I indeed count it as part of income/savings.

Edit: same for employer contribution

I indeed count it as part of income/savings.

Edit: same for employer contribution

For 840.- that is a crazy deal ![]()

Ofc also depends on what a ‘lesson’ is.

It’s a setup that works well for me, it’s online lessons with a tutor from my home country, and we usually do short 40-45 minute sessions. Mostly discussing an article I read beforehand (Spiegel and others) + vocabulary work etc.

So biggest part is speaking practice and not much grammar or writing exercises. I would say I spend no more 5 hrs on German per week

Because he/she can’t live without the gym (“living expenses” category) and considers swimming a “leisure”. ![]()

Jokes apart, I recommend having a “Sport” category!

Here is our yearly spending for 2025 (agregated from bank accounts and cc statements, so it’s not perfectly put in categories).

We are a family of four (8 & 5 year old kids) living in an owned Home somewhere in Solothurn.

all expenses without taxes: 82946.- CHF (up 4.5k from 2024 :-S I’d rather have it go in the opposite direction, but that seems to be the norm for every year)

some categories:

childcare (1 day per week for both kids): 10688.- CHF (that is all kids activities included)

health: 17143.- CHF

house: 15211.- CHF (no renovations this year)

Car, phones and home internet are paid for by our business and therefore not included in the above expenses.

again a bit higher than last year. really want to try to keep expenses steady or even a bit lower.

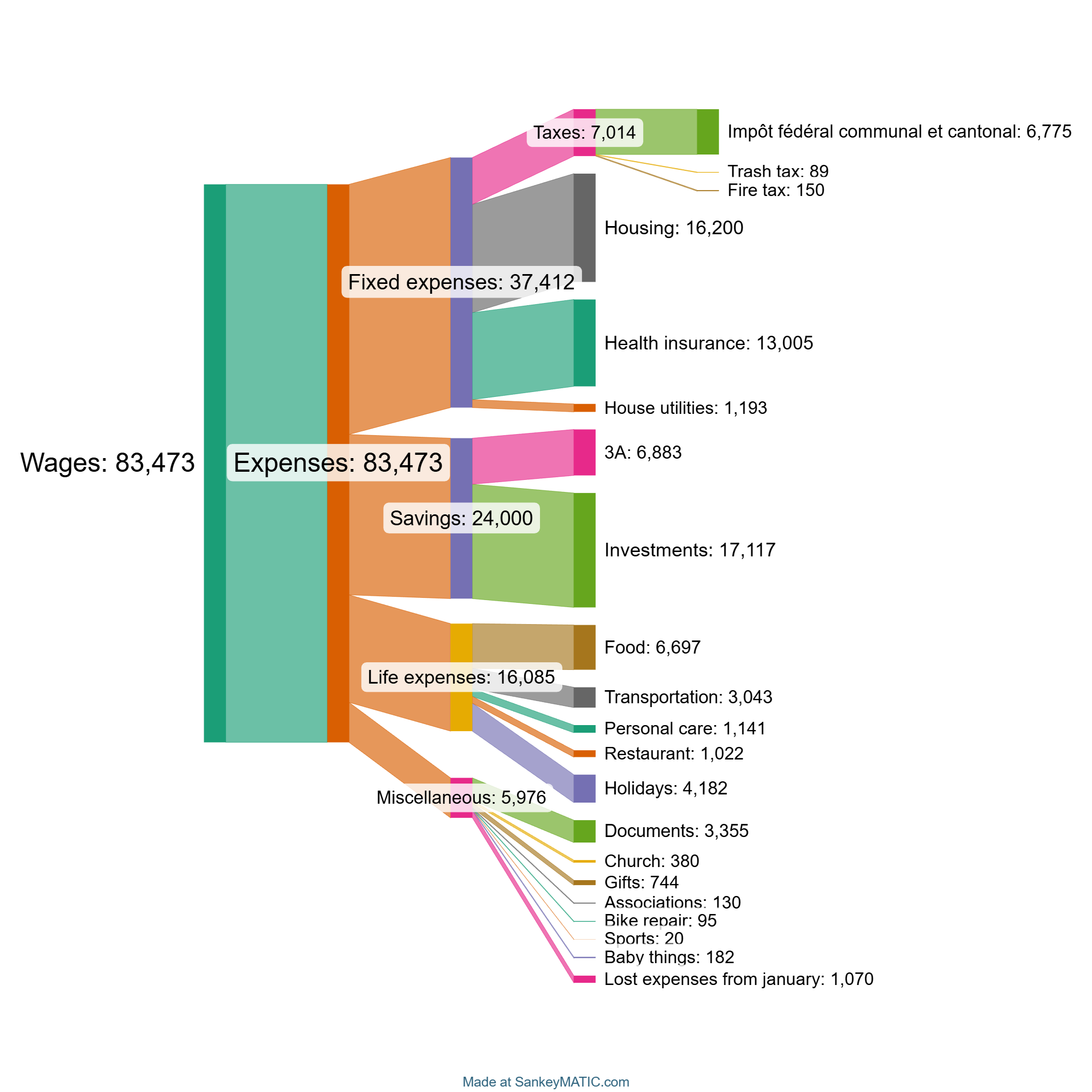

Hello Everyone,

Last year’s good resolution was to budget and to start investing. This is how I found the Mustachian and here are the results of our first year.

I’m 34, working for the past 4 years after a Master, I only worked 80% 2022 and 2023 so it was harder to save.

I’m married since 2024 and am the only earner. My wife is from abroad and is studying.

Documents are studies cost and an attempt to get her driving license.

Lost expenses from January is because we only started budgeting in mid-January.

I also started investing, the ~55k I had saved from the past years and turned it (including the 17k savings of this year) into 102k which is about 40+% gain. I was frustrated of paying more bank fees than receiving interests so this is a pretty satisfying result for my first year. The biggest gains were from some investments in gold and Silver so I know I shouldnt expect such big gains the following years.

My wife is expecting a baby next month so this year will probably see some increases in the in the expenses, we will have to adapt the budget as well.

Family of 4 in BL. Older kid is almost 6 and younger one is 1.75. Biggest expense is Childcare/Kita/Aftercare and expected to remain the same for the next 2-3 years, until the younger one starts KG.

Goal for 2026 is to stay at 100 KCHF or lower.

| Category | 2025 Expense | % |

|---|---|---|

| Childcare | 23,783.7 | 21.51 |

| Travel | 15,115.0 | 13.67 |

| Health Insurance | 14,047.2 | 12.70 |

| Apt Annual Maintenance fees | 12,887.3 | 11.65 |

| Groceries | 10,541.6 | 9.53 |

| Mortgage Interest | 6,269.2 | 5.67 |

| Children & Babies | 3,366.6 | 3.04 |

| Eating Out/Cafe/Lunch | 3,062.9 | 2.77 |

| Driving License | 2,119.0 | 1.92 |

| Financial Planning | 1,909.8 | 1.73 |

| Gifts & Donations | 1,902.2 | 1.72 |

| Other Insurances | 1,822.2 | 1.65 |

| Doctor | 1,652.3 | 1.49 |

| Car | 1,596.7 | 1.44 |

| Household cleaning | 1,267.2 | 1.15 |

| Electricity | 1,141.3 | 1.03 |

| Electronics | 979.9 | 0.89 |

| Mobile | 850.7 | 0.77 |

| Clothing | 780.0 | 0.71 |

| Petrol | 768.6 | 0.70 |

| Household stuff/appliances | 667.4 | 0.60 |

| Apt. Renovation 2025 | 659.4 | 0.60 |

| Internet | 468.0 | 0.42 |

| Personal Care/Hygiene | 442.9 | 0.40 |

| TV Bill | 335.0 | 0.30 |

| Tax Filing | 296.8 | 0.27 |

| Public Transport | 285.0 | 0.26 |

| Pharmacy | 259.1 | 0.23 |

| Furniture | 239.2 | 0.22 |

| Subscriptions/Memberships | 229.4 | 0.21 |

| Fees and Charges | 180.0 | 0.16 |

| Ebike | 169.8 | 0.15 |

| Education | 139.1 | 0.13 |

| Parking | 127.4 | 0.12 |

| Government | 112.8 | 0.10 |

| Other Shopping | 99.1 | 0.09 |

| Books | 7.5 | 0.01 |

| 110,581.3 | 100.00 |

| Category | 2026 Budget |

|---|---|

| Childcare | 26,500.0 |

| Travel | 10,000.0 |

| Health Insurance | 14,250.0 |

| Apt Annual Maintenance fees | 13,000.0 |

| Groceries | 9,000.0 |

| Mortgage Interest | 6,734.4 |

| Children & Babies | 2,500.0 |

| Eating Out/Cafe/Lunch | 2,400.0 |

| Driving License | 400.0 |

| Financial Planning | 250.0 |

| Gifts & Donations | 500.0 |

| Other Insurances | 1,822.2 |

| Doctor | 1,500.0 |

| Car | 1,400.0 |

| Household cleaning | 4,800.0 |

| Electricity | 1,141.3 |

| Electronics | - |

| Mobile | 862.8 |

| Clothing | - |

| Petrol | 750.0 |

| Household stuff/appliances | 200.0 |

| Apt. Renovation 2025 | - |

| Internet | 468.0 |

| Personal Care/Hygiene | - |

| TV Bill | 335.0 |

| Tax Filing | 296.8 |

| Public Transport | 300.0 |

| Pharmacy | 250.0 |

| Furniture | 200.0 |

| Subscriptions/Memberships | 200.0 |

| Fees and Charges | 180.0 |

| Ebike | 169.8 |

| Education | - |

| Parking | 127.4 |

| Government | - |

| Other Shopping | - |

| Books | - |

| 100,537.7 |

@sirob Too many (similar) categories for my taste. Could be reduced to max a dozen categories and be more insightful at the same time.

Or two tiered system, eg Health care on top and insurance, phamacies, doctor visits below.

How is categorizing done? Semi automated or fully manual?

Nice savings, given that is for 2 people. ![]()

If you plan to play this game for the long run, that portfolio would be too concentrated investing for my taste (if you get +40% last year). Worked out well for you last year, but you likely know the consensus on the forum about diversified strategies. ![]()

completely agreed @larix.aurea needs to be slimmed down to max 10-12 categories. The raw data comes from a mobile app (Money Lover) but the initial set-up and category definition in that app was done in a haphazard way and thus we need to re-arrange the numbers (from the available annual export).

What’s “Apt Annual Maintenance fees” given you already have mortgage + renovation + electricity + appliances + …?

I guess a combination of charges + something, but it looks huge to me.

Since we are both in BL, I asked an LLM to compare our budgets and then I removed childcare and mortgage costs (I assume retirement budget where kids are grown up and house is paid off)

| Category | Budget 1 (Annualized) | Budget 2 (2025 Plan) | Diff |

|---|---|---|---|

| Health Insurance | £16,296 | £14,047 | £(2,249) |

| Travel & Holidays | £4,560 | £15,115 | £10,555 |

| Housing & Maintenance | £6,480 | £14,183 | £7,703 |

| Groceries | £10,392 | £10,542 | £150 |

| Dining Out | £1,720 | £3,063 | £1,343 |

| Transport (Car & Public) | £3,420 | £4,897 | £1,477 |

| Utilities (Elec, TV, Internet, Phone) | £4,764 | £2,795 | £(1,969) |

| Medical (Out of Pocket) | £660 | £1,911 | £1,251 |

| Lifestyle, Hobbies & Gifts | £2,424 | £2,309 | £(115) |

| Shopping & Personal Care | £384 | £2,302 | £1,918 |

| Insurances & Financial/Admin | £804 | £4,209 | £3,405 |

| Misc / Uncategorized | £600 | £99 | £(501) |

| TOTAL | £52,504 | £75,472 | £22,968 |

And monthly:

| Category | Budget 1 (Annualized) | Budget 2 (2025 Plan) | Diff |

|---|---|---|---|

| Health Insurance | £1,358 | £1,171 | £(187) |

| Travel & Holidays | £380 | £1,260 | £880 |

| Housing & Maintenance | £540 | £1,182 | £642 |

| Groceries | £866 | £879 | £13 |

| Dining Out | £143 | £255 | £112 |

| Transport (Car & Public) | £285 | £408 | £123 |

| Utilities (Elec, TV, Internet, Phone) | £397 | £233 | £(164) |

| Medical (Out of Pocket) | £55 | £159 | £104 |

| Lifestyle, Hobbies & Gifts | £202 | £192 | £(10) |

| Shopping & Personal Care | £32 | £192 | £160 |

| Insurances & Financial/Admin | £67 | £351 | £284 |

| Misc / Uncategorized | £50 | £8 | £(42) |

| TOTAL | £4,375 | £6,289 | £1,914 |

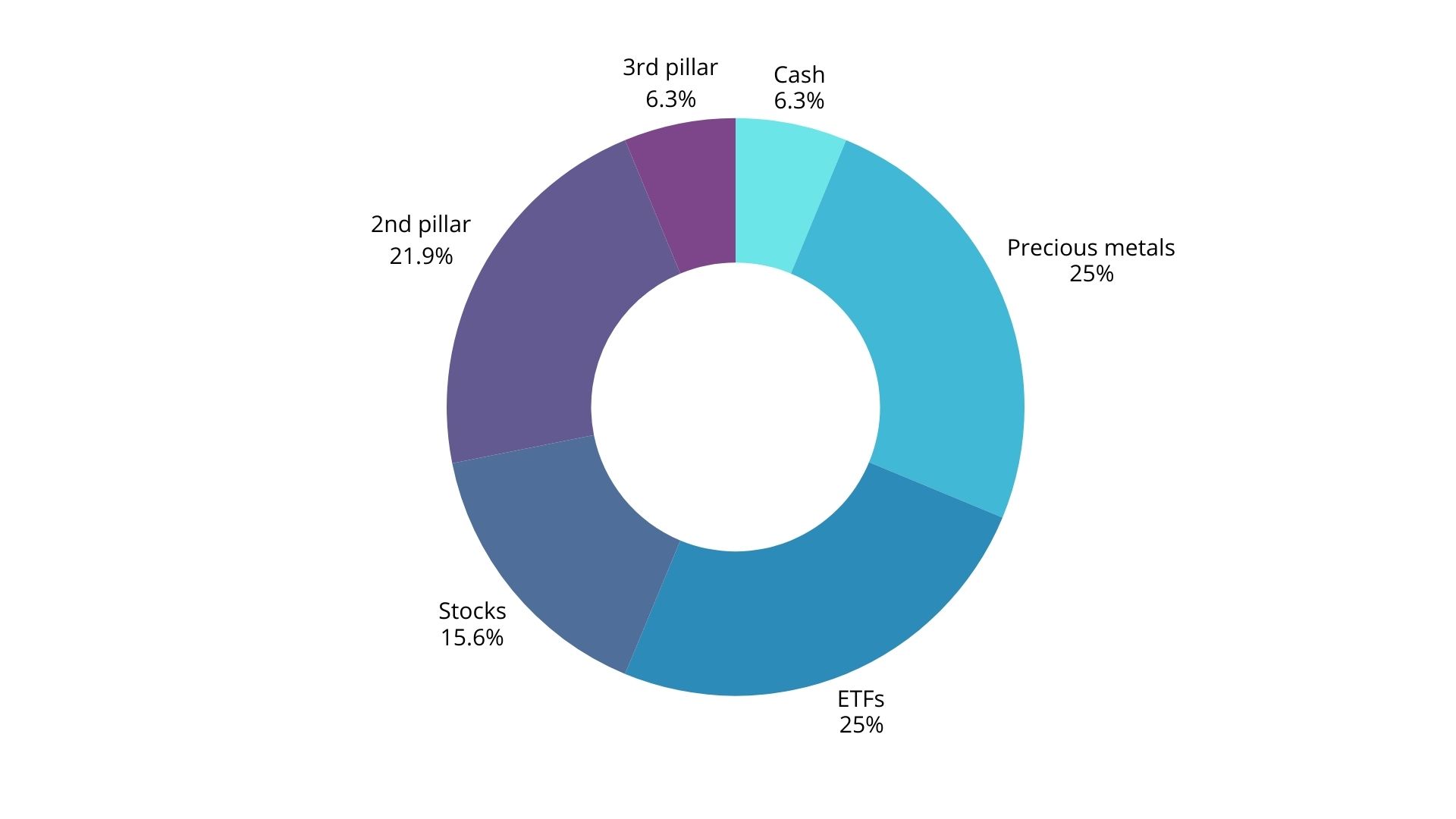

I have 40% in precious metals, 40% in “safe” ETFs and 20% in stocks. The big gains are mainly due to a few stocks and the precious metals. Is it not diverse enough or too concentrated? What would be a good strategy?

These are the annual community maintenance costs - charged on a quarterly basis.

we have a big apartment complex - 10 buildings in one section with 3 families per section so 30 families in all. The costs mentioned cover the maintenance/renovation and upkeep of the community designated areas - underground garage, garden + lawns, common expenses for all the 10 buildings and expenses for the specific building block that we live in. Also top-ups to the community renovation funds.

On a monthly basis we average around CHF 1100 for these costs.

These costs can be absurd. I was once looking to buy a flat in Basel, the kind you can probably rent for around 2’000 per month. The monthly costs were 1’600 and they proudly talked about how this would increase as they would buy earthquake insurance next year.

Seriously, what the hell is the point of buying a place to live if I have to pay almost the same amount in rent for random stupid costs that other owners of the flat have voted for?!

Thanks!

If you don’t mind sharing, how much of % of the flat value does this represent?

I would have expected around 1%, probably in the same ballpark as your mortgage payments. You’re at almost double here, but maybe you’ve already paid a fair share of the mortgage? The amenities don’t look extra fancy from your description.

We can never know what the future may bring but your asset allocation sounds reasonable to me. Was good for 2025 and it looks like the FUD will continue. The precious metal part helps with this. Where is your cash? Getting an overview of all your savings (cash, bonds, real estate, precious metals, pillar 2, pillar 3, stocks/ETFs, etc) will help determine a suitable allocation going forward.

The annual maintenance costs represent approx. 0.8% of the current flat market value. The apartment has been evaluated last year (Apr 2025) by UBS and E&V and the mean valuation was approx. 1.55 mCHF (bought at 1.1 mCHF in mid-2020). Mortgage represents 0.4% on an annual basis.

I completely agree with @PhilMongoose statement that we are having to pay more annual maintenance costs because other owners in the STWEG have voted for them. This is also an ongoing bone of contention between the various families.

For cash I just keep 5k for month to month expenses and 5k as an emergency fund to reassure my wife. I invest all the rest regularly. I have a small 2nd pillar as I got out of studies in the past 4 years. Same for the 3rd pillar. I stupidly took a 3rd pillar insurance and cannot get out of it right now. The image is my savings currently or i guess my net worth of around 150k.

Looking well rounded, so to speak ![]()

So did I. I hope you can at least pause additional contributions indefinitely, because it most likely is a bottomless pit of poor returns.