Yes, I am the living proof of that, since 6 years. But the point is in alpha, not leverage. Leverage rises risk and performance, what translates to more volatility. If you have positive alpha that means more gains, if not more losses.

But again, leverage alone does nothing but rise volatility. You gain more or you lose more, that is all. Provably whatever, but again:

If you use leverage like I do you have to know exactly what you do. Because it can bring you more of everything, more losses, more risk, more performance.

That is true only if volatility was not too big (it may wipe you off) and the expected long term return is positive. Which it is for stocks…

Of course it only applies to sensible implementation. Luckily they are not difficult to identify.

No, you don’t. You always won more, there was no loss. How much more as calculated in cash was “volatile” (if you measure the volatility of long-term intervals). To say it only rises volatility is not true.

Volatility isn’t even an important metric here. Having 1000 and given the choice between:

Investment A: Low volatilty, gives you between 800 and 0 real (should be -450)

Investment B: High volatility, gives you between 800 and 29000 real

If you are not constrained by your own inabilities, you will choose B. It is strictly better. Volatility does not matter.

And that brings me to my intial main point. There can be many reasons why an investor can not get more retuen than they get. They could just be not smart enough to beat classical market beta with stock trades. Or they might not be smart enough to see that someone is scamming them. Or they are irrationality or rationally afraid of volatility along the way.

Regardless, their underperformance relative to what could be optimally expected is their inability to do so. If we reasonably define our benchmark as the average investors return, that looks a lot like alpha.

I know you are joking, but just a bit of diversification with a bit of cheap leverage will be enough. I, of course, can’t say where it actually stops, but there are clearly superior portfolios reachable with leverage.

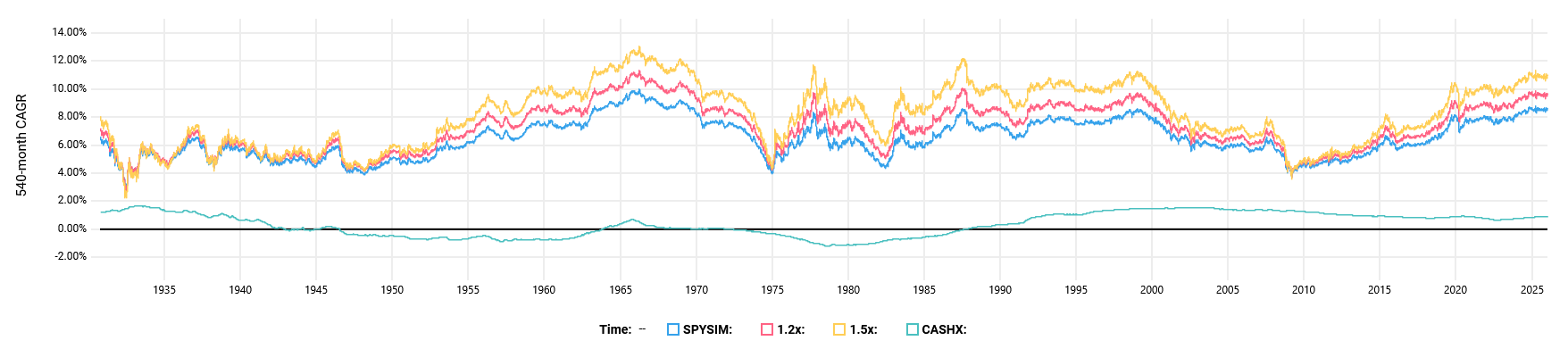

I don’t have the data for diversified ready, but here is a simulation of US large cap rolling 45y real return (vs cash). Leverage excess financing is at 0.5% on simulated USD, rebalanced daily. (Source: Testfolio)

For 1.5x there are still some actual drawbacks if you must liquidate in the biggest pits of the great depression (1 year, about 0.5% less CAGR for the 45y periods). Then a light cross in GFC. 1.2x only crosses lightly during the great depression.

Now, I acknowledge that 45y is relatively large compared to the data, but we must remember that 1.0x also needs about 30y windows to always beat cash.

If you can make a rule against liquidating everything in the harshest of all drawdowns, that starts looking much better.

No. Volatility is the one thing that matters most when using leverage. As I said, it may wipe you out or have the broker selling your stocks in the worst possible moment.

Leverage is part of my money management which is part of my mechanical strategies. It is checked every second of every day to avoid even coming close to the allowed margin.

(Actually, your broker will happily sell your shares even if you don’t respond to a margin call. Both the warnings and the actual selling are automated. It’s just simple risk management by your broker/custodian.)

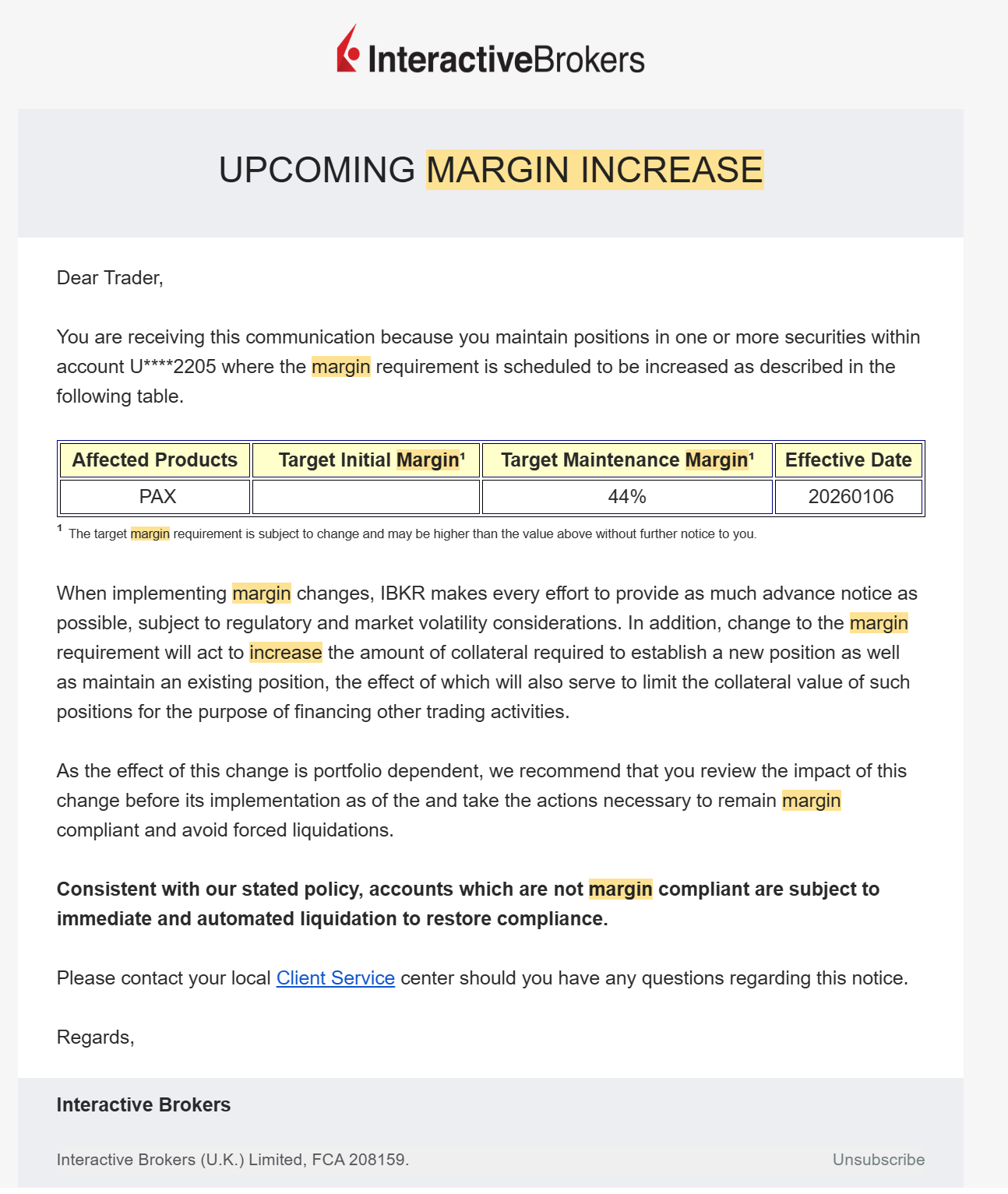

I get notifications[$] about margin increases for (some) stocks I hold at IB, but I guess that’s technically not a margin call (and since I don’t have any leverage, I don’t understand why they even send me these notices – I guess I could unsubscribe from them).

It is just an implementation detail. What matters are outcomes. And I think, I have shown to a sufficient degree, what those are.

Of course, you can mismanage your portfolio. Stock picking a scamer’s reccomendations vs. your local bank’s fund vs. a Vanguard one also has consequences.

Also, there are instruments that don’t suffer from liquidation. And at low leverage factors, even highly sporadic management won’t end in margin calls.

0.5% excess financing for leverage seems particularily low to me knowing we are talking USD. Especially if CASHX (3 months T-Bills) manages to roughly match inflation on rolling 45 year periods (meaning interest on those bills was more than 0.5% at the very least).

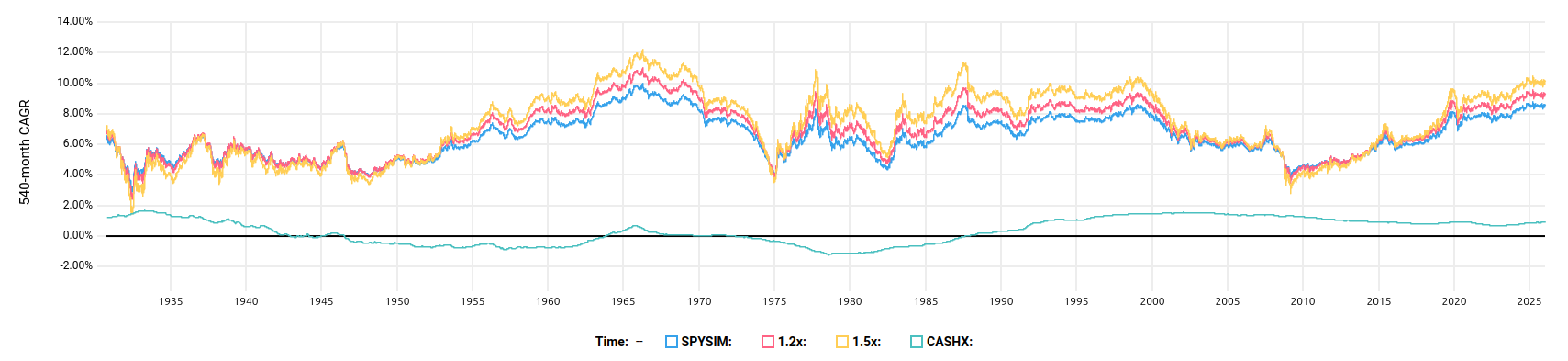

Putting the financing rate at 2% gives some rolling periods where leveraged portfolios have worse returns than the unlevered one (which is not what one would expect when taking leverage. More risk, yes. Less returns over 45 years?).

Of course, we could assume that, going forward, short term interest rates in the US are going to be near 0% and inflation low but that wouldn’t be my personal assumption.

I may have misunderstood your approach, in which case, I’m happy to be corrected.

I tend to quickly and dirtily use inflation adjusted returns in USD to simulate returns in CHF with low inflation, I don’t know if that’s what you have done here since your data is in inflation adjusted USD.

I’m not sure how testfol.io calculates it but I doubt that when forcing a specific rate for the financing, that rate is also inflation adjusted. To my understanding, your simulation assumes 0.5% cost for USD cash every year of the 45 years period for all rolling periods.

That would not have been true. Rates would have been higher with higher inflation as lenders would have wanted more returns to compensate for it. By comparing nominal (without inflation adjustments) and real (inflation adjusted) rolling returns for CASHX, at a very quick glance (I’ve only taken the first year, 1980 and 2025), YoY inflation during those periods has been between 1.6% and 3.9%. I doubt lending rates in USD have gone far under those values.

At the very least, 3 months TBills managed to give interests close to inflation since their rolling returns oscillate near 0% in the inflation adjusted chart (between -1.16% and 1.69%, actually). I’d expect lenders to want to make at least as much money with an investor as they would lending money to the government.

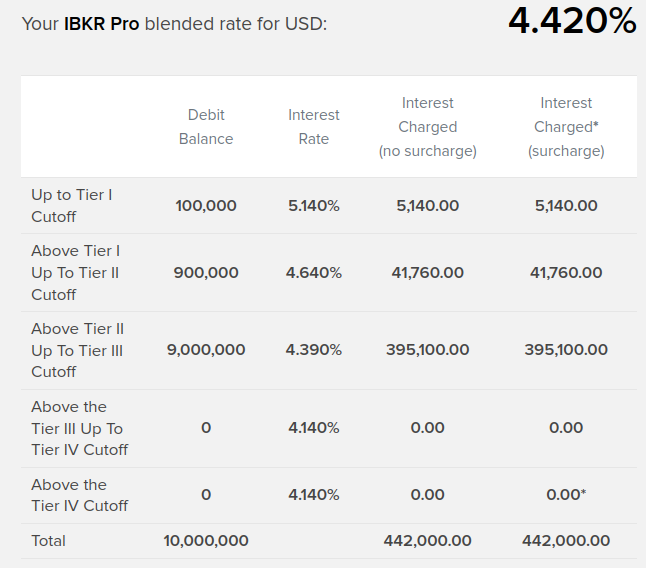

IBKR is benchmark (the short term rate) + 1.5% excess up to 100K, + 1% for everything above that and + 0.75% above 1 million and + 0.5% for an obscene amount no one here will ever have.

Box spreads will easily get you below 0.5% excess.

Ah, I see the problem. Excess financing rate is not the same as financing rate. In my simulation, I borrow the total return of USD cash-like securities (e.g. CASHX), then I add an excess financing rate to that position (e.g. 0.5%).

To see IBKR rates, frst you can scroll down on their Margin & Financing Rates page. They have a huge list containig all rates for all currencies and amounts you can borrow from them. Per currency there is a benchmark rate (BM) plus their spread.

Now, their BM does not strictly follow any other index (e.g. ultra-short-term treasuries). You can see how they are calculated at “Methodology for determining effective rates”. But basically it is anchored to an external market rate, capped above and below. And that cap is ±0% from the “Fed Funds Effective (Overnight Rate)” for USD at the moment.

The same BM is used in other interactions with IBKR. It is the same for giving them money, or short-selling. BM plus or minus some defined spread.

Do you think it would be a good idea to buy the ‘‘SGOV’’ (0-3 Month Treasury Bond) ETF ? I have US dollars in IBKR that I don’t want to invest in stocks at the moment.

SGOV is cash and cash is trash. The only investment with a state guarantee to lose value. In fact money is just a promise and when political circumstances change (like right now) this promise may become worthless.

I prefer (and that sounds very stupid) to lose 50% on stocks of good companies because I own something real. And last time I lost 50% I made 400% afterwards.

This said, I prefer the Dollar to get stronger, as my debt is in CHF. I don’t look for tops or bottoms, but maybe I did hit the bottom when buying Dollars…

From my point of view, it’s awful not to have a minimum amount of cash to seize opportunities. And I wonder if that minimum amount of cash is better invested in SGOV than just in a simple IBKR account.

“When the cannons sound you have to buy stocks” < “it’s when blood flows in the street that opportunities arise”.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.