Oh I didnt think of pausing it, I think I have some penalties if I do so. I put around 26k and so far and they told me it’s worth around 10k or so. I wanted to wait until I can at least get my money back even if it’s a poor return. I need to study the question better before taking a decision.

Double check, there’s a chance the money is gone (to pay the bonus of the person who got you to sign + the insurance part)

10 Likes

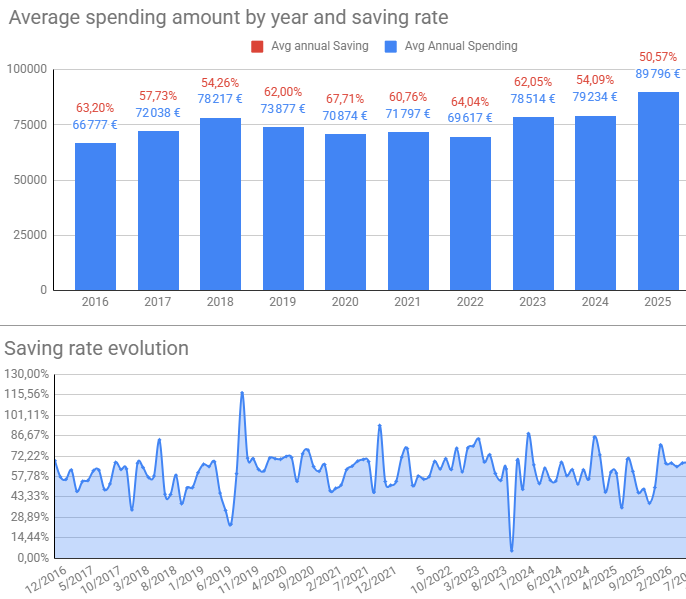

Back to the topic - the first time I calculated the actual spending for 2025 and I’m kind of shocked and think we could do much better, seems we’re not frugal at all… even though net worth increased by 250k in 2025 - we “only” contributed 91k through savings, which is a pre-tax saving rate of 35% and post-tax of 42% (not including pension fund contributions for both of us)

Here’s the details: Net household income 258k / Savings 91k / Expenses 123k / Taxes 43k

It is a monthly expense of 10300 CHF for a family of four - Annually / Monthly

- Vacation 19,3k (extraordinary in 2025, usually 8000) / 1600

- 2 cars 12,1k / 1000

- House interest / utilities 18,5k / 1500k

- Groceries 11,8k / 980

- Clothes/Shoes 6,2k / 520 (seems high)

- Eating out 3,7k / 310

- Healthcare 21k / 1760

- Kids/Daycare 4,2k / 350

- Hobbies 5,3k / 290

- Insurances 3k / 260

- Presents 1,8k / 160

- Public transport 0,6k / 55

- Other expenses (acquisitions like furniture etc.) 15,3k / 1280 (most potential for savings)

What do you guys think?

2 Likes

maybe remove ‘fixed’ costs like tax etc. and then calculate the savings rate as a percentage of the variable/discretionary? because it seems not too bad and if you beat yourself up over fixed costs that you can’t easily change, then it is not helpful.

IMO this is quite decent. (*)

And 10.3k for 4 seems reasonable too.

Plus you identify travel as an outlier this year, so it would be more like 9.5k.

I don’t think you need to worry too much,

as long as you get value out of 2nd car and those clothes+furniture parts you highlight. ![]()

Otherwise those would be the 3 areas I’d try to address.

(*) Primarily because mine is hovering about the same ![]() (covering most expenses for 2 persons)

(covering most expenses for 2 persons)

1 Like

It is a very good saving rate, based on a relative scale. If you don’t pursue an early retirement, anything above 20% (not including the second pillar) is good.

On the other hand, 120+k expenses for a family of 4 looks like a lot on an absolute scale, so you might think about downsizing. But it’s nothing unreasonable in your case.

3 Likes

Thanks for your feedback - well I actually do pursue an early retirement - we’re early 40s now so early fifties would be nice. But as said in the other thread, I feel that with 1mio (out of 2.3) of net worth locked in our primary home it could be difficult. Also considering that pillar 3A and Pension Funds would be also locked until at least 58…

So yes, we need to think about downsizing… a good objective for 2026 would be to get it down from 123k to 105k… I will set that as our objective and revisit in one year ![]()

My turn for a family of 3 living in Geneva (with a 3 y.o.).

This year is the end of allowances benefits for my wife. She got a small occupation for 70% of her time to stay active and keep the daycare.

Our annual spending increase to 89k/year.

My main cost increase were link to daycare 5 days/week, more insurances, more food/travel spending.

Some details but it is not very well categorised …

| Category | Monthly | Yearly |

|---|---|---|

| Mensual rent and charges (Naef) | 1,450 | 17,400 |

| Charges hot water and heating (Naef) | 189 | 2,264 |

| ASLOCA | 38 | 452 |

| CODHA | 17 | 200 |

| Internet Fiber (Sunrise) | 42 | 505 |

| Power (SIG) | 30 | 360 |

| Swiss Tax - Serafe - Radio et Television | 28 | 335 |

| Geneva Personal tax | 2 | 25 |

| Fortune tax | 270 | 3,237 |

| Assurance protection juridique - Dextra | 20 | 240 |

| Smile.Direct - RC + Assurance ménage | 23 | 273 |

| Car rental insurance | 0 | 0 |

| Laundry (Lavorent) | 33 | 396 |

| Caution (BCGE) | 2 | 20 |

| LAmal + complementaries | 1,246 | 14,953 |

| Groceries FR | 966 | 11,587 |

| Groceries CH | 1,128 | 13,536 |

| Train | 117 | 1,403 |

| Babysitter | 33 | 393 |

| Holidays/hotel | 8 | 99 |

| Public transport | 1 | 12 |

| Rental flat in France | 400 | 4,797 |

| Wife spending + family house | 1,646 | 19,752 |

| Total | 7,687 | 92,238 |

My saving rate will continue to sink except if I have a career change or if my wife find a real position. ![]()

In the saving rate, I include both revenue, bonuses, the second pillar (employee + employer contributions), rental revenue employer shares purchase at cost price but not the dividends or free shares granted.

5 Likes

Do you really have no spending on bars, restaurants or holidays? Is that the effect of having a young kind at home?

I easily get (for 2 people) to 4k/5k in bars + restaurants a year, and holidays (flights, hotels and activities) will be in the 3k/5k range depending on the year.

The other thing that stands out positively in your breakdown is your rental cost, which seems super cheap for 3 people in Geneva.

Yeah I need to switch flat and will certainly pay 2800-3300.- by month soon.

I spend almost nothing on bar and holidays. Since our son is born we have mostly visited our families and family home (we have 2).

I mostly account for travel costs and the nightout are mixed in the groceries section… I need to dig a bit more in my wife sending but no time to do it.

I also do not include revenue tax in myspending and deduct it from the salaries. It make no sense to me as this cost will drop dramatically if you stop working.

However, I should include the fortune tax as it should continue to grow after retirement.

I’m glad you posted this,.

Some of the costs lists in this thread just don;t seem to be based on Swiss prices, or are missing the huge expense of children..

When we moved to CH we were paying 4.8K for daycare, 3.5K for a basic apartment without utilities, 1.6k health insurance. Even without everything else it is easy to get to 120K year costs!

1 Like

I have a category called insurance and a category called sport.

- I record my supplementary insurance as an expense under insurance

- I recod my gym membership as an expense under sport

Now I have received CHF 200 from my supplementary insurance for my gym membership.

My question:

Would you record this as income in sports or insurance? I have currently recorded it under insurance because it makes my insurance “cheaper” because I benefit from it. On the other hand, I could also categorize it as sports, because my gym membership became cheaper. The category insurance sounds more logical to me. But somehow, for unknown reasons, I’m not convinced.

4 Likes

These are the hard questions of life. ![]()

Personally I would book it under sport, with the only reason that I would find it strange that if I cancel my gym membership, suddenly my insurance goes up by 200.-.

But then again the same is the other way that sports gets more expensive when cancelling insurance. But this feels more natural to me.

2 Likes

Insurance as it is a conditional rebate for your insurance. If you change your insurance this changes.

How about prorating it?

200 * gym membership / (gym membership+complementary health insurance) under sports.

200 * complementary health insurance / (gym membership+complementary insurance) under insurance.

I would personally register both under “health”.

For someone so interested in categories it is weird to see you posting on the wrong thread. ![]()

7 Likes

At least for health, I have a third (sub-)category for reimbursements.

That way, you have the net amount, yet still have total premiums visible.

For other categories, it’s a bit random. Not that many cases, but typically I lower the reimbursed or discounted category (i.e. sports in this example).

2 Likes