Follow-up from another thread. Found an older thread which was last edited from 2019 which kind of discusses the topic but not all of it.

As hinted in another thread I will execute a modified buy-borrow-die strategy as this is tax efficient even if there are no capital gains taxes because you can deduct the debt and interest.

I target fatFIRE with 100% equities and after RE to live on margin loans from IBKR or a pledged asset line from my local bank, depends on what is cheaper and more flexible.

What is your retirement portfolio strategy after RE when living mostly from your wealth?

Yes I know. Everyone who holds accumulating funds can see it when filing taxes that you still pay income tax on dividends.

After rethinking the only difference is that I don’t have to manually reinvest the dividend with optional currency conversion. I don’t want the dividend to pay down my margin loan but to stay invested and keep earning me money and hopefully outpace the growth of my margin loan.

If I choose VWRL the dividend will just pay down my margin loan (which I don’t want) but I can obviously buy shares with the difference but this incurs trading fees so in the end I should be slightly cheaper and, which is more important for me, much more “automated” than with a distributing fund.

Well, definitely sounds very risky to me. I think big ERN was doing some simulations about margin lending instead of selling securities.

But there is something in the idea to invest in accumulating funds and take margin loan instead of selling during the downturns. However I would rather repay the loan when we are at a new maximum.

You obvously need to be in control of your margin yes but that is essentially what all wealthy people are doing. You might have heard from the buy-borrow-die strategy.

You do you but that sounds like market timing to me (I don’t want to spark a discussion about that though as this has been discussed in lengths in this forum already)

The reason of the buy-borrow-die strategy in countries like the US is to not pay taxes on capital gains. Their heirs will actually sell some of the assets to pay back the loan

For the past decade it has been a free lunch for wealthy people to borrow at 1% to invest in equities. So there are a lot of people talking about this strategy online

The decision becomes less clear if interest rates go to 4% or above

I have retired last year and that’s exactly what I am doing. I borrow currently at 3% in CHF/EUR, USD at 4,5% with swissquote against my equities portfolio.

I used to borrow against my cryptos for 1% but after I have lost some money with Celsius that has become too risky recently

Living of dividends just earns too little for me and I don’t want to sell any assets in the current crash. I pay some taxes on dividends, but when I deduct my mortgage and my interest rates it’s very little

True, my current loan is with 15k CHF not that big. I wanted to be more defensive at that time but then my monkey brain got bored and I tried to be clever and bought a lot of gold with it as an “cashlike inflation hedge” in an ETF, which also went down in the meantime.

So at the moment I have both: Cash waiting on the sideline on my bank account and a loan on my trading account. This might seem a bit of a over reaction/contradiction, but my wife gets nervous when our shared accounts are too low. In the meantime I still trade a bit for fun (and mostly unsuccessfully). For the big bets I’ll wait for a clear uptrend.

Maybe I should get a job

Yes I know… Swiss bias again I guess. I know I get the correct documents for my taxes. Something that has been sometimes difficult with non-swiss companies.

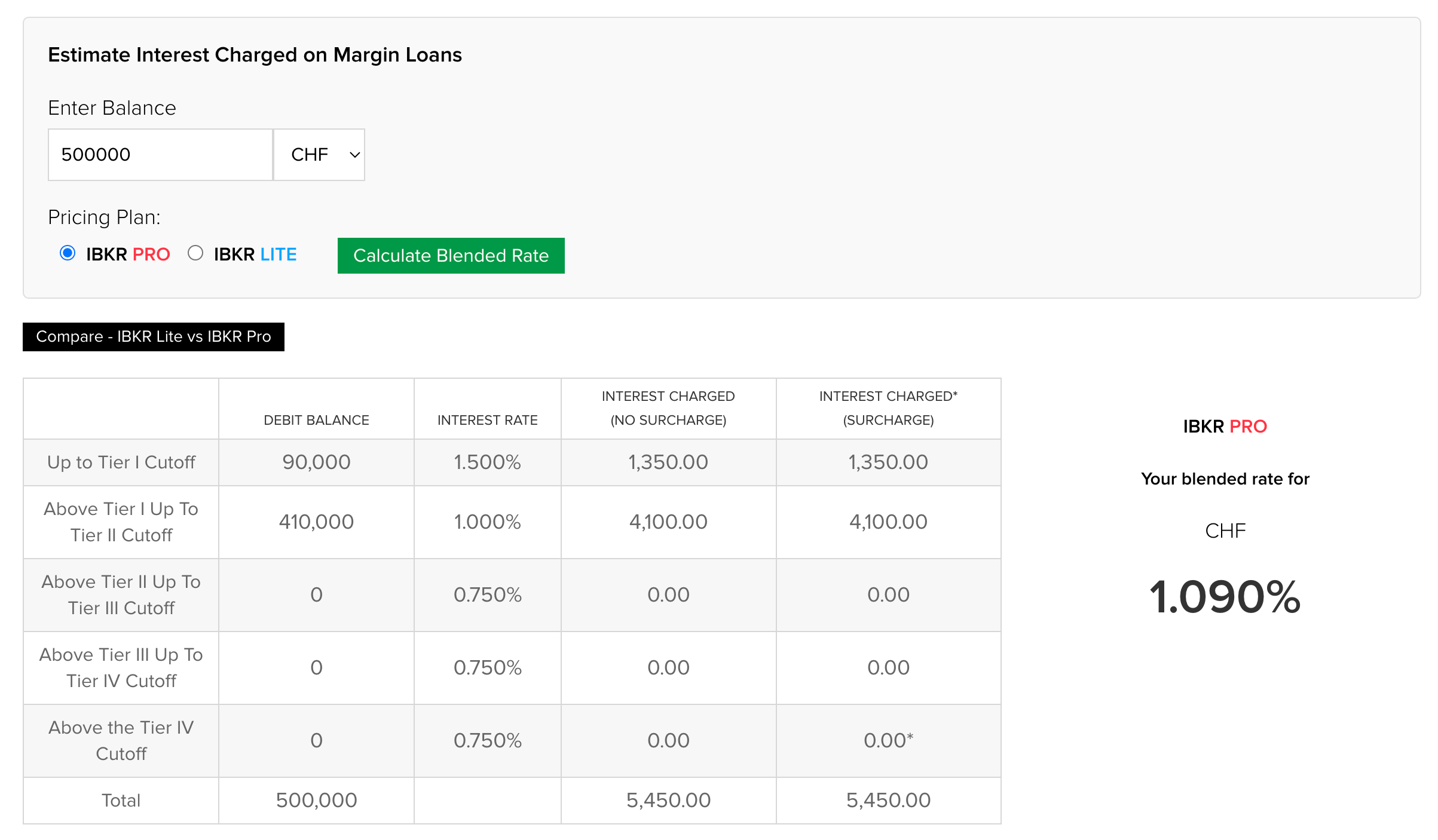

What are their rates?

For CHF, first 90k is 1.5%, then above this threshold it is 1%. So if you borrow 500k you would pay a blended rate of 1.090%. Same for EUR. USD is more expensive, you would be in for 3.43%.

What is still messed up is that inflation is much higher than interest rates

e.g. swiss inflation 3.4% whilst IBKR interest rate is 1.5% → in real terms the loan decreases in value faster than interest accrues. Not to mention that interest is deductible from taxable income for a swiss investor

On the other hand if we borrow to buy equities, the risk is that if interest rates go up share prices are likely to go down (present value of future cash flows from equities decreases)

That is also true with our 10 year mortgage of 1,6%

The only way to really lower inflation would be to solve the global energy/deglobalization issues, something that seems unlikely for political/moral reasons. I don’t think this is necessary bad. Our reliance on cheap Russian energy has to end and people here will simply not work for the same wages as in China.

Still interest rates cannot stay highly elevated over a long time. High interest rates not only means destruction of the economy but also destruction of tax revenues and higher debt service costs for the governments. The US and the EU with their astronomical debt levels would either default quickly and the swiss export industry would get annihilated by a skyrocketing CHF.

I expect instead inflation will stay higher over the next few years (around 5%) and we will probably get a new creative way to obscure this so that the official number comes down to the target of 2%. Inflation is no longer in the headlines. Central bank are back to pumping liquidity into the markets and politicians can go back to throwing around money to keep the voters happy. Mission accomplished.

In short: I feel comfortable buying shares of companies with pricing power with debt that gets eaten away by inflation in the long term.

If you had enough money to FIRE tomorrow, how would your portfolio look like?

Here’s mine (for now )

60% total world stock market (e.g. VT)

32% total world bond market (CHF-hedged, e.g. BNDW)

4% Cash (1 year of my expenditures)

4% Gold (for diversification, protecting from negative real yields in recession, currency hedge)

Oh sweet dreams of FIRE! If I have no restrictions, it would be something like

70-75% in a tax- and fee-optimized all world market capitalization weighted stocks portfolio.

5-10% gold (haven’t finished my analysis/simulations yet)

20% initial CHF cash buffer. Includes CHF deposits with different lengths of locking: checking accounts, savings accounts, medium term deposits, maybe individual bonds and money market funds. But nothing that can lose value in nominal CHF.

If stocks+gold grow to more than 85% of the total portfolio, rebalance to the initial allocation.

Withdraw 4% of the last ATH value of the stocks+gold portfolio (after rebalancing) in CHF per year. I don’t want to deal with the inflation adjustment and CHF inflation is quite low.

Unless stocks+gold drop by 20+% from the last ATH in CHF. In this case stop selling, reinvest half of dividends and rebalance stocks+gold, withdraw from the cash buffer and use half of dividends to refill it. Wait until next ATH value of the stocks+gold portfolio in CHF, then start selling again. The cash buffer, yield from cash and dividends should sustain me for 8+ years, after that it’s margin loan.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.