That’s the thing -: most significant returns in equity markets mainly come from concentration. But even a larger number of portfolios suffer due to concentrations. Mostly we talk about the first group

Folks who are heavily exposed to Mag 7 either by luck, Choice, rules, or ignorance must have significantly outperformed market over the last few years. The question is always at what point this changes and would they diversify in time.

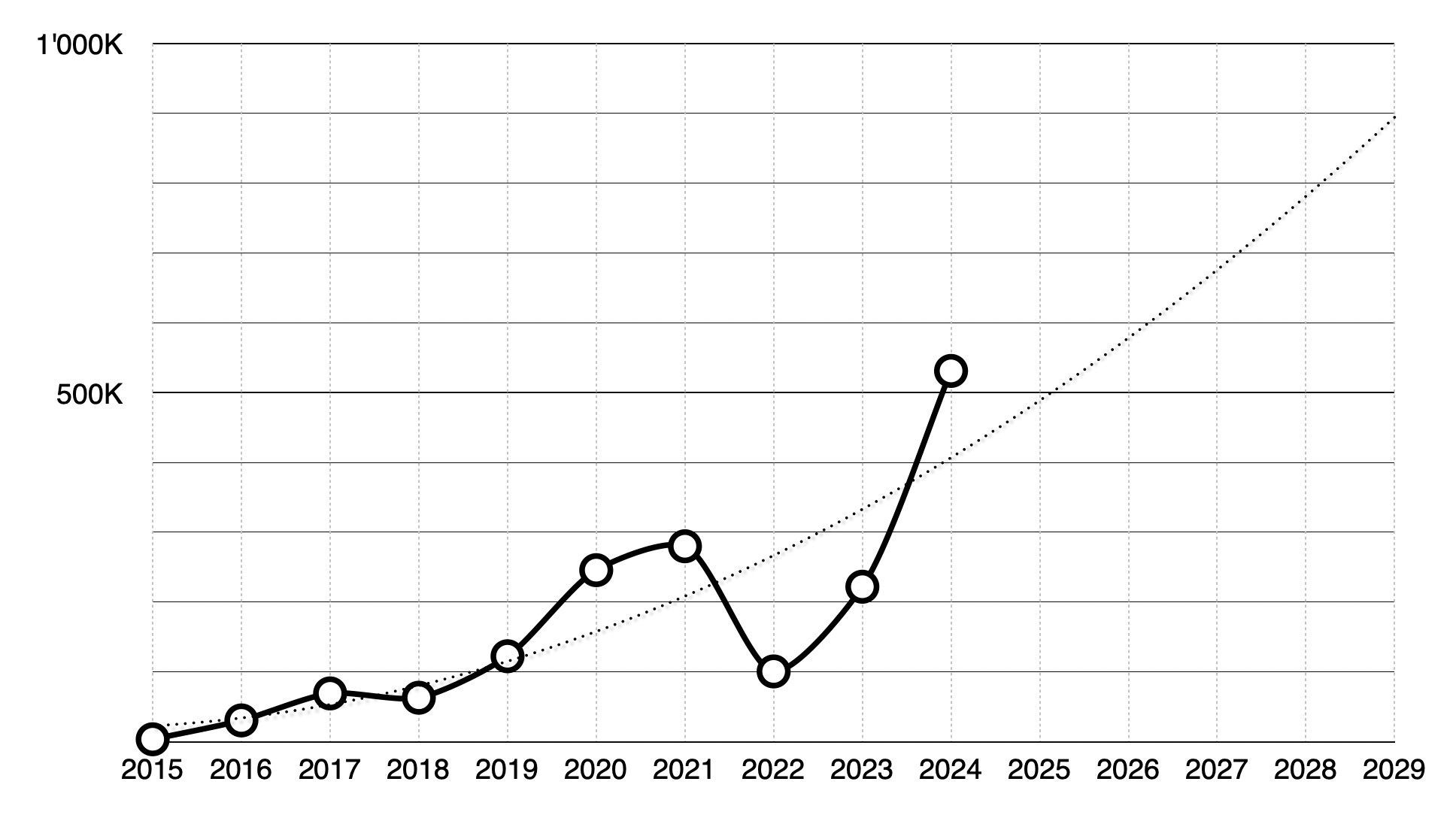

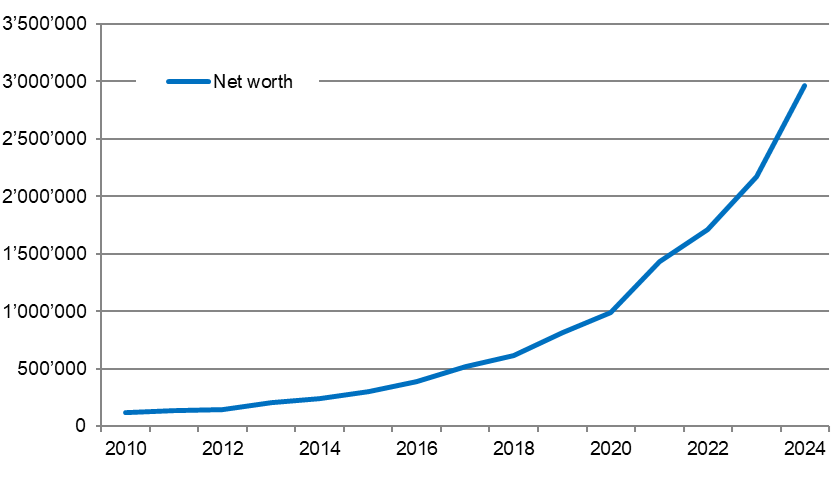

I set out to reach 500k EOY when I started investing ten years ago and thanks ot a stellar market it somehow worked out. I’ve given up on my timeline at some point after having had a terrible drop from 300k down to a low of 96k in 2021. I am equally glad and surprised to have recovered so swiftly! 80% stocks, 20% VT.

Congrats on reaching your target! When you say 80% stocks and 20% VT, do you mean 100% in equities with 80% in individual stocks? That is an impressive risk profile…

It is indeed 100% equities, but no options. With quite a long investing timeframe in mind, I am hoping I should be fine and benefit from big years like this year.

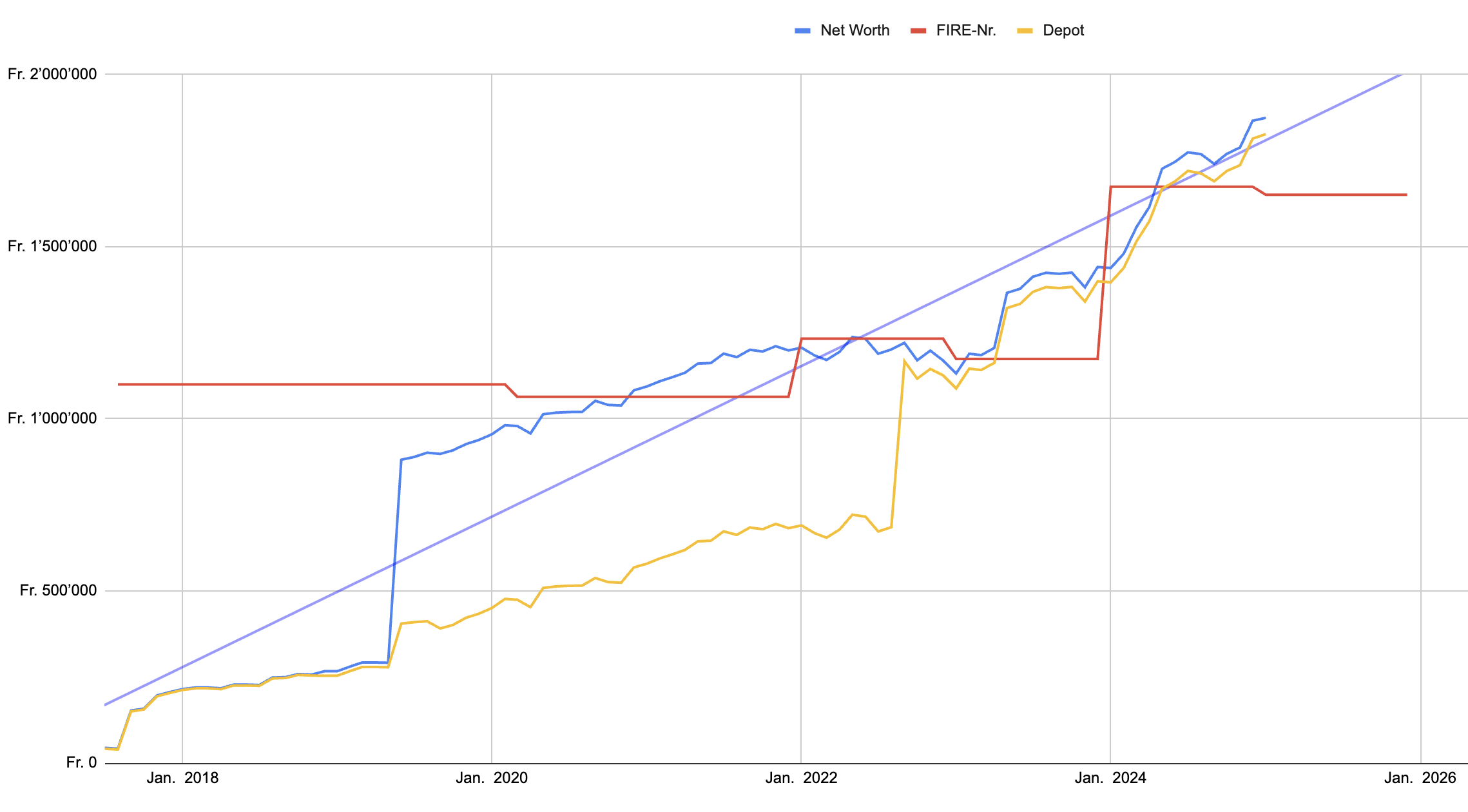

At my stage I am more forward looking than backward looking. Still, some recent and mostly* current numbers, as I have just swung onto my horse to ride into a Marlboro like Altria-dividend-paying sunset:

Just for my understanding: do you mean 80% individual stocks? I’m asking because VT is an ETF which is composed of stocks, so it could technically also be considerd stocks.

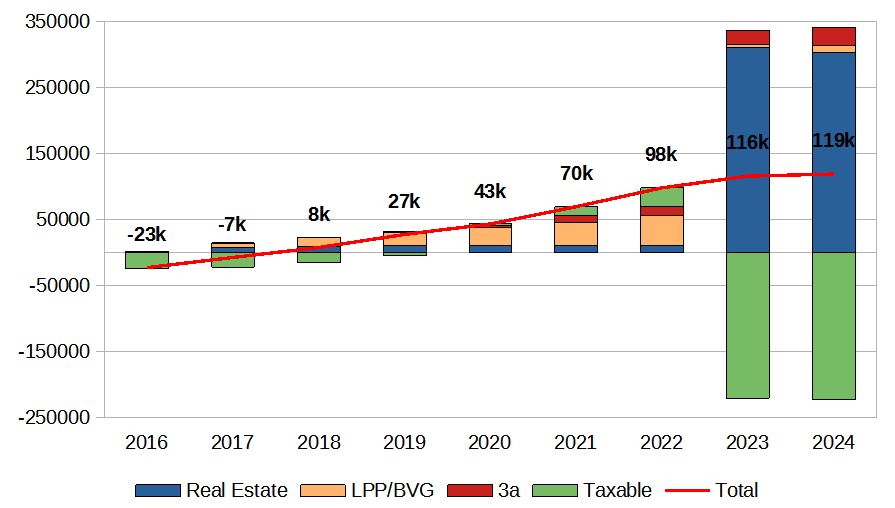

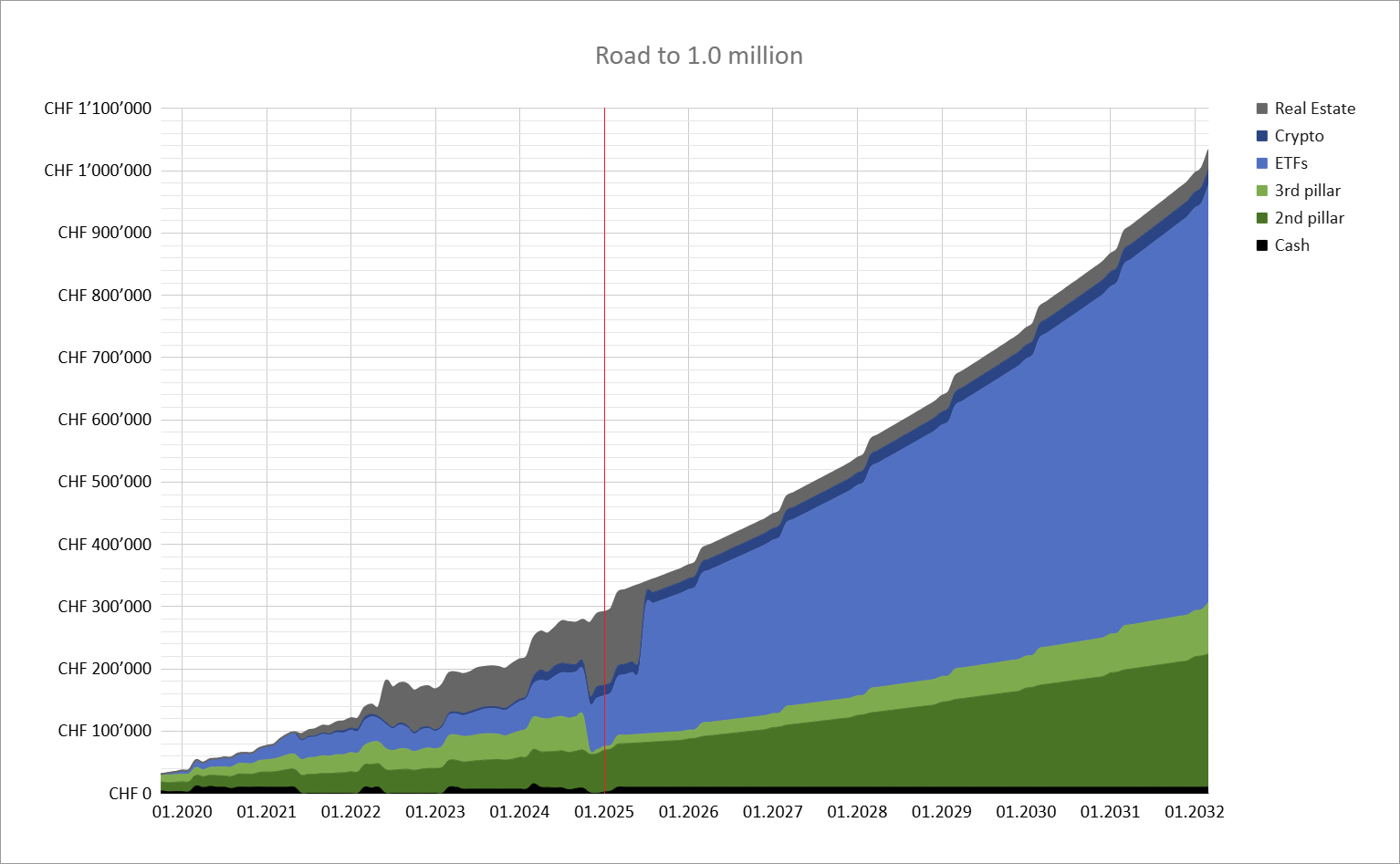

btw consider doing a stacked graph for the net worth? (it’s a bit weird to see it go up when it’s actually distributed differently between taxable assets and retirement assets)

What is your (target) asset allocation ? You indicate dividend stocks, what stocks do you target here?

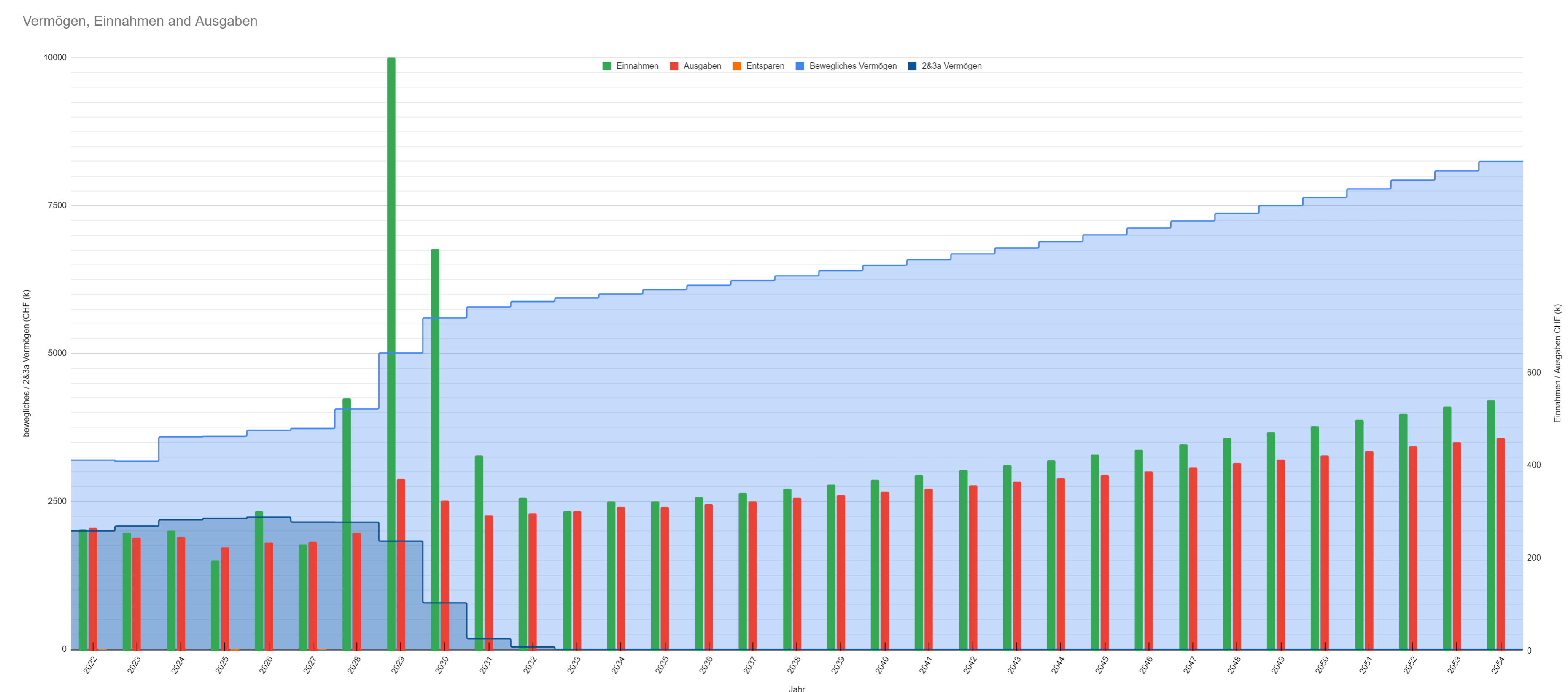

If I understand your graph you anticipate in 2033 (at full retirement?) 300k income with a 6M stache? How much is this in terms of (post tax) portfolio return vs AHV/pension?

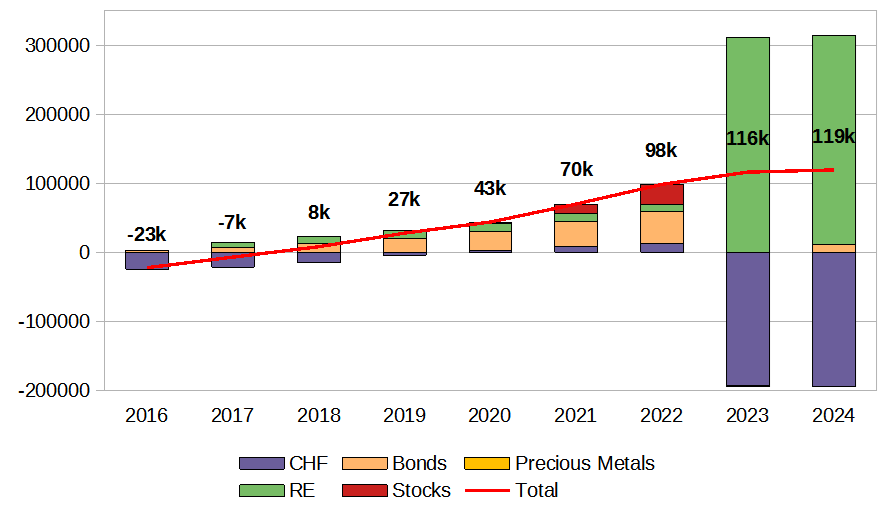

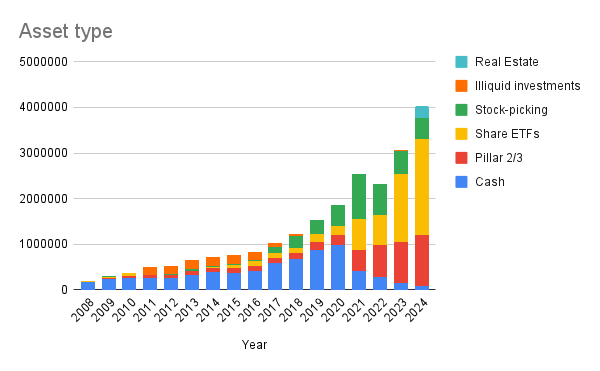

I think I mostly already am at my target allocation (for the taxable assets), which is about 3/4 the stock picked portfolio, 1/8 ex US equity (VXUS) and the rest in bonds (BND, BNDX, VDET).

The allocation doesn’t have some big return theory behind it, it’s just what I feel comfortable with and what produces the cash flow that I need as income.

For dividend (growth) stocks I try to pick those that reliably pay, and ideally keep raising their dividend. I’ve linked to my picks in this post. The topic of said post also discusses how I (and others) arrive at potential picks.

I haven’t run the numbers to compare to pension return, but I would accept a lower return on my portfolio in order to pass on an inheritance. As it stands today, the (entire taxable) portfolio returns 4.3%. When I’m eligible to withdraw capital from pillar 2 (or the Freizügigkeitsstiftungen), I’ll aim at investing with an initial 3% return, most likely into the stock picked portion of the portfolio.

I don’t know how to compare to AHV, as regardless of what I paid in I’ll get a mostly fixed amount out starting 2033.

Full retirement is hopefully earlier than 2033 … I’m reducing from 50% to 10% starting next year (tomorrow!), and depending on how comfortable I’ll feel with this setup I might dump the remaining 10% in a couple of years as well.

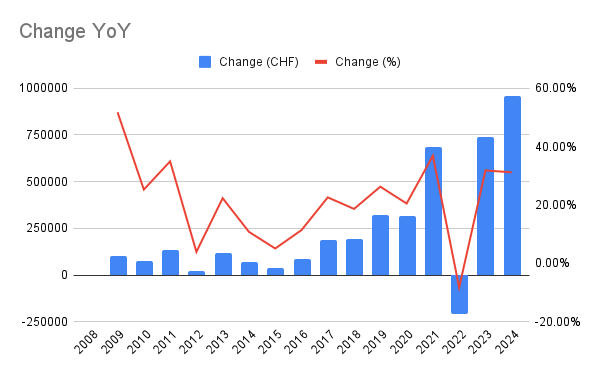

YoY sum says 17% gain in stocks and 16% in 3A, pretty damn good. Onwards and upwards.

Edit: probably not super accurate, I’d planned of doing some sort of analysis of what % did the 2023 tranche do, what did individual tranches in 2024 did etc but in the end can’t be arsed, it’s just EoY value of 2023 vs EoY 2024.

I’ll still have to deal with real estate this year so not much will be invested in stocks but things should start to normalize in 2026 if life pretends to be normal until there.

YTD 30% + 436k (approx. 150k where savings, the rest stock market performance). Had to raise my expenses due to health issues, but the performance kept me well above my FIRE-Nr. ;-):

Preliminary, that is +36% YoY, with roughly 21% asset return (with individual stock picks somewhat underperforming) plus new savings. New savings in 2024 went already more towards 1e pension fund with lower equity exposure and increasing share of uninvested cash, and I plan to repeat that in 2025 (market timing, expecting some turmoil once Trump is acting president).

Having reached my lean fire target in early 2024, and given that reaching my actual fire target in 2025 is pretty much guaranteed (unless there is a severe market crash), the main goal for 2025 is to switch to a less demanding job, at the cost of course of also exiting an extremely well paid job. Let’s see if that works out. Happy new year to everyone!

My target allocation was 66% shares, 34% other asset classes, and with at most 500k CHF in the stock-picking portfolio. I undershot the share allocation a little bit in the end (63%) to finance the down-payment for an apartment, but it’s still within acceptable tolerances.

I’m now comfortably over my FIRE target. It might become harder and harder to justify working, but I don’t have a fixed RE date set yet.

Quick explanation: In October 2024 I withdrew 50k from my 3rd pillar to reduce the mortgage (thus increase home equity). I did that because I’m in the process of selling this apartment and will use the freed-up funds to invest in ETFs in my taxable account. I’m assuming I’ll sell the apartment by June 2025.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.