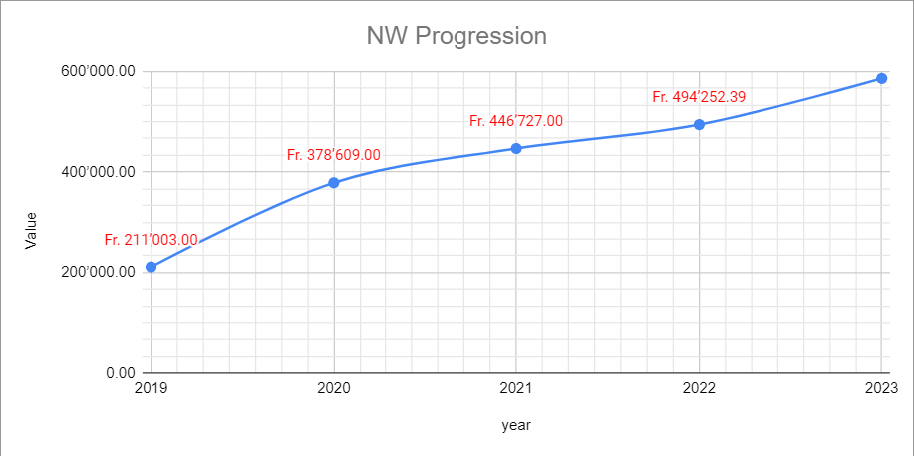

Exciting news on my net worth (NW) progression—I’m on the verge of reaching the 1 million mark in assets, and that’s truly thrilling. As of the end of 2023, my NW stood at CHF 586k. I didn’t contribute to my VIAC 3a this year, thanks to a new real estate project involving significant renovations eligible for tax deductions. My investing journey kicked off in late 2016 with my initial real estate investment, although I started officially tracking my NW in 2019.

2023 update:

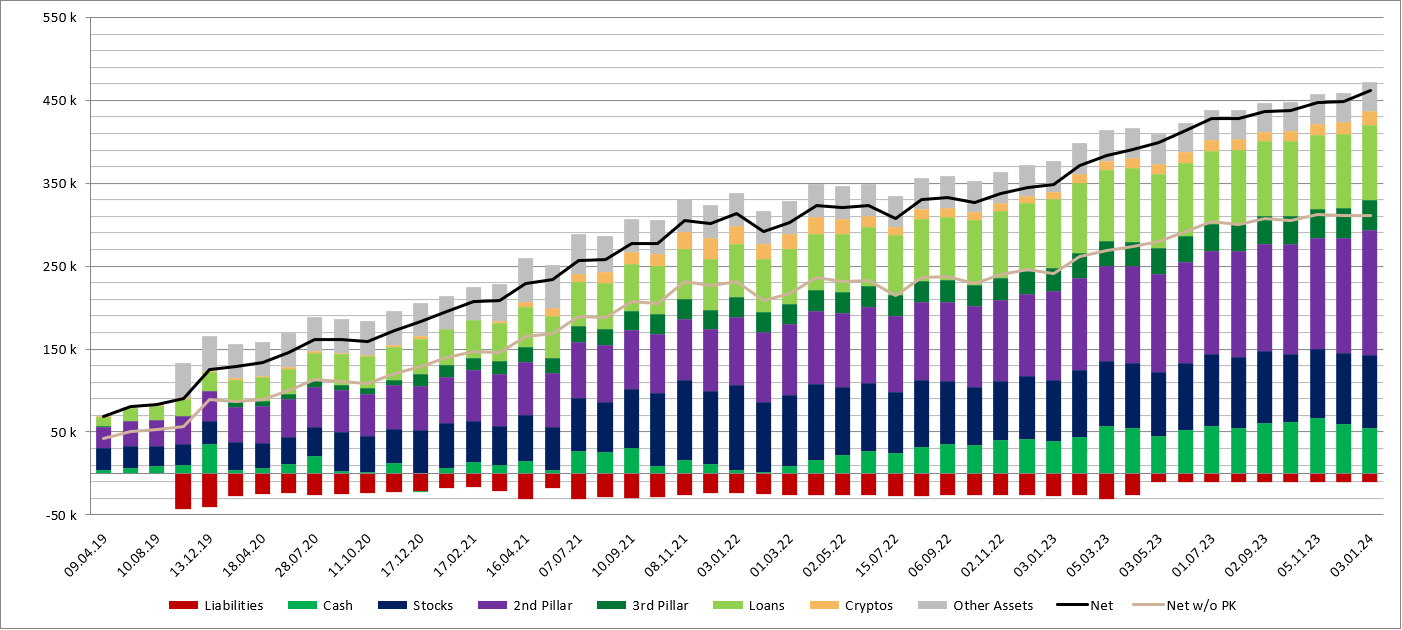

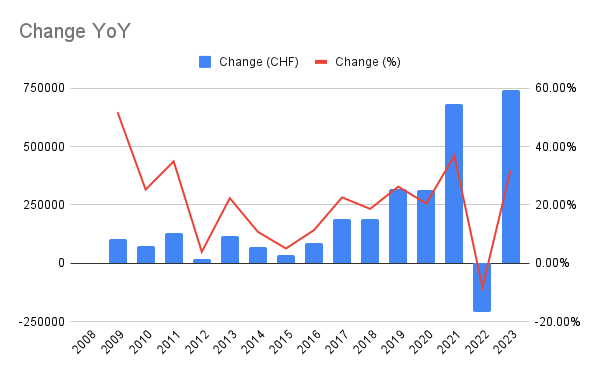

NW increased about 113k YoY to 462k (including pillar 2a, which increased 43k alone thanks to higher contributions due to age bracket and excellent returns of the fund).

ETFs/stocks at IB increased a nice 26%, cryptos 2X’ed, and a personal loan continued to pay out 3% interest. Furthermore, was able to eliminate some debt.

I expect a significant shift of asset allocation in 2024, as we bought a single family home and I will have to deposit around 200k as a down payment, hence the relatively large cash position of around 55k. Another 90k will be coming form a paid back loan and rest by selling off parts of the ETF/stock portfolio.

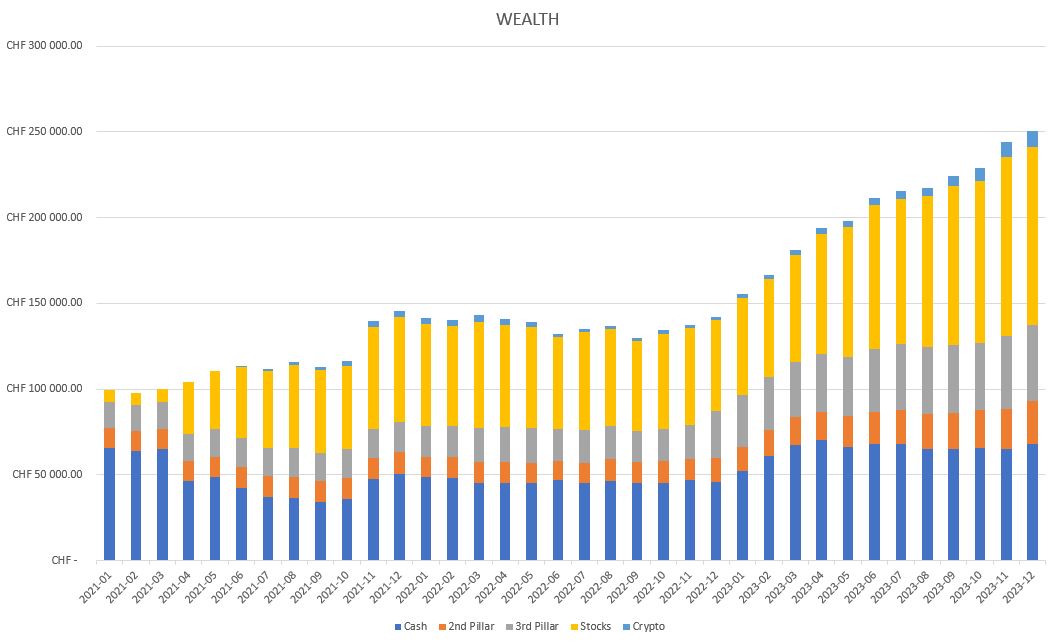

This year, my girlfriend and I started our 2 news jobs with 2 real salaries (not internship salaries). This year was very nice! We liked our news jobs and we could finally save a lot of money (75k) for the first time and invest it! Part of our saving was used to fill up our “emergency fund”:

The progression is completely different than I initially expected by end of 2020. Getting into RE (abroad and Switzerland) wasn’t planned and slowed down my investments outside of the 3rd pillar significantly. Only managed to invest another 20k in those 3 years in ETFs (6k in 2021, 0k in 2022 and 14k in 2023). It’s a shame I wasn’t able to invest more than 7k (3a) in 2022 when stock markets declined.

But now as there aren’t any investments in RE anymore and I’ll receive my last bill for my BSc degree (which cost me 30k in total) next month. I’ll be able to invest much more in ETFs. Should be able to invest 40k in ETFs and 7k in 3a from now on. So I hope to hit 1 million within the next 10 years.

What helped was an inheritance, and the starting of a civil job with a real salary in february 2022 (was living with less than 20k a year before). Well, it was mainly the inheritance.

Now that the year of not knowing what to do (2022) and the year of investment (2023) are done, I will spend next year just watching it, and I hope watching it grow.

Interesting evolution.

Can you elaborate what are the changes in real estate? Did you inherit a fully paid real estate and got a mortgage on it for investing it in stocks? Or did you had 3 smaller objects and sold 2 of them in order to invest it in stocks?

I received a fully paid real estate, as well as a lump sum. Then I took a mortgage on it to buy a second one and invest in stocks, and I invested it over a little bit of time.

The small wiggles are just down payments.

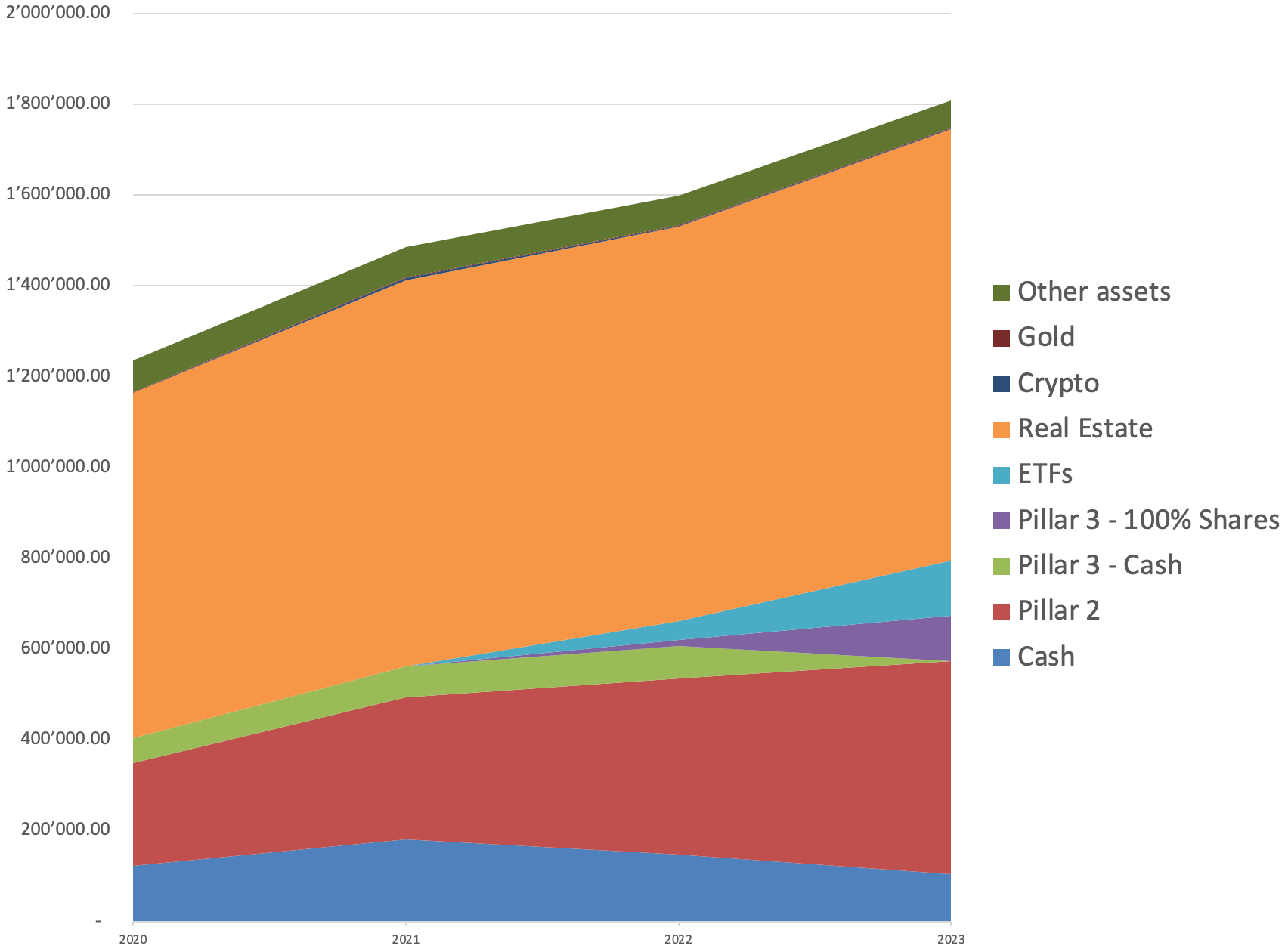

Up to 2020 my asset allocation was suboptimal (some might say insane). I’ve been fixing it since then, but in 2024 the goal is to not do any kind of rebalancing except for continuing with the extra 2nd pillar contributions, which seem worth it given how close I’m to pulling the trigger.

Your funds+ETFs have more than doubled in value last year if I understand your graph correctly. That can’t be because of rebalancing and/or increase in their value, I assume. Did you receive additional capital last year which you invested ?

I’m still working, so part of it is definitely me investing basically all of my salary into either ETFs or additional 2nd pillar contributions.

But a lot of it was just rebalancing away from the individual share portfolio, which pretty much concentrated in one company that’s had very volatile share prices from the start of the pandemic. What in the graph looks like the share portfolio stagnating in value is actually the shares going up by more than 50%, and me selling a good chunk of them to buy something more diversified.

I assume you will retire early, not in an age that allows withdrawal of 2nd pillar. What are you planning to do with it after retiring?

I also buy-in with similar amounts into 2nd pillar for tax optimization. This is well invested (1e solution) so no issue there, but I will need to buy real estate if I want to access these funds eventually.

The plan is to transfer it into a vested benefits account until official retirement age, at a provider that allows some control over how the money is invested, where it can provide a good return unlike my current 2nd pillar account

At least Finpension and VIAC have reasonable looking products in this space, which allow for a configurable equity index funds / bonds / cash split. The TER is higher than with a good ETF (~0.5% for both of them, I think), but that’s dwarfed by the initial tax savings.

This is also my plan. Until last year, I avoided contributing to my pillar 2 due to poor performance (~1%) and lack of benefit since I won’t get the nice 5%+ conversion rate as I plan to retire early, so it was a losing proposition for me.

However, now that I’m <5 years from retirement, I’m aggressively filling the pension and will shift it into both VIAC/Finpension on quitting. This will allow me to invest in stocks not too expensively and more importantly, within a tax protected wrapper where it will stay until retirement.

In an emergency, I could withdraw some to pay off mortgage.

From 2020 to 2022 I was finishing my IT apprenticeship and was making less than 20k/year on average.

On 2023 I worked 10 months and was able to save a considerable amount, also opened a 3A.

We’ll see if I’ll be able to keep the pace this coming year since I just resigned from my job

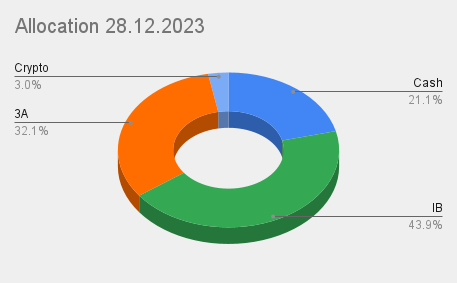

When it comes to my asset allocation, I don’t have an emergency fund. The cash portion is only there since I’ll take a trip to Japan next month and still need to pay a few things. Overall, I’m pretty happy to have attained my first 10k.

Nice job. At this stage in life, I was still heavily in student debt and even increasing in debt with my first job (living costs > income due to living in London).

I have heard many times that the first million is the hardest and I am curious how it goes further. Still far off from FIRE number. I am less pursuing RE, more FI

Excluding 2nd pillar since I am too lazy to transcribe it every month (and because I have no real control over it…).

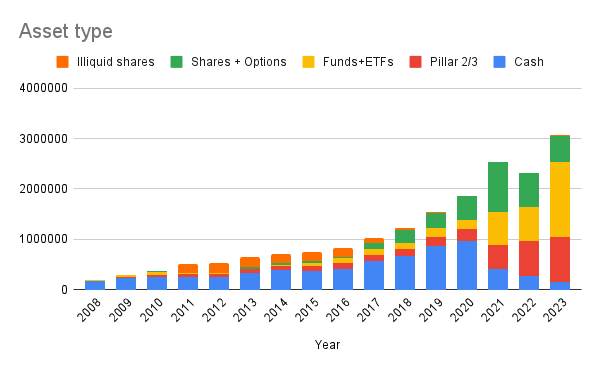

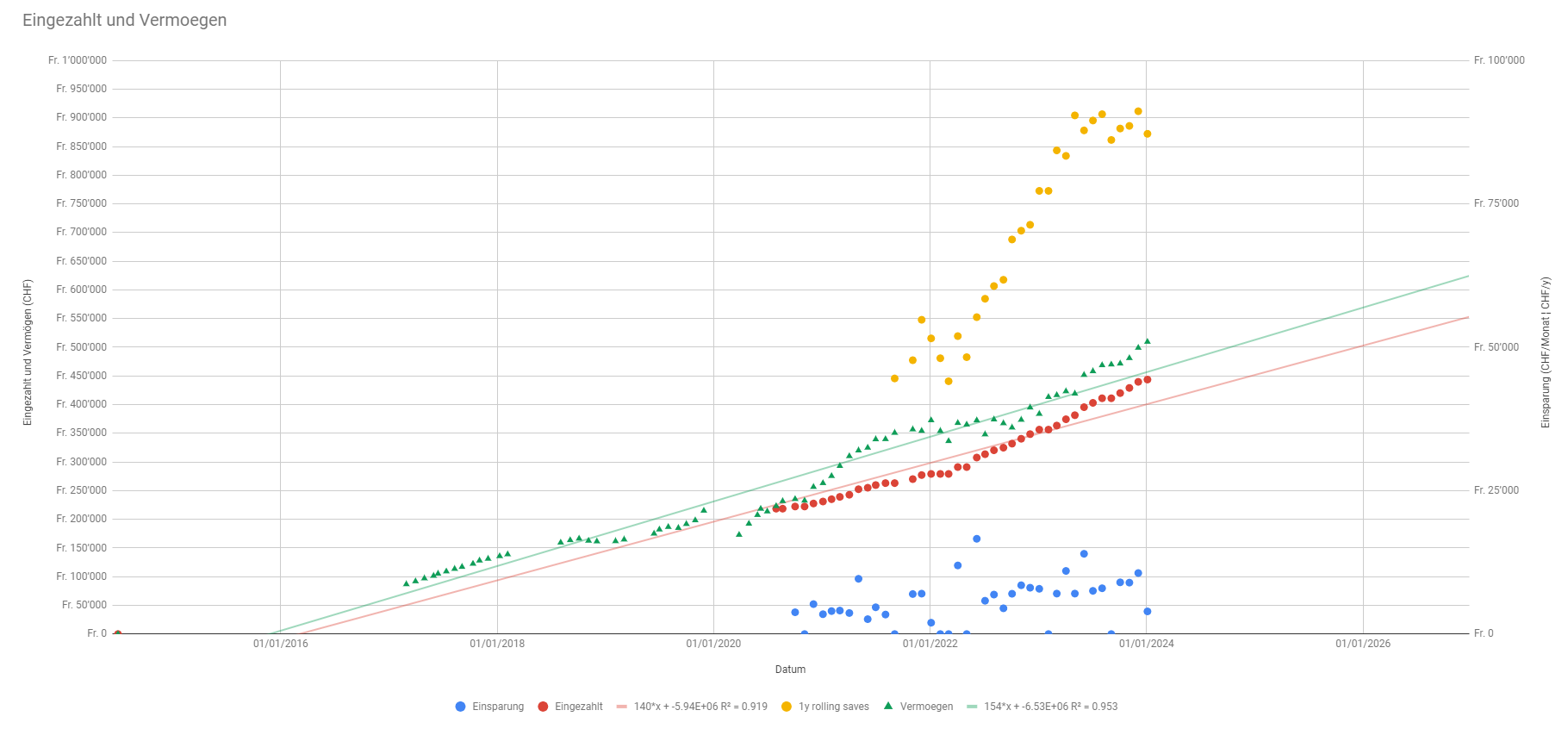

Savings have substantially increased, we hit the 500k mark, the increase is still mainly driven by inpayments (close to 90k in a year on a brutto salary of about 170k). We should hit the 100k savings next year.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.