Honestlly, this is the lesser evil. SIX exchange for lower stamp duty and CHF for currency exchange fees.

I’m well aware that IB (and US domciled ETFs) would be overall cheaper but simplicity of Corner Trader made me start investing, that’s most important. Also, I used up my capital for an apartment purchase so I have no significant initial amount to start with. It will indeed take me some time to reach and exceed 100k. I will eventually open an IB account and perhaps keep both in parallel. I have calculated that with higher trading costs and higher fund TER compounded for 20 years I’m looking at a difference of around 20’000 CHF in favor of IB or in other words 2.5% of my capital in 20 years.

As a side note, the cowboy approach of US administration to finances (introduction of FATCA etc.) adds a layer of insecurity which I’m not ready for at the moment.

Well, if people opt for the Swiss brokers and SIX-listed ETFs, it’s for the sake of simplicity. I agree, if you have a bank account at PostFinance and open a depot there, buy som VWRL on SIX, then it’s really easy.

But of course you pay a price for that. You have higher broker fees, you have currency exchange fees, you have stamp duty for using a Swiss broker, you can’t reclaim withholding tax from USA. 1% for currency exchange is just unacceptable. It’s a huge cost.

The withholding tax is not included in the TER. It is deducted from the dividend. You can check on Vanguard’s website that it pays e.g. $1.00 per share on March 24 2018. But when you have VT, you will only get $0.85 and $0.15 will go to uncle Sam. When you own VWRL, you will receive the whole dividend, but it will be 0.85 from the start. The withholding tax that Vanguard paid to USA for the US-part of the ETF is hidden.

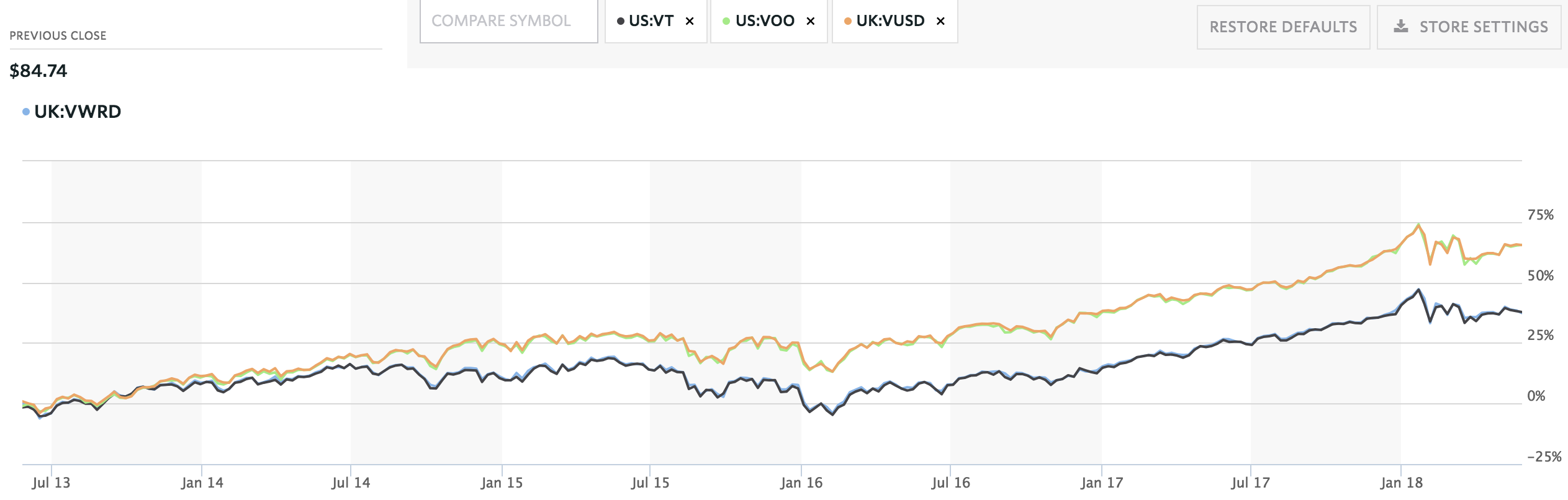

Actually, I’ve got a question. Here’s a chart from MarketWatch, which compares the relative price change of VWRD vs VT and VUSD vs VOO. As you can see, the two pairs are almost glued to each other.

So why are the European versions not lagging behind due to higher TER?

And why does VWRD not differ a bit from VT, due to not having small caps?

When I was looking into VWRD I noticed it had an excellent tracking difference of ~-0.25%, so effectively “negating” TER. This might be reason. I’m not exactly sure what the TD of VT is though, I think something around 0.09%

It could also be that the charts are shown without TER?

If I understand correctly, the chart is showing the price, the closing price from the exchange. On one hand, it makes sense that it’s identical, VOO and VUSD track the same thing. But where is the TER?

Ok so in the end, whether you own VUSA or VWRL, it does not make a big difference from the tax perspective. Could it be interesting to keep a little bit of VUSA on top of the VWRL in the portfolio since the TER costs are lower and to increase the US exposure a bit? or it makes no sense at all due to too much overlapping

for instance taking the example for Glina. That could give 50% VWRL, 20% VUSA + Small caps and Gold

If you look at the graphs, they all start at the same point (100 USD) in 2003.

By 2018, the MSCI World Small Cap rose to 562.60, while the MSCI Emerging Markets rose to 590.99 but it had a way bumpier road along the way. The MSCI World returned 374.80 with least volatility.

As to trading costs and TER, my calculations show that an additional initial investment of 500 CHF in first year covers 20 years of compounded trading cost and TER difference between IB and Corner trader so this is indeed perhaps a bit overblown in proportions. As a matter of fact, this has convinced me to sell one of my camera lenses so that I don’t feel bad for investing via Corner.

Edit:

Oh and by the way 50% VWRL, 20% VUSA only makes sense if you inted to heavily overweight USA. The VWRL already includes 51% US.

As mentioned, the only alternative MSCI All World Small Cap is the Ishares WSML, but it’s not on SIX and not in CHF.

The WOSC, same as VWRL is listed in ICTax, https://www.ictax.admin.ch/ so the tax authority knows exactly what to charge for dividends. I don’t think it makes any tax difference if you own an accumulating or distributing ETF as long as you are in the wealth accumulation stage. It is also my understanding that the TER is relatively high due to US withholding tax which is levied at fund level, but don’t take my word for it.

I have a monthly payment to my trading account, but purchase shares every 2-3 months to minimize trading costs. Only 1 ETF per purchase. I’m aware that this will cause some portfolio balancing errors at first, but I’ll manage.

Browsing thru the various discussions on the advantages/disadvantages of accumulating/distributing funds specifically for Swiss residents, I have a query.

I plan to invest in VTI, VXUS and VOO (overweight on large and mid cap for now) by making monthly investments thru Degiro, in a consolidated portfolio combination of

Question which I have is, from a Swiss resident perspective, what is better (accumulating vs distributing) if one chooses to invest in US domiciled funds?

Are there different ISIN ids for accumulating vs distributing versions of VTI, VXUS and VOO?

Any suggestion or criticism on the above portfolio is also welcome.

Apologies if the query seems overly simplistic. Thanks for your time and effort in replying!

VTI and VOO are largely the same thing, you’re way overweighting US (70%) compared to its place in the world (~55%), is that what you wanted to achieve?

Ok thanks for the link. Saw it earlier but I am not sure I am using the tool right. Where do you actually enter VWRL (or WOSC) ? i downloaded the reports but cant find it there.

Did you finally choose the 70/20/10 split mentioned above (including AUUSI - by the way is that one also registered)? That would mean the following (sorry to ask but new to the topic, I like reading about other strategies)

→ month 1: 70% of the saved money on VWRL

→ month 2: investment on WSOC to reach 20% of portfolio

→ month 3: investment on AUUSI to reach 10%

that would mean that (at least at first) every time you invest on VWRL the ratio will change a lot, and you will correct it in the following months? Is it better than investing on the 3 ETFs every 9 months?

If you have an initial amount to invest, it would make sense to buy your portfolio of choice at once in multiple transactions, and then distribute regular purchases so that the ratio remains correct in one year.

@hedgehog do you know why these ETFs I mentioned have identical price charts? (VWRD=VT, VUSD=VOO) Why don’t they diverge due to different TER or lack of small caps in VWRD?

No, the exact opposite, they pay out all dividends. That’s a good thing for swiss investors as accumulated reinvested dividends would get taxed in Switzerland with not so transparent rules as to how the extra tax is calculated. Dealing with distributing funds is much simpler.

Have a look at their distribution yield, expenses normally are first subtracted from distribution rather than recouped by selling shares

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.