Until the End of 2019 you should pay everything with the new Swisscard Cashback Card because you get Cashback of 0.5%. Starting from 2020 you should get back to paying with Supercard Topcard/Cumulus Cembra (0.33%), because than the Cashback of the Swisscard goes down to 0.25%.

In Coop and Partners you should only pay with Migros Cumulus and in Migros and Partners you should only pay with Coop Supercard. (you don’t get cash back when using their own card at their place)

Outside of Switzerland only Revolut and Co. should be used.

Say what? That sounds counter-intuitive. I thought when I pay with Cumulus in Migros, I get 1 point for 1 CHF and outside Migros I get 1 point for 3 CHF.

Indeed it sounds counter intuitive, but this is exactly the way it is.

If you pay in Coop with Coop Supercard Plus from Swisscard you will only get 1 Superpoint per Swiss Franc that you will get anyway (if you scan your Supercard). The money you pay at Coop will NOT count for cashback with your Credit Card. If you pay with the Migros Cumulus Mastercard at Coop and Scan your Supercard you will get the 1 Superpoint per Swiss Franc AND 1 Cumulus Point for every 3 Swiss Francs.

The same goes for Migros, if you pay at Migros with the Cumulus Mastercard from Cembra you will only get the 1 Cumulus Point per Swiss Franc that you will get anyway and no additional Cash Back. If you pay with Supercard and Scan your Cumulus you will get 1 Cumulus Point AND 1 Superpoint for every 3 Swiss Francs.

Right now there are 4 different free Credit Cards in circulation in Switzerland:

Cumulus Mastercard issued by Cembra (0.33% Cashback in form of Cumulus Points outside of Migros)

Supercard Plus issued by SwissCard (0.33% Cashback im form of Superpoints outside of Coop) - this card can no longer be ordered and all cards will be automatically replaced with Swisscard Cashback until 2020. You can manually trigger an automatic switch to Swisscard Cashback

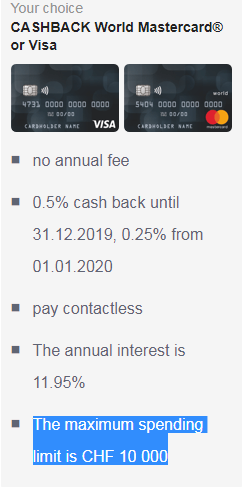

Swisscard Cashback issued by Swisscard (0.5% Cashback until end of 2019, 0.25% from 2020 in form of cash - in every store)

Supercard issued by Topcard (0.33% Cashback im form of Superpoints outside of Coop), this card can be ordered starting today and you get a sign up Bonus of 4000 Superpoints

Is it worth the hassle? 10000chf give 33 chf but since I can’t pay rent or health insurance with it, I don’t reach that amount. Did I miss a way to pay everything by CC?

Also the only reason I use the Cumulus Mastercard is that it has the insurance for when I go on holiday.

Of course you cannot pay health insurance and rent with credit card. But almost everything else you can (Rail Abo, Car mechanic, groceries, dinner, drinks etc.) for me this is easily 100 Swiss Francs cash back per year. (20k with 0.5% cashback)

Is it worth the “hassle” - you decide for yourself. But since this is not a hassle for me but rather something I like doing I can easily answer yes.

Now this I have not known… I do have the Cumulus Mastercard from Cembra.

So This Swisscard Cashback gives 0.5% cashbach on every purchase? Plus I can scan my Cumulus to get 1.5% effective cashback? Didn’t know it works like that.

And how do you get the cashback with Swisscard? It’s a monthly credit to your saldo?

All these cashback programs are so ridiculous. I honestly don’t understand why they pack you back for using the card. Surely they get this money back from the shops. In my perfect world, there would be no silly cashbacks, and shops would not pay extra if their customer uses the card…

Yes exactly until the end of 2019 if paying with Swisscard Casback and scanning Cumulus Card you get an effective Cashback of 1.5% . From 2020 it will only be 1.25%

According to Swisscard “our card payments are rewarded with cashback that is credited to your card account every month.” (https://www.cashback-karte.ch/en/)

To make it more complicated if you buy stuff online you should also use cashback platforms like https://www.rabattcorner.ch and than pay with credit card. This way, in addition to credit card fee cashback, you also get back part of the commission paid for referral.

The whole cash back thing is even more ridiculous in the United States…

As just said, I wonder who pays for this cashback. Surely, the shops. In the end these are non-trivial amounts. If your annual CC spending is 40’000 CHF, then 1% cashback is 400 CHF.

I guess if I was a big shop chain, I would put all this extra cost on the customer. Like: you come to the checkout, your final amount is 100 CHF. You want to pay with SuperCrapCard Plus, you pay 1.50 CHF extra. You pay some no-nonsense card, then no extra charge.

CC commissions in Switzerland are quite high (around 1% but can be and is negotiated by big merchants). Part of this money goes to the “CC terminal” provider, part to the CC issuer (and is used for cashbacks sometimes).

Of course in the end this additional cost is included in the price, but merchant contracts forbids them usually to increase the price for only customers paying by CC.

Also from the merchant perspective they are not able to see which CC was used, especially they don’t know if the card used has cashback or not.

Yes it’s the shops that are paying for this. But if they sign up to accept Credit Card payments in Switzerland the shop agrees to not charge the Credit Card fees to the customers. If you see a shop that asks for extra fees when paying with credit card you can request the money back via your card issuer, they have forms for that.

Another difference I found it the fee for paying in CHF abroad (for example online). The previous Supercards didn’t charge this fee, at least for Boon topups.

I’ve looked at my paper docs and they introduced this change in 2015 (I’ve got a letter from them, dated 3 september 2015, in which they announce the change beginning 15 october 2015)

The fee regarding CHF abroad in regards to online shopping is really in-transparent. The rule of thumb is that for .ch Domains you will not get charged this fee even if you get charged from outside Switzerland. For example Opodo will charge you from London, but you will not get this fee. It’s something each credit card issuer usually manually adjusts and can change - so the only one that really knows are the guys adjusting this list. AFAIK only Postfinance Credit Cards do not have the CHF abroad fee yet - all other credit cards do.

Yes if you spend more than around CHF 1’900 per month on average in Switzerland the best card to get is the TCS Mastercard Gold which has 1% cashback but costs CHF 132 (32 TCS Membership and CHF 100 for card) per year. This is by the way the only card worth considering other than the free cards in regards to cash back.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.