In every crash cash is trash. I prefer to hold stocks.

But yes, if I am able to do that I will let the forum know when I reduce or add leverage. I always have debt because my accounting teacher in the 70s told me “you don’t really have done it until you have one million of debt”. I am afraid that this is many millions now…

Nice to see everyone’s strategy. To give a bit of context, I’ve been investing for a while, never sold anything so far I sticked to the plan.

I’m thinking about going a bit out of the beaten path with about 10% of my portfolio and maybe sell a little, maybe just stash the money I was gonna invest until I can enter lower (if so, good, if not, it’s only a small proportion of the total amount).

My take? If you don’t need that money, choose a benchmark then go for it. Assess your results vs your benchmark and document your journey (emotional state, happenings,…). Then revisit your journey from time to time.

Since you started the topic on a more dramatic topic title, is there a plan for that, too? I.e. selling “before the bubble bursts” and selling into what?

Please accept my apology if your question was different, but summarizing it I would say that you’re chickening out on accumulating into VT and you’re looking into potentially diversifying 10-20% of your (VT) allocation into “something else”?

Totally legit question, just want to make sure I get the question.

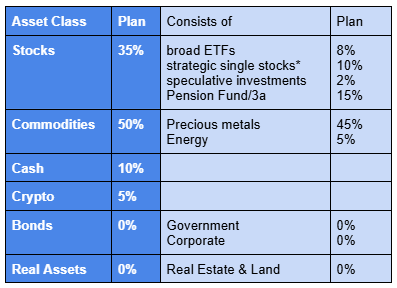

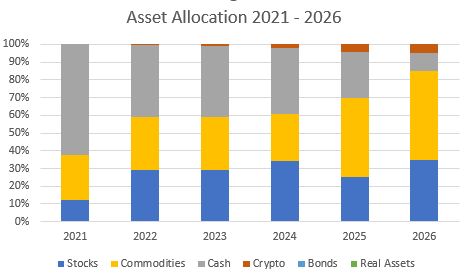

Rather than selling something now, I’ve been thinking about my asset allocation for 2026. I’ve been doing this since 2021, therefore I am already somewhat in the target zone. With plenty of dry powder (precious metal and cash) to adjust to whatever scenario. Any thoughts?

I don’t have a crystal ball and I hope a major meltdown will be less severe with my asset allocation. Given the increasingly belligerent tones in several countries and the continuation of money printing and increasing debt burden in major economic areas, I see a some signs of a severe storm. As I am near the end of my career, it has become more important to me to protect my assets (stocks and cash) from crashes and inflation than to participate fully in growth events.

I expect people will shelter from inflation in CHF as a currency. Nationalbank does not really like too much money flowing into Switzerland

When the going gets tough, energy stocks are able to continue perfoming as energy prices as everyone needs energy and prices will be adjusted

Precious metals have been the safe heaven assets across millenia, I don’t expect any changes this century.

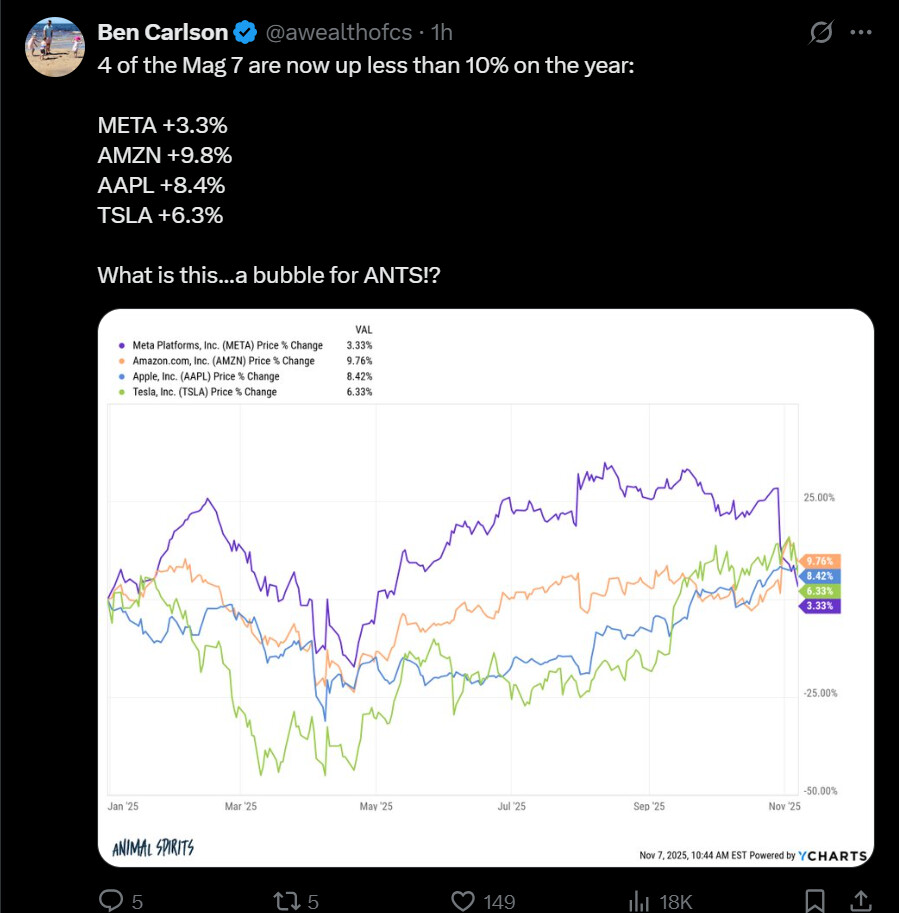

It is funny though that silver and platinum have performed exceptionally well alongside gold this year. Not something I had anticipated or positioned for.

In line with what @Your_Full_Name has mention before - if you’re uncomfortable piling even more money into VT-and-chill, then what would happen if you reworked your strategy and reduced your regular contribution until we reach a better (lower) valuation levels? So you can ride the wave upwards with the current stash and only add significantly more when we go down (like you add 100+2*(), –> a 20% drop would make you add 140% of your regular monthly contribution, a 50% drop would double your investments, a -20% “drop” (20% raise) would make you only pay in 60%.

Trying to catch the tops and bottoms will probably not work consistently.

“normal” commodities (as in: raw materials, agriculture, oil, mining) are super volatile and they also tend to go down in crises, but gold is inversely correlated with stocks in a crash (as safe haven).

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.