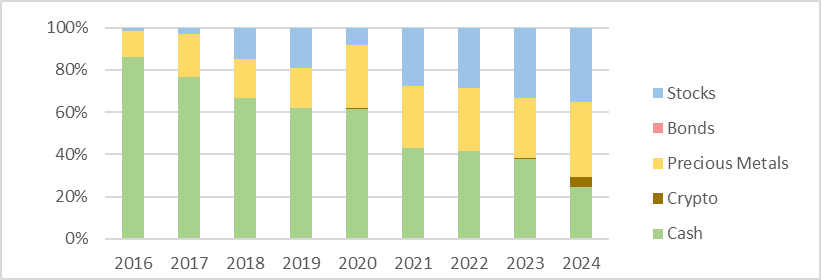

Aren’t you afraid with the “crash that never comes” with so much money in stocks? It could go down 500-1000k in a whiff. (maybe this question belongs to the bottom-of-the-dip thread rather)

Yes, the stocks market can (and probably will) go down significantly. The question is when.

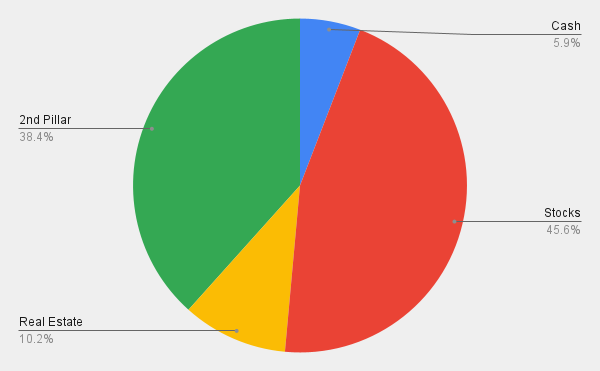

But no, I’m not afraid. With 45% of net worth in stocks, I too think that this is rather conservative compared to others (~80% in stocks or even in crypto). Even if I loose 100% of ETFs, which isn’t likely at all, my life would go on…

It is. I’m just looking at the absolute numbers. Having a 3M NW and losing (unrealized) a 4-5-600k chucnk on a potential 30% downturm would not make me sleep well. Especially around 50 or over.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.