Do you own Venezuelan assets or assets in Greenland? Then what’s to worry about?

3 Likes

Economic sanctions from the US vs Europe in the context of them wanting to annex Greenland and the freezing of US assets by the US (equities/bonds) + assets held by US banks and brokers. With Switzerland being potentially seen as a way for EU countries to bypass the sanctions and being caught in the fire.

I’ve considered the US as a bully state for some time. I think @Helix presents a good enough generic solution that works for most situations here (it can be applied whether we feel there is a threat or not, no matter from where the perceived threat may come): How to protect assets from international disruption

1 Like

US Nightwatch plane is flying for example. Maybe it is a crazy Ivan move. But I find it difficult to distinguish strategically 5d chess “crazy” from just crazy. First time I decided to ride this one out. I decided that my peace of mind is worth the opportunity price.

My worries are not about the Venezuelan or Greenland assets. Not even aboit the value over underlying stocks.

My worry is sanctions from Europe to US or otherwise. All my investments are in US stocks/ETFs, I think worry to lose them (like happen to people investing in Russia) is a real concern, imho.

Then split your holdings.

US etfs for US assets.

european ucits etfs for ex-US assets

A bit of a home bias helps here as well, swiss etf on swiss stocks/assets.

Reduce the US weighting a bit as well.

Nothing of this will seriously alter returns going forward, but already helps a ton against expropriation risks.

4 Likes

YTD 7.03% in my momentum strategy after 6 trading days, >85% U.S.

Do you really believe that any event will make stocks worth less and will not make money worth less? Why people after that many years of central banks still do not believe that cash is just another position, and a very risky one, manipulated by politicians and with a state guarantee to lose value.

I know this situation, had that many times in my life. But anything can happen anyway anytime. That is the beauty of it, nobody knows in advance. But logic tells me that real value like stocks are worth more than a promise and money is nothing but a promise.

And then again: I am very bad in timing tops. However, I am quite good in calling bottoms, that is where I made most of my money. It is when your whole body and soul tells you not to buy, pressing the “buy” button physically hurts. That is when I buy. On credit, so it hurts even more.

Now, when to sell? As late as possible… but not later. For me that means I never ever sell anything without a plan to reinvest the money, usually in stocks.

1 Like

A few words to asset allocation: if you do it do it right!

In literature you are required to hold many different assets like real estate, gold, stocks, bonds, currencies, art and so on. That really reduces the risk, one thing goes up, the other goes down. But then, probably you won’t make much more than inflation…

In practice, which of those assets did gain the most long term? Stocks of course.

A friend of mine had a really really good hit by timing the Nasdaq. He invests only in ETF. I could prove to him that a simple allocation of all his ETF would have given almost the same performance, even he was very lucky the last few times he bought and sold the Nasdaq (which was pure luck anyhow, the timing came from external influences).

I could show him that a predefined allocation of his ETF with reallocation every 6 months did almost as good as he did. Without having to guess tops or bottoms. And being invested a 100% in stocks all the time.

Anyhow, if you feel you are better off with cash, you still should have a plan. When do you sell how much of what, when do you re-enter the market and so on. Otherwise you are almost sure to lose money.

Do you have a literature citation for that? Sure 60/40 is controversial in today’s regime but not making more than inflation?

1 Like

OK, that was probably just a mathematical assumption: if you invest in everything except cash you will make exactly the inflation of everything.

But then if you use clever reallocation strategies you will hopefully make more. Shannons demon, you can gain even if all assets you reallocate lose.

Those reallocation systems are mechanical and I love mechanical strategies. I could even live with cash in such a strategy. Because you automatically buy low and sell high. The key point being “automatically”. If you have to decide on a case-to-case base you put yourself out for pure luck.

You cannot invest in everything else, not close.

One can reasonably expect 4-5% real return for global stocks and about 0-1% real return for global bonds, over the longterm.

In a 60/40 and going with the lower threshhold and no rebalancing would mean 2.4% real return. Upper bound 3.4%.

And with Shannons demon and rebalancing as you say, this will get bumped up some more.

I thnk you can reasonably expect a 3-4% real return still with a global 60/40.

Bond rates are a bit higher again, which help expected return, while stock valuations are on the high end of course currently. Should balance out relatively.

1 Like

I wonder if by “inflation of everything” what was meant was “you’re not generating alpha”?

(at least for me the goal is not to generate alpha, market returns are fine)

In a way we are always generating alpha. Someone knowing nothing won’t manage to reach the market before being picked off by banks or, worse, scamers.

Then you can trivially beat the stock market with low amounts of leverage by also accepting more problems (e.g. volatility, complexity).

Of course, from the outside this can be explained by simple betas. But why is one allocation chosen over the other? Why do some people hold all in cash over decades? That is because they don’t know or can’t.

Of course, this was just a mathematic/statistic thing, an average if you want.

Interesting point. The problem is how to measure market returns and risk adjusted market returns. The “average” is a very strange concept that is often used to make shine the own performance. I fall for the same, compare my returns with the U.S. indices, what makes no sense because I have a completely different risk profile.

No, leverage alone does not beat anything. It rises volatility, that is all.

Because most people lose money in the stock market. So the loss of cash value is the lesser evil.

1 Like

That is provably wrong. A diversified leveraged portfolio can beat pure stocks in every metric.

But that is not the main critique. Your claim is like saying that stocks can’t beat cash, just raising volatility. This too is provably wrong, as over longer intervals stocks have always beaten cash.

Of course, theoretically something else could happen, but now we are in the domain of risks where many unexpected things could happen instead (e.g. hyperinflation).

The same is true for low leverage. For large enough intervals it will beat unleveraged.

2 Likes

Yes, I am the living proof of that, since 6 years. But the point is in alpha, not leverage. Leverage rises risk and performance, what translates to more volatility. If you have positive alpha that means more gains, if not more losses.

But again, leverage alone does nothing but rise volatility. You gain more or you lose more, that is all. Provably whatever, but again:

If you use leverage like I do you have to know exactly what you do. Because it can bring you more of everything, more losses, more risk, more performance.

That is true only if volatility was not too big (it may wipe you off) and the expected long term return is positive. Which it is for stocks…

1 Like

Of course it only applies to sensible implementation. Luckily they are not difficult to identify.

No, you don’t. You always won more, there was no loss. How much more as calculated in cash was “volatile” (if you measure the volatility of long-term intervals). To say it only rises volatility is not true.

Volatility isn’t even an important metric here. Having 1000 and given the choice between:

- Investment A: Low volatilty, gives you between 800 and 0 real (should be -450)

- Investment B: High volatility, gives you between 800 and 29000 real

If you are not constrained by your own inabilities, you will choose B. It is strictly better. Volatility does not matter.

And that brings me to my intial main point. There can be many reasons why an investor can not get more retuen than they get. They could just be not smart enough to beat classical market beta with stock trades. Or they might not be smart enough to see that someone is scamming them. Or they are irrationality or rationally afraid of volatility along the way.

Regardless, their underperformance relative to what could be optimally expected is their inability to do so. If we reasonably define our benchmark as the average investors return, that looks a lot like alpha.

2 Likes

Where can I subscribe to this incredible service?

Seems like a no brainer.

2 Likes

I know you are joking, but just a bit of diversification with a bit of cheap leverage will be enough. I, of course, can’t say where it actually stops, but there are clearly superior portfolios reachable with leverage.

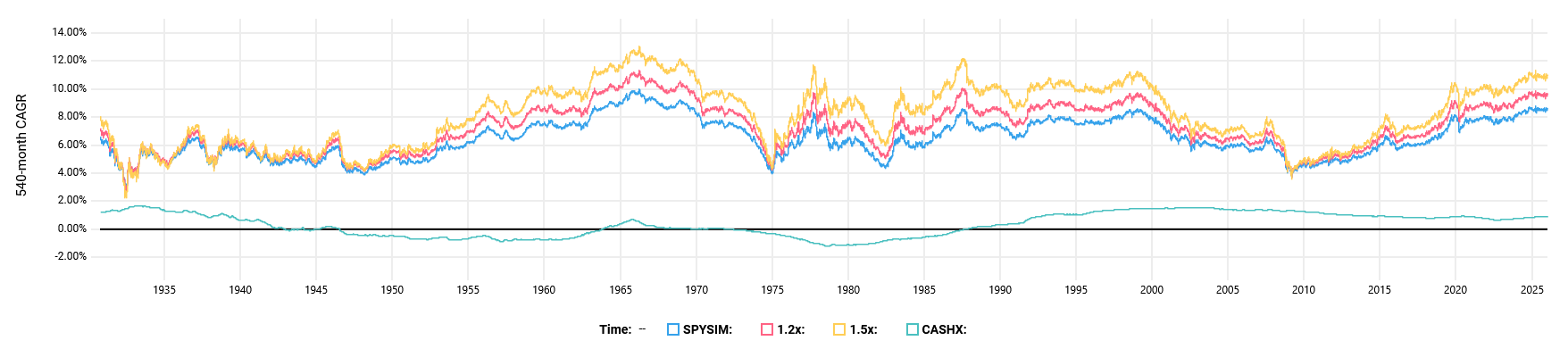

I don’t have the data for diversified ready, but here is a simulation of US large cap rolling 45y real return (vs cash). Leverage excess financing is at 0.5% on simulated USD, rebalanced daily. (Source: Testfolio)

For 1.5x there are still some actual drawbacks if you must liquidate in the biggest pits of the great depression (1 year, about 0.5% less CAGR for the 45y periods). Then a light cross in GFC. 1.2x only crosses lightly during the great depression.

Now, I acknowledge that 45y is relatively large compared to the data, but we must remember that 1.0x also needs about 30y windows to always beat cash.

If you can make a rule against liquidating everything in the harshest of all drawdowns, that starts looking much better.

1 Like

No. Volatility is the one thing that matters most when using leverage. As I said, it may wipe you out or have the broker selling your stocks in the worst possible moment.

Leverage is part of my money management which is part of my mechanical strategies. It is checked every second of every day to avoid even coming close to the allowed margin.

2 Likes