How can your car be this cheap? My car insurance alone is above that and I drive a cheap compact car.

and then only 150 for transportation?

How can your car be this cheap? My car insurance alone is above that and I drive a cheap compact car.

and then only 150 for transportation?

I received money back from Ticino this year as I bought an EV last year. Without that and not split is around 2600, which doesn’t include charging at home that is under bills.

Transportation doesn’t include trips and I’m mostly driving now when I need to move but I often work from home.

Family of 3 renting in GE:

| Label | CHF |

|---|---|

| Rent and charges | 1524 |

| Additional charges for heating and water | 9 |

| Internet Fiber - no TV | 41 |

| Power | 40 |

| Serafe - Radio and TV | 28 |

| Genève - personal tax | 2 |

| RC + House insurance | 20 |

| Car rental insurance | 9 |

| Laundry | 33 |

| ASLOCA contribution | 36 |

| Deposit at the Bank | 2 |

| Bank fees | 8 |

| Daycare | 1897 |

| Health insurance for 3 | 768 |

| Groceries+take away+restaurant | 867 |

| Travel expenses (me) | 935 |

| Monthly TOTAL | 6 178 |

| Yearly TOTAL | 74 136 |

My wife will participate in 30% of our fix costs but 50% on the groceries, take away, trips …

I did not include personal expenses of my wife (travel cost, some groceries, night out …).

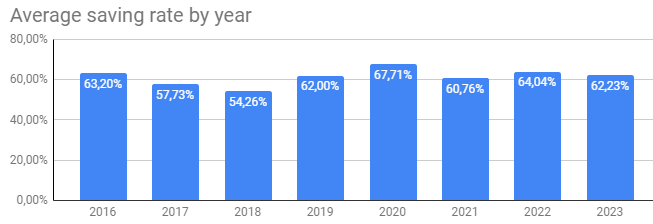

Final year with the saving rates above 60% … next year we’ll spend 12 months daycare and not 6 months …

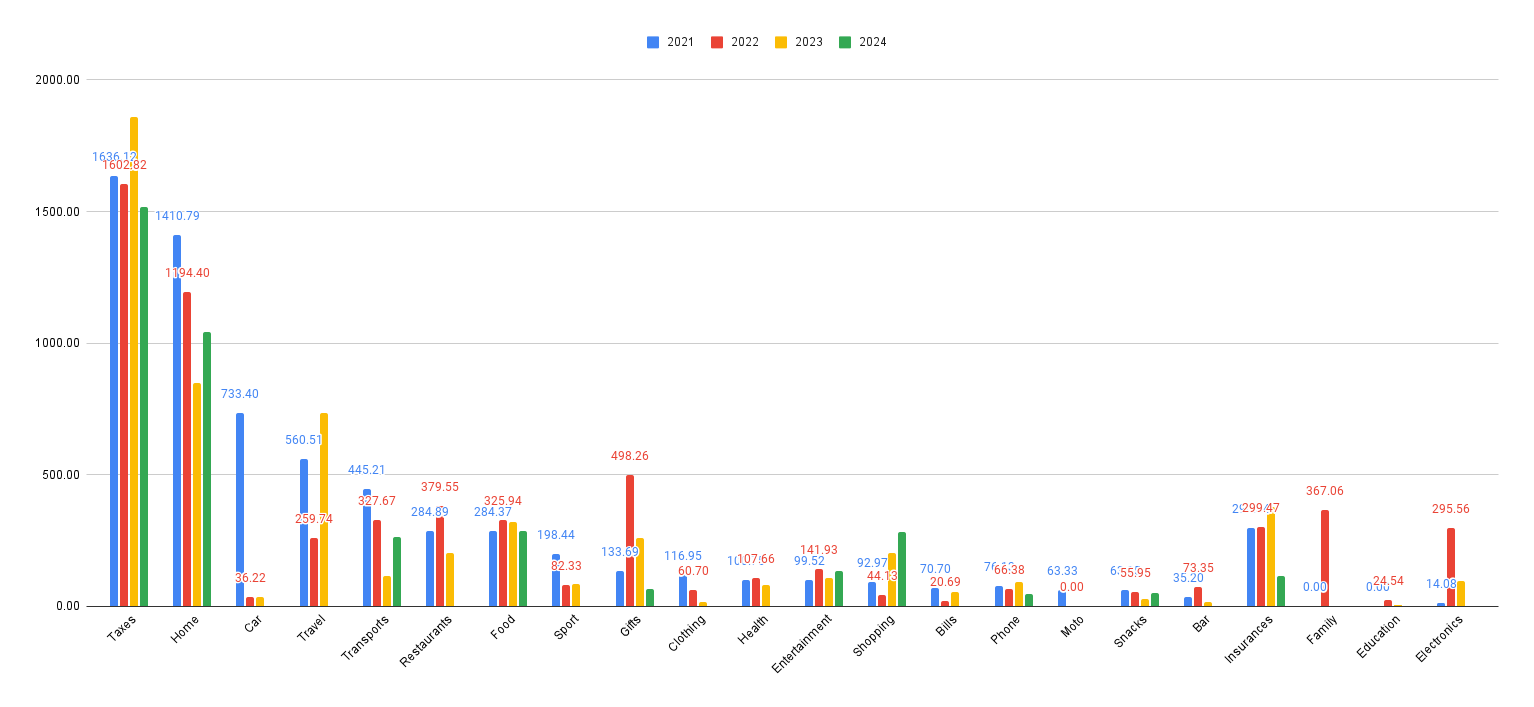

My 2023 expenses. Married, but I only count my own expenses + my share of the common expenses (we keep our finances separate and split expenses).

| Category | Yearly |

|---|---|

| Taxes | 22287.03 |

| Home | 10157.33 |

| Travel | 8,792.54 |

| Insurances | 4511.37 |

| Food | 3853.21 |

| Gifts | 3120.27 |

| Shopping | 2428.11 |

| Restaurants | 2407.35 |

| Transports | 1398.5 |

| Entertainment | 1303.15 |

| Electronics | 1131.35 |

| Phone | 1123.85 |

| Sport | 1016 |

| Health | 955.2 |

| Bills | 635.27 |

| Car | 411.45 |

| Snacks | 312.29 |

| Bar | 187.9 |

| Clothing | 175.25 |

| Education | 51.65 |

| Moto | 0 |

| Family | 0 |

| Total | 66259.07 |

And how it compares to the past 3 years (monthly averages):

All in all I’m quite happy with 2023, I spent 9k CHF less than in 2022, and almost 15k less than in 2021 ! I started caring about personal finances in late 2020, as can be guessed here.

What is “Shopping” ? You should incorporate it in Home/Snacks/Car/Sports etc instead of being by itself.

Or it’s more like “Other stuff I don’t need” ? I’m curious.

if you are living with your spouse and have a kid together, what sense it makes to give “your” expenses?

The only thing that makes sense for me is “our household expenses” in that regard.

Not if she pays the other half…

She doesn’t track all her expenses, only the shared expenses

Sorry for the late reply. It’s indeed what doesn’t really fit anywhere else, but can be bought in shops. In 2023 the main expenses in this category were ~1k for furnitures and tools (moved to a new place), a watch, and a few misc things ordered on galaxus.

Not the most precise category of course, but as it’s quite low in the list, I don’t feel the need to add more granularity here.

You could put almost everything under “Home” and the rest in “Hobby”. This way you could track better how much your hobbies costs. Or maybe watches are not your hobby so it should go under “apparel” instead.

Just my opinion. Every time I see this labeling I always wonder what I could track with them and if a separation would make sense to track something special. For example I don’t have a “furniture” label because I can use “home” to see rent+anything related to it (not on “home care” on my own list)

getting offtopic sorry.

Which tool do you use to get these nice graphs ![]()

Just Google sheets. ![]()

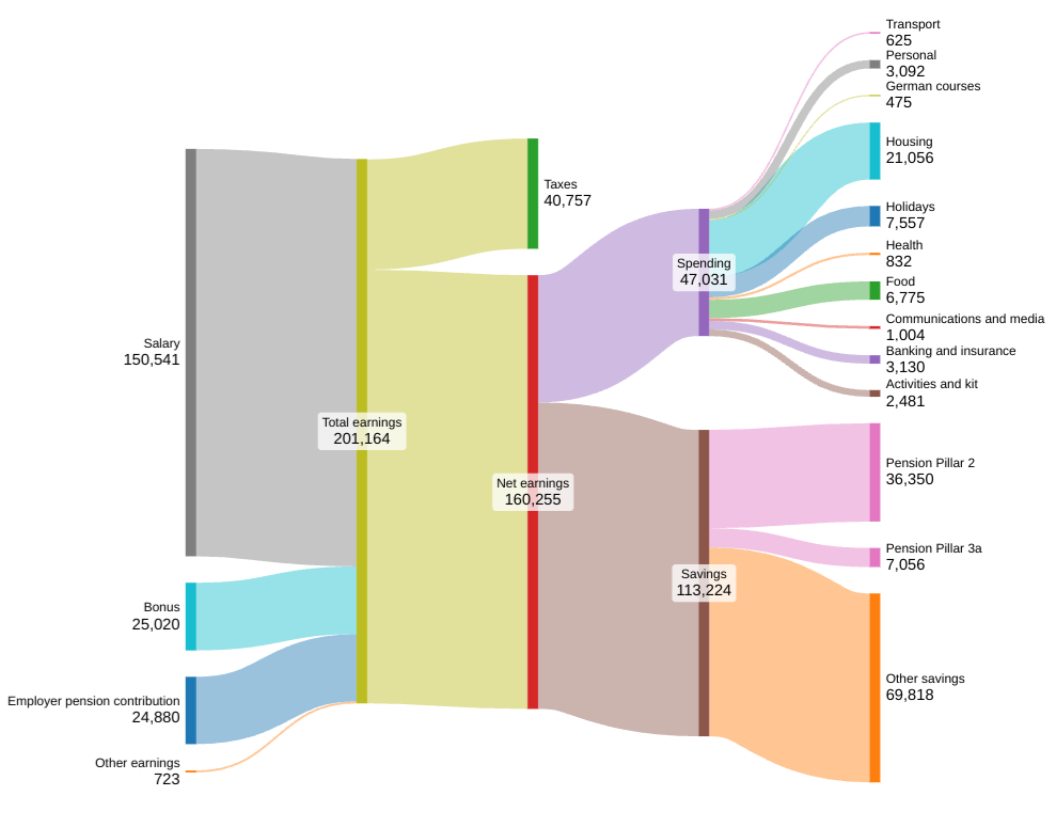

First time posting here. I´m a little late but wanted to share my full year spending for 2023.

For background to the numbers I live together with my girlfriend, as she´s studying I pay for most of the rent, all of the utility bills and somewhere around 2/3 of the cost of our joint holidays. Food we split in half. The rest of the spending categories are just for me.

Sharing it including my taxes and income so it´s clear what is and isn´t included in the numbers. I also already created this diagram so I could easily see where my money was going!

Overall spending (not including tax) was 47,031 compared to 46,340 for 2022.

I calculate my savings rate as 70.7% (all savings including pensions divided by all net earnings). I guess it could also be a lot lower if I calculated it differently.

What is baking and insurance and why is that high?

I love sankey diagrams… u did that in R?

It´s mainly health insurance, but also includes liability insurance, home insurance and a small amount for banking fees too.

Not sure what “R” is, I created it on the SankeyMatic free tool it was quite easy to use once I got the hang of it.

The plot is great!

How is it that your employer’s contribution to your 2nd pillar is 25k, but yours is only 11k?

Great employer I guess, I had this as well with a previous employer. Currently my employer also pays way more than I do.

Mine does it as well.

The amount my employer contributions is the same regardless which plan I choose (min, standard or plus)

I chose min of course, due to still only getting the bad 1.x% standard interest.

So for me the ratio is 1:4. So let‘s say I pay 200/month and my employer pays 800/month on top. It‘s made up of two parts 50:50, one is a "risk“ that is not quite static. The factors that determine that part I dont know exactly at the moment.

Thanks!

Yep Burningstone is right I´m super lucky to work for a company with a great pension scheme. They also pay a once yearly contribution into my pension based on my bonus, so that also makes it look a little higher too.

Sounds similar to mine, including the really low interest rates especially compared to the market at the moment!

For me I hope to be able to withdraw it to buy a house (for emotional not financial reasons) at some point in the future so based on a calculation I did would hopefully still be worth it to save the tax I would otherwise be paying on it.