Hi,

I claimed the consulting process (it was on english), and mentioned many times, that I didn’t wanted a life insurance, just only a 3rd pillar account, but I ended up in one.

Read the other topic and my posts, I hope you can also come out of this contract.

Fingers crossed!

Currently going through the same nightmare with AXA after 2.5 years of wasted money. Eager to learn from your experience: what do you mean with “claimed the consulting process?”

Did you have any other insurances with AXA that you could cancel as negotiation leverage?

I tried simply to describe, the consultation with the agent has beed done in English. My argumentation was simple: I told them, I didn’t understood all part of the consultation because of the lack of my English knowledge.

On the other hand I mentioned at least 3 times, that “I strictly don’t want to have a life insurance”.

Of course every case is individual, and there was a lot of humanity in my case. At the end was important, the agent gave the approval to AXA to annul the whole contract with cashing out the whole original paid-in money value.

I hope you can move lucky forward too!!! Fingers crossed

Hi FirePhoenix, I suffered the same as you in French in 2016. Have you signed in Geneva office? maybe we shall make an effort together to quit without loss.

Apologies if this post disturbs anyone, I would be grateful if anyone can advise me what to do now to minimize my loss.

I did a search on the Forum about 3A and have read a few discussion threads, my situation looks kind of similar. the premium invoice for this year was due 1st Nov and seems I have till month end to pay for it.

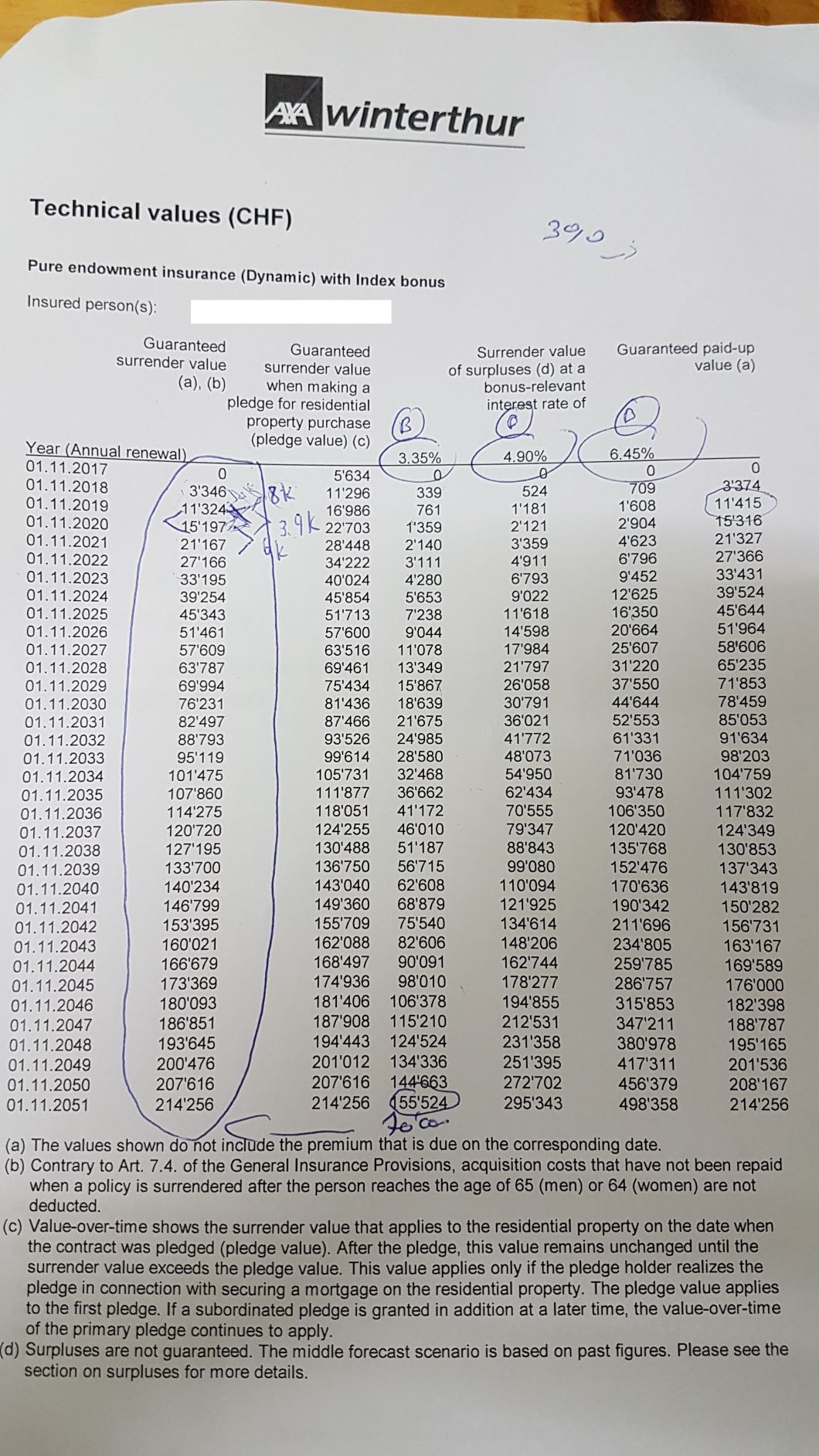

I have bought 3A at Axa Winterthur since 2016 and paid 3 annual premiums of 6.8k CHF.

Life insurance Protect Plan

Contract

Policy dated: 24.10.2016

Beginning of the contract: 01.11.2016

End of the policy: 01.11.2051

Pension type: tied

Premium rate: CHF 6’798.00

Payment method: Annually

Value

Calculation date: 10.11.2019

Surrender value: CHF 11’641.00

Redemption value of bonus: CHF 484.00

Policy pledged: no

I think not paying premium in the first 5 years will lead to the ending of the contract and policy. 2019 premium is due and the deadline to pay is end November.

1.When I signed the contract in 2016, the salesman confirmed to me that I will be able to withdraw my money if I leave CH or buy a house, WITHOUT specifying that I can never withdraw the amount I paid. Do you think this act of hiding information can be used to sue them to get a full refund as information was not given in a transparent way? Or legally they are not at fault at all or very difficult to win against them?

2.It seems that if I close my AXA 3A without buying a 3rd pillar at bank, I have to give back the tax saving I have had?

3. Therefore what is the best action I shall do now to minimize my loss? AXA advisor tells me that if I close my account now, I will only get back the 12k, which means I will have 9k incurred loss.

Close it now, get the rest back and forget it. Transfer the rest to VIAC.

It’s an insurance. Why should you be able to withdraw the amount that you paid? You are paying for the insurance benefits (like invalidity and losing your job).

It’s very simple: you’ve been f*cked. Unfortunately for you this scam is 100% legal in switzerland. Close account (unless you still need the insurance for some reason?), cut your losses and write it off as a financial lesson.

In principle maybe, but you’re in the unfortunate position where you’re the one who has to prove the fact of this alleged miscommunication to the court. Most likely, unless your salesmen was totally dumb (e.g. let you record him), you will not succeed at doing that with the necessary rigor, they would judge the case according to papers you signed which I’m sure are all in their favor, and thus you would only waste your time and money further.

Thanks Cortana, I have seen some posts on this forum that people succeeded getting their money back after 3 years. like the post of Mr.Paprika @Mr.Paprika

BTW any idea about my 2nd question?

I claimed the consulting process (it was on english), and mentioned many times, that I didn’t wanted a life insurance, just only a 3rd pillar account, but I ended up in one.

Read the other topic and my posts, I hope you can also come out of this contract.

Of course it was a lot of goodwill and humaneness behind it, but at the end I didn’t loose almost 10k CHF.

One thing you probably should do to minimize losses is ask the insurance Ombudsman to verify calculation of policy’s buyback value. By law, you have a right to this and the insurance must provide all necessary documents for it. And cancel the policy asap if you haven’t already or you’re on the hook for another year of premiums. Not paying your bills doesn’t terminate contracts in Switzerland, they will still be able to collect what you owe through legal means, and with interest.

Thanks for your prompt reply. I did read every of your post before posting… Did you make the claim to the person who sold you the insurance or to the management? I only have the contact detail of the sales person…

Thanks, do you think I still have time to do these? my policy started with them on 1st Nov 2016, so I guess the premium for this year is due 1st Nov, the sales person told me that I have till month end to pay the invoice, and failing so the contract will be ended… so it’s another lie here?

I talked to them both. AXA, and the broker who sold me the insurance. AXA contacted the broker after my claim, and took almost 1,5 month to end up the whole process.

If you have that statement officially in writing or as part of the contract (read your contract!) then it’s fine and should prevail in a dispute. Otherwise you should explicitly cancel, most contracts in switzerland would not be that easy to get out and usually need to be cancelled with 1-3 months notice - when you get the bill it’s already too late.

@nugget dear nugget, could you please have a look on my situation? I have read your posts. BTW what is "Wert- bzw. Kostenaufstellung” in English or French? I cannot find it online…Thanks a lot

thanks a lot. no I don’t have it in writing…

1.sorry I know it is stupid. but my insurance papers are currently in a friend’s place in a different city…is the “contract” the 9 pages that this OP has uploaded in his first post? I don’t remember having received any other document called “contract”, I have a similar document than that OP’s, and it is weird that there is no clause about cancellation, notice period etc in this document…

I guess it’s the same here: take the losses asap, reinvest in your low-cost ETF portfolio and be amazed 20 years from now on how much better it went. beware Schiller PE is high curently, so there might be below-average returns in the coming years. Still, that 6.8k policy sucks hard.

If you con prove it, i.e. have a signed document that says “I, the salasman did not transparently inform”, then you might have a chance suing. otherwise, you will have a hard time gaining anything from suing other than large lawyer costs

you can cancel the AXA policy - but the resulting cash is locked in the 3a system. put it to a 3a savings account (currently ~0.2% yield) or check out security depot solutions from VIAC, VZ, Banks, swisscanto,… around here, ppl will recommend VIAC/ VZ for most mustachian-like investments within 3a

Take it and run. your losses (including opportunity costs) increase every year you are with AXA and not with your low-cost portfolio. Mind, the AXA product probably contains some death- and work-inability insurance and make sure you sign up for according replacements in case you need those.

But make a prcize estimate of your losses: only a fraction of those 6.8k wen to building a stash, some of it went to fund the insurance policies. this money is not a loss but a cost for an insurance cover you enjoy. deduct this from your calculation, and then you will have a better idea on how much loses you have. will be smaller then you think now. see my post

Ombudsmann

i did not use that, and I cannot tell if it is advantageous. I dont know any details

Wert- bzw. Kostenaufstellung

this is a formal listing of what components of your policy cost what money, i.e. what goes to the stash, what tho which insurance. in my case back then, the whole thing included two insurances (death / work.inability). You can request it formally at your broker (or better directly with AXA). The interesting part in there was nut as such written in my contract.

In the end I am sorry for you, but there is no known way around just quitting and taking the losses.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.