Totally agree with the fact to not own a car is a massive saving cheat. Despite the fact that I would love to have my own car (probably something affordable but only to enjoying it on weekends), the costs involved and the fact that I’m lucky enough to have other mobility options (CFF 2nd Class AG and EV rental) make me think every day that it’s not worth it.

For home-related expenses, do you mean rent, insurance and furnishings?

GA would be already to expensive for my use case. Cycling to work every day, my wife commutes more (Abo Aargau-ZH), so we do not spend much on this as well. Especially we get 20% off since I have plenty of REKA (3000 CHF @80% input). I can’t understand people who commute more than 20 minutes one way. For my wife it is temporary right now, since she is looking into opening her own takeaway/catering.

I meant rent. But actually we furnished also pretty good. Most of the stuff (Except bed and wardrobe if I am right) is second hand, so no homestuff insurance needed. We have good cooking stuff, but it should last forever (just got a cast iron stuff, probably already 30y old but could look like new) for free.

Oh and I forget, basically not going out much, because mostly we cook better than most restaurants anyway. Never taking lunch out at work (left overs of previous day) and cutting down the meat helps a lot (but when we buy meat, it is quality stuff).

Normally, or credit card bill is largely under 2 kCHF every month, including business expenses.

In our case it’s mandatory as my girlfriend commute everyday (1h) and I commute 2 days per week (1h too) from our home to our employer. Also, our parents lived in different cantons so it’s also really useful. Fortunately, my girlfriend has de Duo GA and my employer contribute to 25% of the total cost. Last but not least, we live in a new eco-neighborhood which, to encourage mobility, is giving us a voucher equivalent to a year’s subscription to the region’s public transport network. This voucher can be used for the GA (so we’re saving quite a bit too).

I’m working harder on that. Since I like to cook, I always try to have leftovers for the next lunch.

Interesting! I hope our new furniture will also last forever

I’m impressed - I think I could do much better, we “only” saved 80kCHF this year but have a 100kCHF higher household income… and I agree, cars and food and “enjoying life” (the sports, vacation etc. we like) just costs a lot of money and I’m currently in a phase of life where I’m not motivated enough to cut down on this…

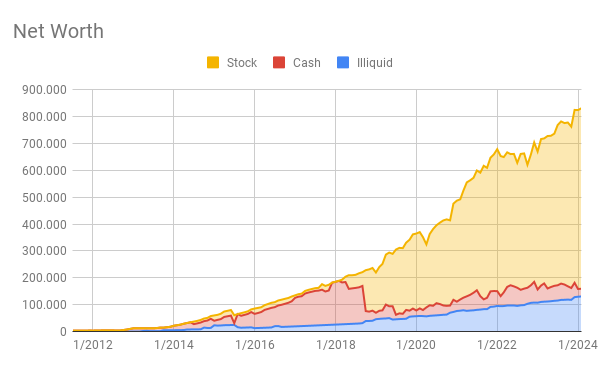

2023 has been quite a nice year, in terms of investment returns (+11%), savings rate (44%) and net worth increase (+85’000 CHF), but also in term of experiences (many weddings, a lot of travels…).

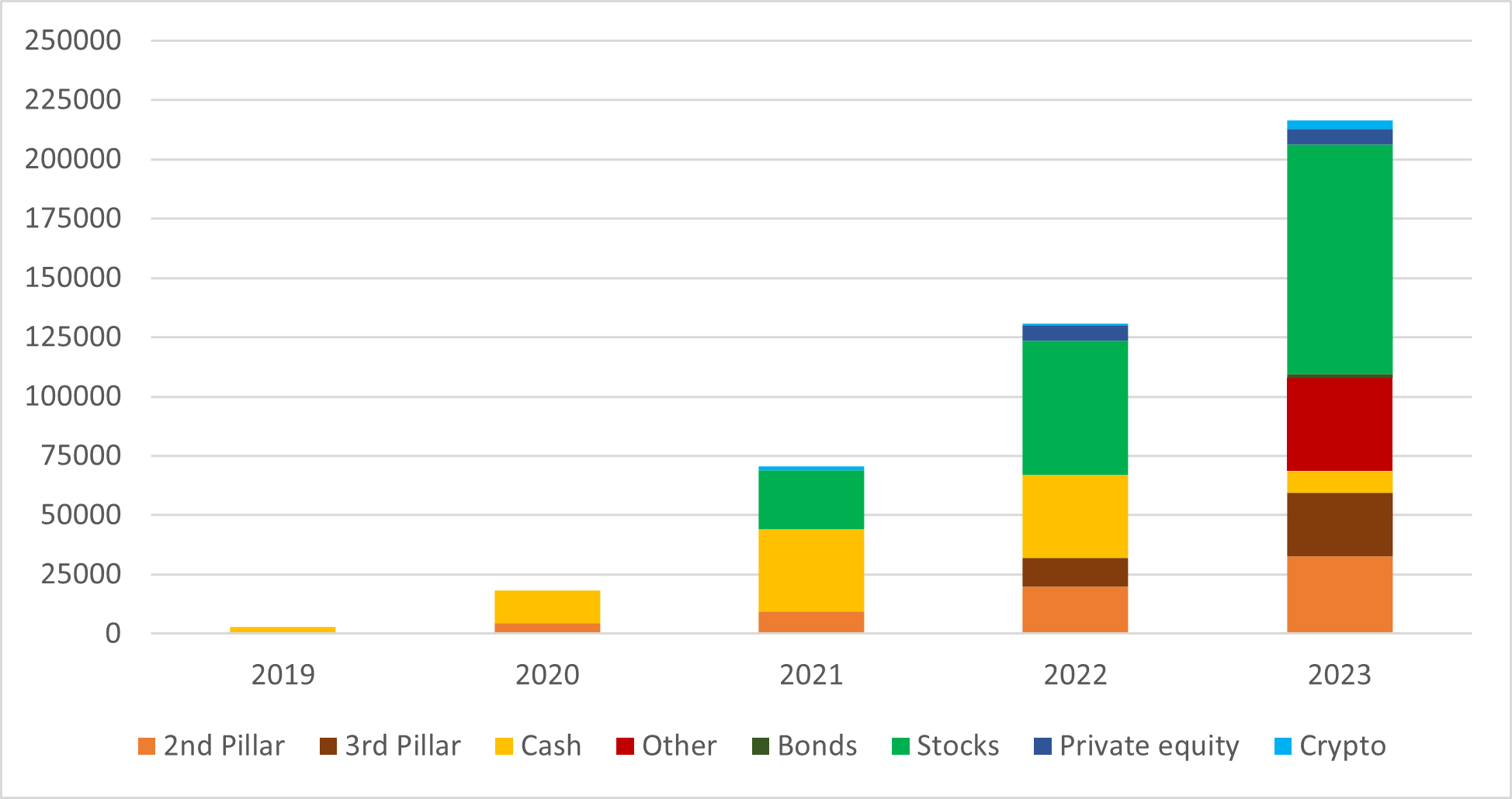

The “other” section is now mainly occupied by the paid value of a classic car, purchased in the second half of the year. Not the best mustachian decision ever made, I have to admit, but it has been a dream of me from more than a decade, and finding one in good condition at a reasonable price has been extremely difficult. Ideally, I wanted to wait a little bit more, but the occasion was too good to not be taken.

That’s my man! What a beautiful car indeed. And I think that it is more an investment than a loss, you should be able to sell it more or at least at the exact same price as purchased

Thanks.

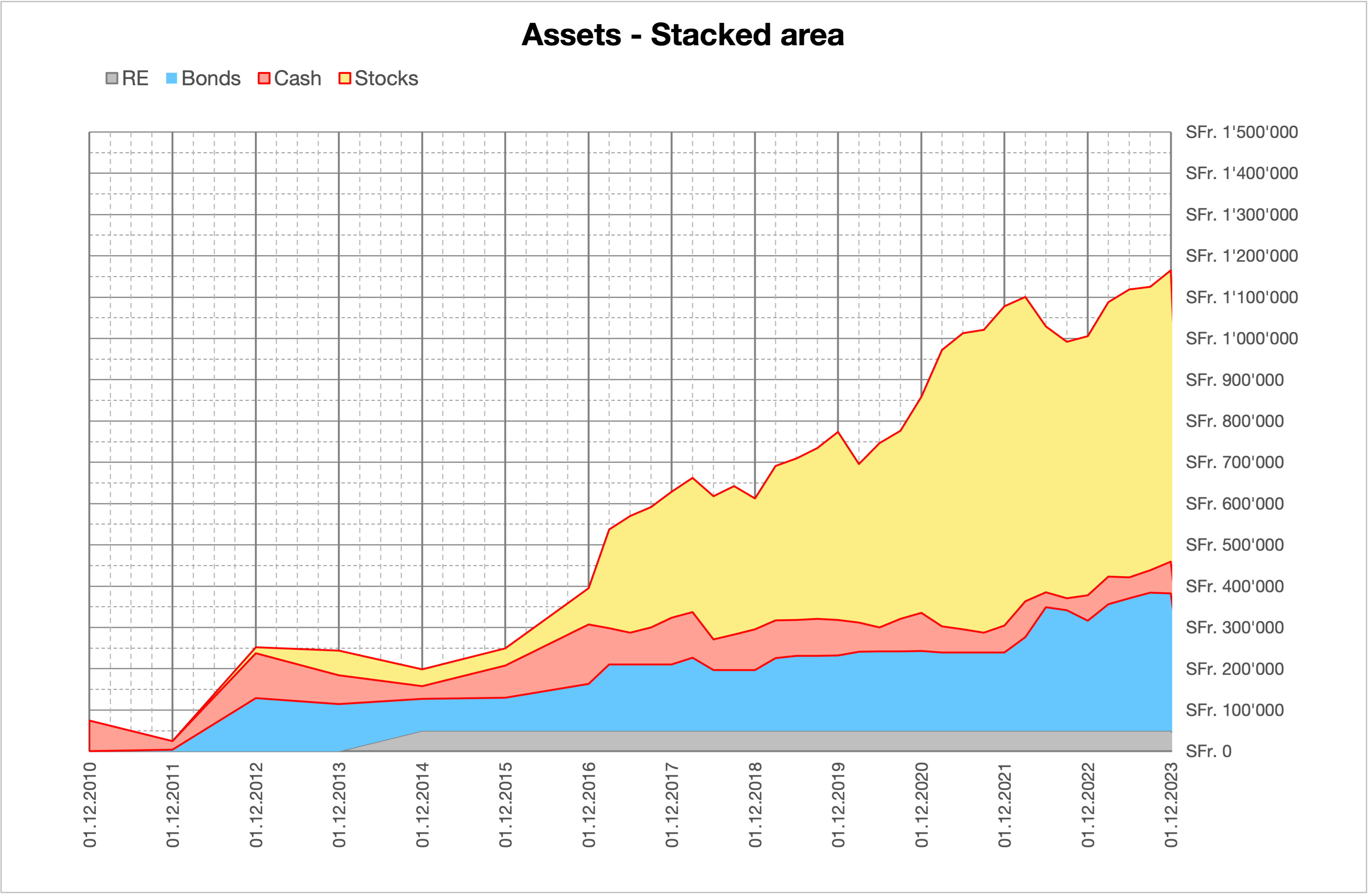

Well then I have to check in more detail my portfolio as I have a very similar allocation to yours and I’m putting on average ca. 60k / year but the growth curve of my assets is much flatter…

With “illiquid” you mean 2nd / 3rd pillar, right ?

[edit] do you have any liability (e.g. mortgage) and if so how are you tracking them ?

The flatness of the curve also depends on the ratio of portfolio value vs annual contributions. If the portfolio value is larger with the same value of contributions the curve will be flatter compared to a smaller portfolio value.

The horizontal scale in my chart might have been wider; compressing it makes the slope appear steeper. Nonetheless, my dip in the 3rd quarter of 2022 appears more substantial than yours, and the recovery seems comparatively slower. Further investigations are needed…

[edit] I have verified the values, and indeed, the growth of my stocks over the last 6 years has been lower (from approximately 300k to about 700k). It is likely attributed to a different split or the inclusion of some underperforming assets. Apart from VTI, VEA, and VWO, I also hold VWRD, acquired earlier and retained in my portfolio, along with a few other securities that might have contributed to the overall downturn in performance.

Congratulations for your achievements, by the way!

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.